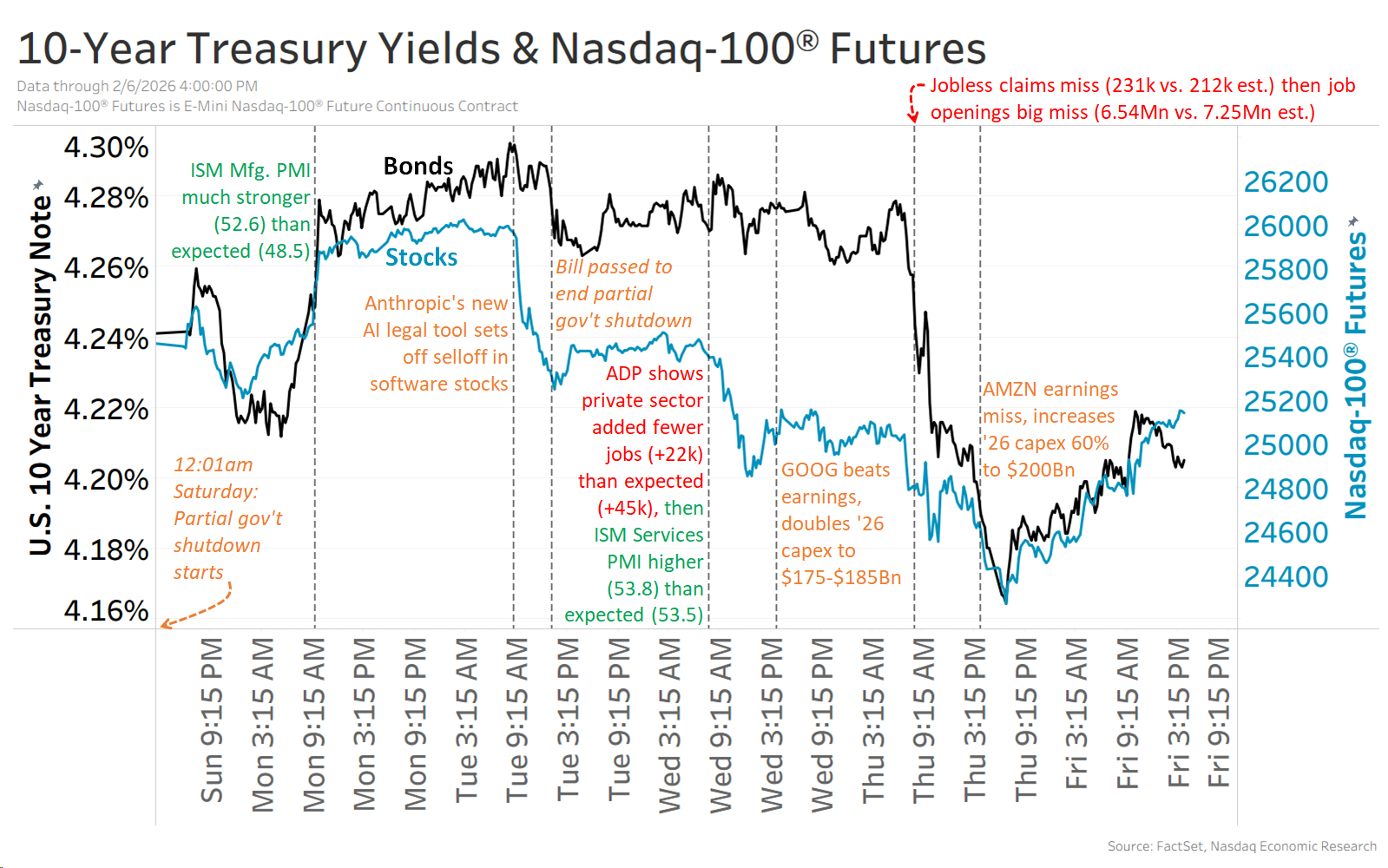

Markets turned risk-off as AI-related disruption fears and hefty AI capex plans weighed on tech: Anthropic’s new legal tool triggered a selloff in software (including private markets) while Google said it would double 2026 capex to $175–$185bn and Amazon flagged a near-60% capex increase to ~$200bn, renewing profitability concerns. Labor prints were mixed-to-soft (ADP +22k vs +45k expected; initial claims 231k vs 212k; JOLTS ~700k below expectations but hiring rates rose and layoffs remained low), and market moves included software -9% for the week, Nasdaq-100 down ~2%, and the 10-year yield down ~5bp to ~4.2%.

Market structure: The immediate winners are hyperscalers and AI-infrastructure suppliers (GPUs, data-center power/real estate) as GOOG’s announced capex jump to $175–185B and AMZN’s +60% to ~$200B lock compute demand and pricing power into a smaller set of players. Losers are mid/small-cap enterprise software firms and private-market SaaS investors facing accelerated product obsolescence and margin compression as foundation models commoditize functionality; software was off ~9% this week, a leading indicator of re‑rating. Cross-asset: equity risk-off lifted bond demand (10y -5bp to ~4.2%), raised tech IV and option skew, while energy/industrial inputs for data centers (power, copper) see higher forward demand. Risk assessment: Tail risks include rapid regulatory constraints on model use (EU/US AI rules within 3–12 months), GPU supply shocks or price spikes, and hyperscaler capex overruns that compress free cash flow into 2026–2028. Near-term (days–weeks) expect sentiment-driven drawdowns similar to this week; medium (months) hinges on Q1–Q4 2026 guidance cadence from GOOG/AMZN; long-term (years) likely concentration of economic rent with 3–5 hyperscalers. Hidden dependencies: enterprise adoption speed, third-party model liability events, and NVIDIA supply; catalysts that could reverse trends include a clear ROI story from enterprise AI pilots or regulatory clarity within 90–180 days. Trade implications: Tactical plays favor long AI-infra exposure and defensive trimming of software; consider 1–2% overweight in NVDA (GPU beneficiary) and 2–3% underweight or hedged exposure to IGV-like software ETFs given likely margin pressure over 6–12 months. Use option structures: buy 3‑month put spreads on IGV (10%–15% OTM) to hedge downside and sell 6–9 month covered calls on GOOG/AMZN to monetize elevated premiums while holding selective long exposure. Rebalance into any persistent >12% pullback in hyperscalers where capex is clearly funding monetizable cloud/AI services. Contrarian angle: Consensus underestimates hyperscalers’ ability to monetize AI via per-call pricing, custom chips and enterprise subscriptions — initial margin hit from capex could be followed by 30%+ incremental operating margins on AI services over 3–5 years. The week’s 9% software correction may be overdone if enterprise churn remains low and hiring/sticky ARR holds (Indeed/ADP signals mixed); historical parallel: cloud capex cycles (2016–2019) saw short-term multiple compression then concentration and outsized returns for infrastructure winners. Unintended outcomes: persistent overspending could trigger M&A (acquihires, vertical consolidation) — watch deal flow as an early signal of structural re-pricing.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment