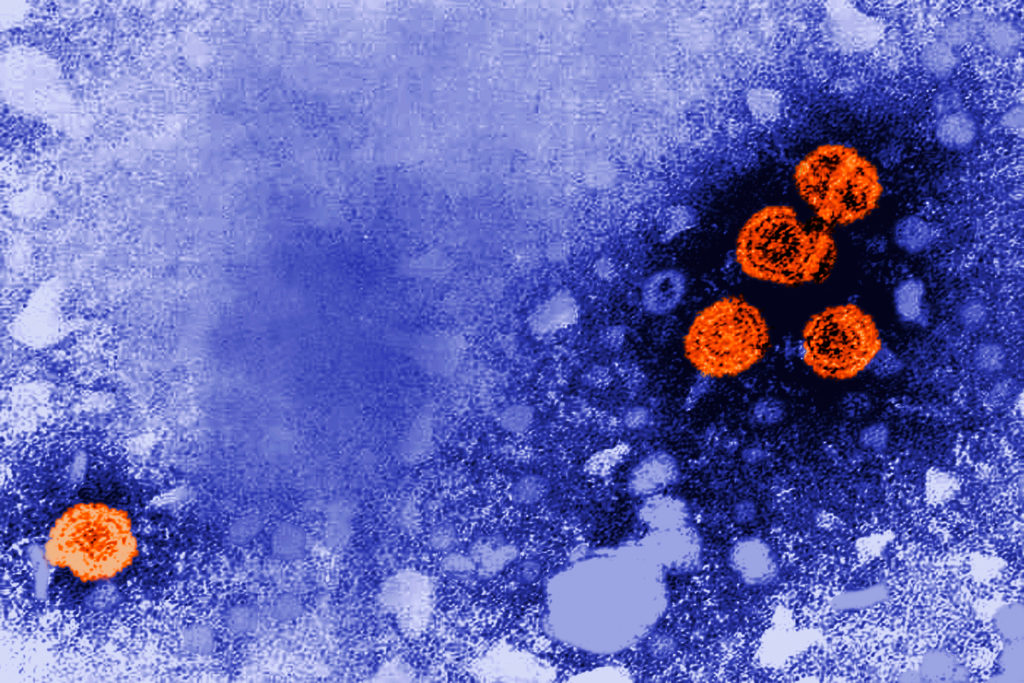

An experimental hepatitis B drug, bepirovirsen, produced a 'functional cure' in about 20% of patients across two international studies, allowing some to stop treatment without viral rebound for at least six months. The therapy is under fast-track FDA review, with a decision expected in October, and regulators in Japan, China and Europe are also reviewing it. While the results are a meaningful advance for a disease affecting more than 250 million people globally, researchers cautioned that longer-term durability and broader patient populations still need study.

This is less about an immediate revenue step-up and more about a valuation re-rating for both names: the market has been pricing HBV as a chronic, slow-moving franchise with modest durability, and a credible functional-cure signal changes the terminal-value conversation. For GSK, the upside is not just the asset itself but the read-through that its antiviral platform can create a second growth engine outside the legacy respiratory/base business; for IONS, the event de-risks the commercialization narrative around nucleic-acid therapeutics and validates the partnership model as a monetization path rather than a science project.

The second-order winner may be payers and health systems, because a therapy that reduces lifelong treatment dependence creates a future cost-offset argument that can support premium pricing and broader reimbursement. The more important competitive effect is on every HBV incumbent: chronic antivirals, liver-disease monitoring, and eventually some transplant-related economics face a slower-growth end market if functional cure rates scale from ~20% into a broader label. That said, the trial population looks selected enough that investors should not extrapolate a clean conversion to cirrhotic or high-antigen patients; the commercial pool may be meaningfully smaller than the headline addressable market suggests.

Near-term catalyst path is asymmetric: FDA timing in months, not days, but headline volatility can still be large if regulators ask for durability or safety follow-up. The biggest tail risk is that the market overprices a broad label before the data answer durability, retreat rates, and use in harder-to-treat subgroups; any signal of liver-enzyme issues, relapse after treatment cessation, or narrower-than-expected eligibility could compress the re-rating quickly. Conversely, if the October decision is clean, this can become a multi-quarter sentiment trade rather than a single-day event.

Consensus is likely underestimating how much of the near-term upside already belongs to GSK versus Ionis. GSK gets the larger commercial claim and a cleaner strategic story, while IONS gets platform validation but still depends on partner economics and pipeline breadth to translate into sustained multiple expansion. The best contrarian framing is that the science win is real, but the stock market may overvalue the first drug’s peak sales while underweighting the probability that the initial label is narrower and the durability data remain the gating item.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.72

Ticker Sentiment