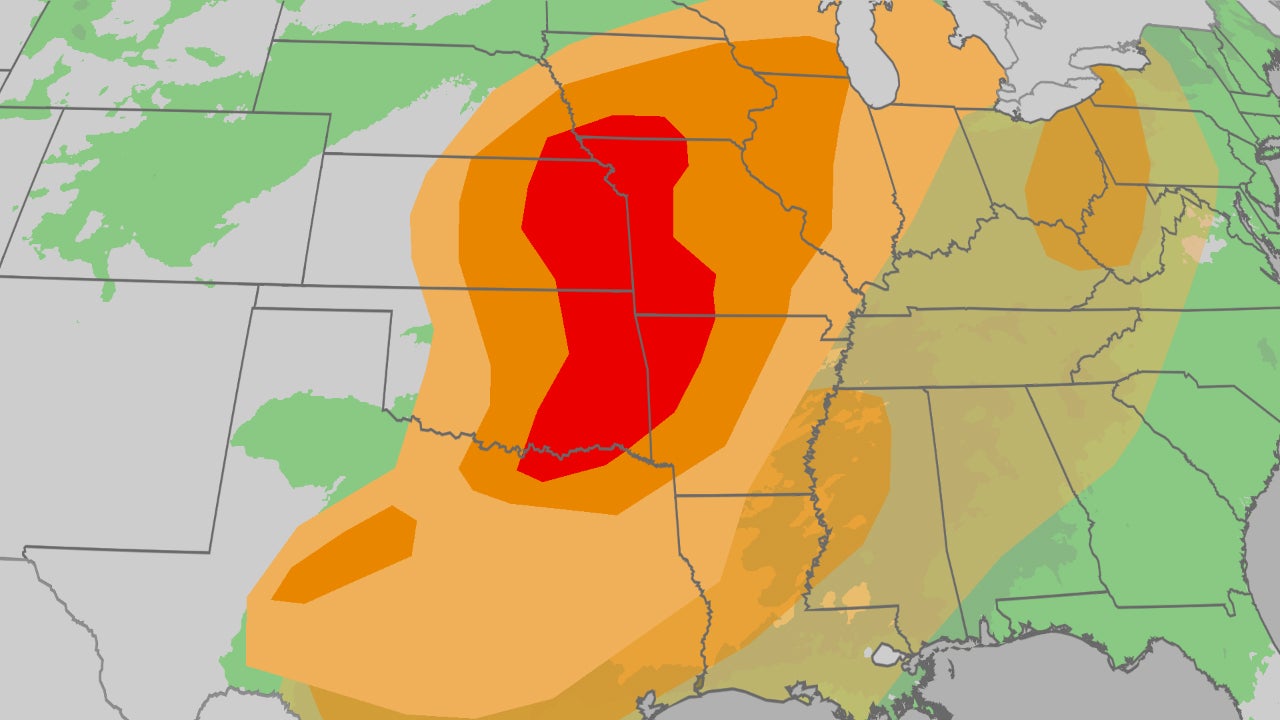

A multi-day severe weather outbreak is forecast beginning Friday across the Plains into the Midwest, with the SPC highlighting an elevated risk of EF2+ tornadoes in parts of eastern Oklahoma, eastern Kansas, western Missouri and western Arkansas; hail up to 2.25 inches was reported in Hall County, Texas, and at least three tornadoes were observed late Thursday. Multiple rounds of storms could produce localized flash flooding with an additional 3+ inches of rain across parts of the Southern Plains and Mississippi Valley, threatening infrastructure, logistics and insured losses, and the threat may return early to mid-next week as a strong cold front and upper-level low move into the central and eastern U.S., with drought context tied to a fading La Niña.

Market structure: Severe storms concentrate near-term winners in building materials, roofing and debris-removal services (Home Depot HD, Lowe’s LOW, Owens Corning OC, Waste Management WM) with localized demand shocks of ~2–6% revenue lift in affected MSAs over 4–12 weeks; losers are P&C insurers and reinsurers with concentrated exposure in Plains/Midwest (Travelers TRV, Progressive PGR, RenaissanceRe RNR) where modeled insured loss layers and reserve volatility push near-term equity volatility +30–70% and may pressure combined ratios by several hundred bps if losses exceed $1–3bn regionally.

Risk assessment: Tail risks include a multi-week outbreak producing >$5–10bn insured losses triggering reinsurance repricing at upcoming H1 renewals and state-level rate interventions; immediate (days) operational risks are logistics/planting delays and supply constraints for shingles/plywood, short-term (weeks–months) are claims adjudication and price inflation for contractors, long-term (quarters) could be higher insurance premiums benefiting underwriting margins. Hidden dependencies: concentrated reinsurance attachment points, municipal borrowing for recovery, and seed/planting calendars for Midwest crops that would amplify commodity moves.

Trade implications: Direct plays: favor short-dated tactical exposure to building-material upside (HD, OC, LOW) and commodity longs in corn/soy on planting delays (CORN ETF or July futures). Defensive shorts/purchased puts on reinsurers/insurers (RNR, TRV, PGR) to capture implied-volatility expansion; use option structures to limit capital. Cross-asset: expect spiking equity vols, modest widening in catastrophe bond spreads, and short-term flattening in regional muni credit where recovery spending rises.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Contrarian view: Consensus may over-penalize large diversified insurers with diversified book (Chubb CB, Allstate ALL) — incremental premium rate increases and reinsurance adjustments often restore profitability within 2–4 quarters. Historical parallels (spring tornado outbreaks) show sharp short-term equity drawdowns but recovery within 3–6 months; mispricing exists in near-term implied vols and select option premia which can be sold against carefully sized protective hedges.