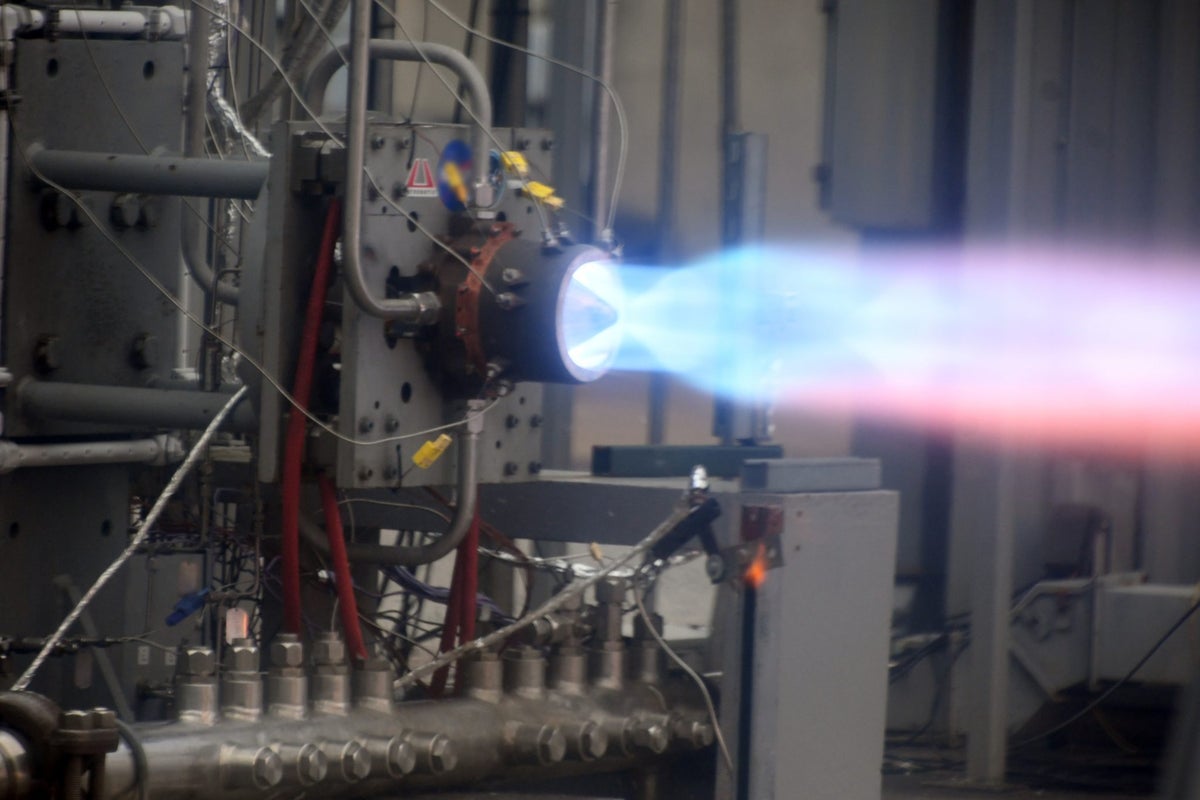

Astrobotic successfully tested two rotating detonation rocket engines for more than 470 seconds, including a 300-second continuous burn that it says may set an RDRE record. Each engine produced more than 4,000 pounds of thrust, and the company sees the technology as a path toward future lunar landers and in-space transfer vehicles. The news is encouraging for advanced space propulsion, but it remains early-stage and is unlikely to move markets broadly.

This is less a near-term revenue catalyst for Astrobotic than a validation event for a propulsion stack that could alter mission economics across the small-launch and cislunar logistics ecosystem. If RDREs can sustain burns reliably, the real winner is any platform where delta-v and payload mass fraction are binding constraints: lunar landers, orbital tugs, upper stages, and defense maneuver vehicles. That shifts value away from pure launch-bus providers and toward companies that can own the propulsion IP, hot-fire testing capability, and flight qualification pipeline.

The second-order effect is competitive pressure on incumbent propulsion suppliers: if detonation cycles deliver even a modest efficiency edge, the benefit compounds through fewer stages, more payload margin, and lower unit cost per delivered kilogram. That matters most in markets where customers pay a premium for schedule assurance and payload flexibility, not headline thrust. It also creates a procurement bottleneck around test infrastructure, valves, tanks, thermal materials, and high-frequency instrumentation — the picks-and-shovels layer is likely to monetize earlier than the prime contractors.

The market is probably underestimating time-to-revenue risk. This is still a lab-to-field bridge, and the failure modes are harsh: combustion instability, repeatability degradation, and qualification over many cycles, not one long burn. The next 6-18 months should be treated as a catalyst window, with sentiment likely to overreact to any flight test announcement; conversely, one anomaly could reset the category for a year or more because investors will extrapolate it to the whole RDRE class.

The contrarian view is that the value may accrue more to defense and mission-enablement than to commercial launch. If RDREs improve maneuverability and range for orbital transfer vehicles and proximity ops, the economic prize could be in national security and in-space logistics contracts, not in cheap launch. That argues for exposure to companies with broader propulsion portfolios and government ties rather than narrow pre-revenue space names.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35