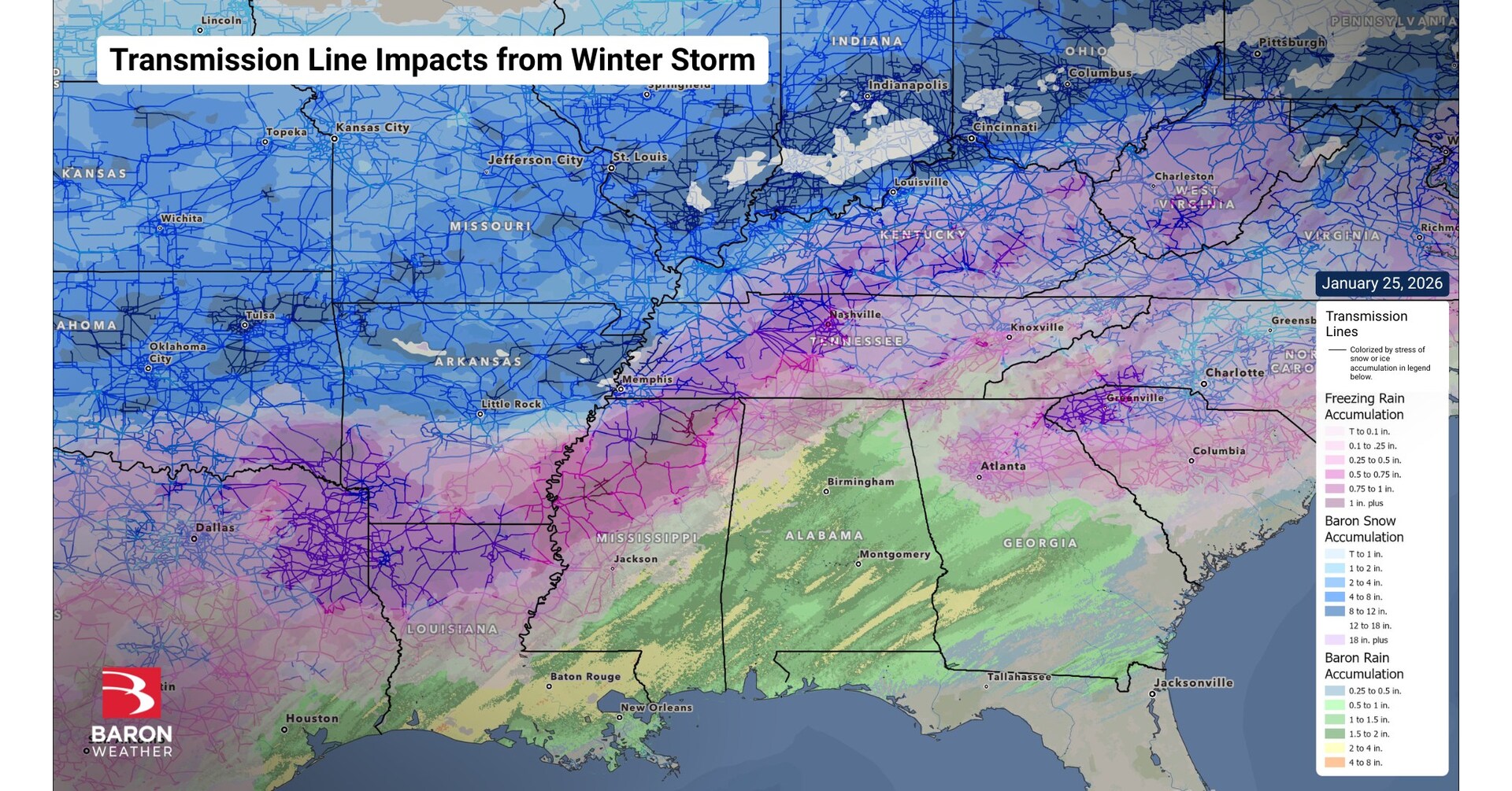

Baron Weather expanded its partnership with Esri so Esri customers can purchase its premium weather data products directly through ArcGIS, gaining access to 25+ products across domestic and global coverage. The portfolio covers real-time radar, satellite imagery, severe storm intelligence, road conditions, and tropical tracking, delivered as continuously updated map/feature services (up to every two minutes). The change reduces friction by eliminating a separate vendor relationship, supporting improved operational situational awareness for utilities and government users.

This is more a distribution upgrade than a demand shock. For a niche data provider, the economic value comes from reducing friction inside an incumbent workflow: shorter sales cycles, higher attach rates, and better renewal odds when the product is embedded in a system customers already budget for. That tends to lift lifetime value more than it lifts next-quarter revenue, so the market should be careful not to capitalize this as a step-change in growth. The second-order winner is likely Esri, not just Baron: adding a higher-frequency weather layer makes ArcGIS stickier for utilities, public-sector buyers, and critical-infrastructure customers that live or die by operational latency. The competitive pressure falls on standalone weather-data vendors and smaller GIS add-on providers, because bundling through a dominant workflow platform can compress pricing and make procurement decisions path-dependent. If this expands into broader enterprise usage, it also raises switching costs for customers who build alerts and response protocols around the integrated feed. The contrarian point is that this may be strategically important but financially modest until there is proof of incremental bookings. The consensus tends to overrate partnership announcements; the missing variable is whether Esri’s channel actually creates new seats versus simply redistributing existing spend. Falsify the thesis if management cannot show conversion, ARR uplift, or lower churn within 1-2 quarters; if that evidence appears, the upside is more likely a slow grind higher over 6-18 months than a re-rating spike in days.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.12

Ticker Sentiment