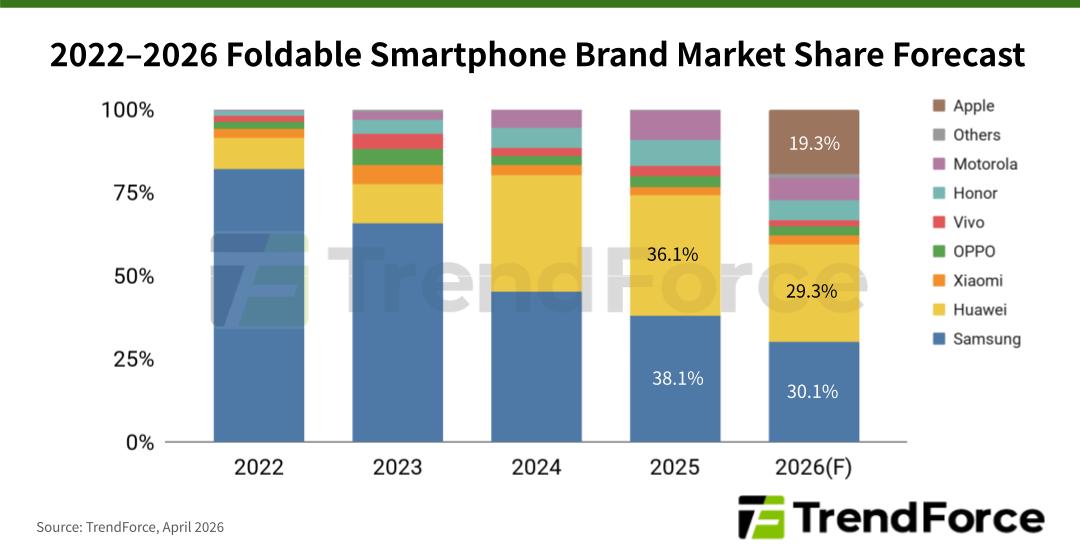

TrendForce says Apple could enter foldable smartphones in 2H26 and capture nearly 20% market share, with Samsung Electronics and Huawei each potentially near 30%. The main investment takeaway is that crease reduction is shifting from hinge design to materials innovation, especially optimized OCA, UTG, and stress management. The article is constructive for foldable-display supply chain innovation but is largely forward-looking rather than immediately market-moving.

The strategic issue is not whether Apple can ship a foldable, but whether it can redefine the category fast enough to reset buyer expectations around durability and crease visibility. If it lands with a materially better user experience, the first-order winner is not just AAPL hardware margin; it is a multi-year ASP reset across the premium smartphone stack, because incumbents will be forced to spend more on materials, hinges, and yield without getting commensurate pricing power. That tends to compress mid-tier foldable economics first, where weaker brands have less room to absorb higher BOMs and lower panel yields. The bigger second-order beneficiary is the display/materials ecosystem rather than the hinge complex. An Apple launch would likely pull forward demand for higher-spec OCA, UTG processing, laser drilling, and precision metrology, creating a tighter procurement environment for suppliers with unique process know-how. The likely losers are vendors whose differentiation sits in mechanical ingenuity alone; once the market frames crease reduction as a materials-and-stress problem, hinge IP becomes necessary but no longer sufficient, which usually shifts gross margin from assemblers to upstream process suppliers. Consensus may be underestimating how slow the category can be to scale even after a strong Apple entry. Foldables remain a yield-and-reliability problem, so even if Apple captures meaningful share in the premium segment, the adoption curve may be lumpy over 12-24 months rather than linear. The tradeable opportunity is likely in supplier re-rating ahead of launch windows, while handset competitors face a slower but more persistent margin headwind as they match the experience with inferior economics. Near-term downside risk is mostly execution: if Apple’s solution adds weight, thickness, or battery trade-offs, the market could treat the launch as incremental rather than category-defining. On the other hand, if early teardown evidence shows a superior stress-management stack, suppliers tied to advanced adhesive and glass processing could see a valuation step-up well before volumes inflect.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment