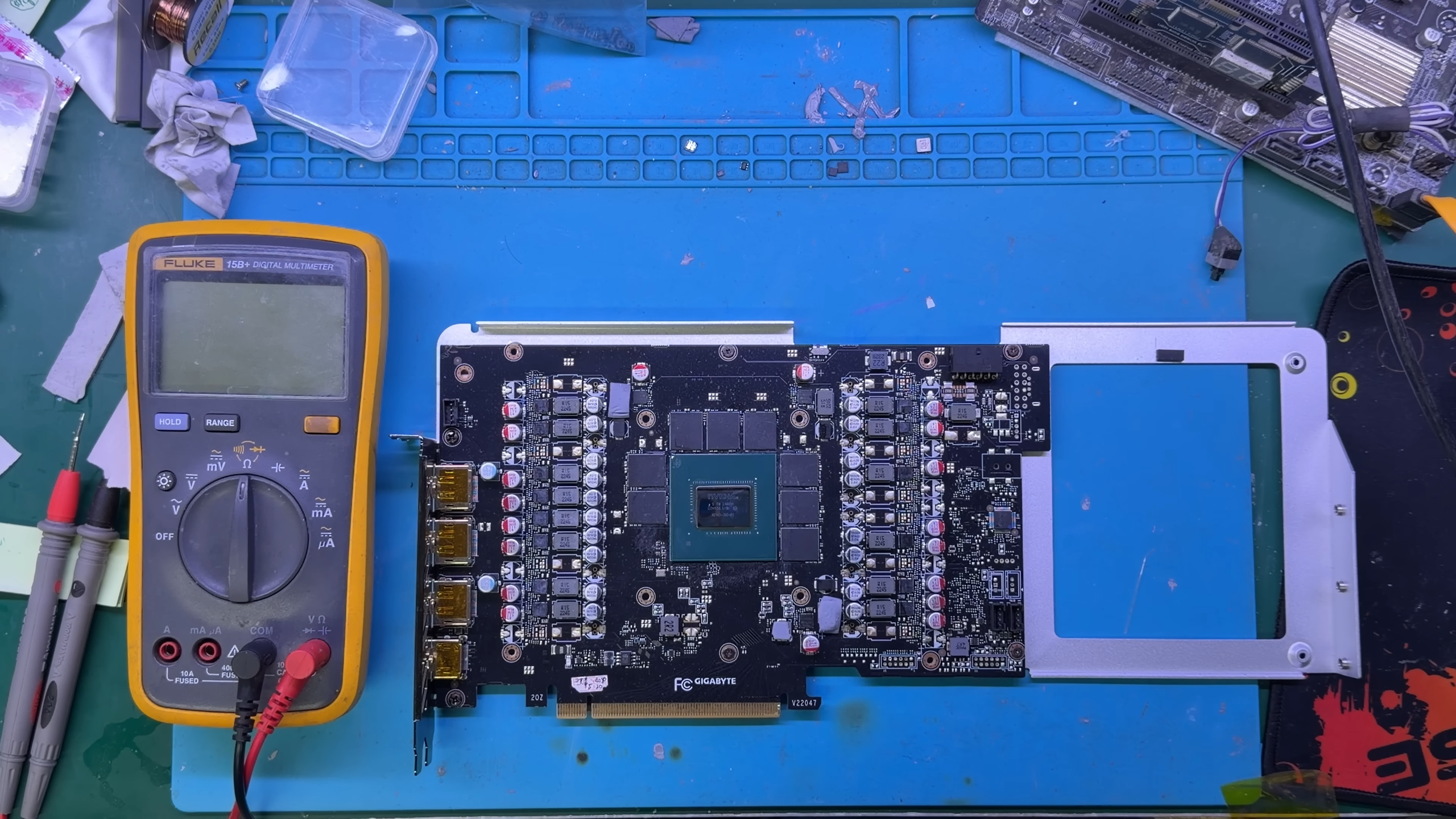

A DRAM shortage has tightened GPU supply and inflated prices while enabling sophisticated second‑hand scams: a Gigabyte GeForce RTX 4080 (launch MSRP ~$1,199) was sold for ¥~143.50 (~12% of retail) but contained an Ampere GA106 die (RTX 3060 Mobile) and suspect GDDR6X memory. Nvidia has reportedly cut partner supply by up to 20%, which will further constrain availability and support higher prices; AMD says it will try to hold pricing near MSRP but may have to raise prices later. The story highlights heightened operational and reputational risks in the used‑hardware market and potential upside pressure on OEM and component pricing.

Market structure: The DRAM shortage (Nvidia reportedly cutting board-partner supply by up to 20%) tightens GPU availability, boosting pricing power for Nvidia (NVDA) and DRAM suppliers (e.g., MU, SMH constituents) while eroding second-hand marketplace trust (negative for EBAY). Counterfeit scams increase frictional costs for used-market liquidity, shifting demand toward verified retail channels and OEM-authorized refurbishers, which can sustain gross-margin expansion for tier-1 GPU vendors over the next 3–12 months. Risk assessment: Tail risks include a rapid DRAM supply normalization (e.g., >15% spot DRAM price decline in 3 months) that would compress DRAM supplier margins, and a China-led regulatory crackdown on cross-border second-hand electronics or on chip re-marking that could disrupt supply chains. Immediate (days) risks: reputational headlines and platform liability suits raising short-term volatility; short-to-medium (weeks–months): pricing adjustments by AMD or Nvidia; long-term (quarters) structural shifts to onshore fabs if exporters/controls tighten. Trade implications: Tactical long in NVDA and select DRAM names benefits from sustained tightness—favor 2–3% portfolio exposure to NVDA and MU via equity or call-spreads over 1–3 months, funded with OTM call sales to cap cost. Small short exposure (1–2%) to EBAY equity or 2–3 month puts captures marketplace trust erosion; pair trade: long NVDA (2%) / short EBAY (1%) to express pricing-power vs. platform-risk. Contrarian angles: The market underestimates that scams can accelerate capture of demand by authorized channels, concentrating revenues among OEMs and on-brand retailers—this favors NVDA and authorized AIB partners, not generic marketplaces. Historical parallel: 2020–21 GPU/crypto cycle saw 30–50% retail spikes then rapid collapse; set mechanical stop/trim rules (e.g., trim DRAM longs if spot DRAM down >15% in 90 days) to avoid a repeat correction.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45

Ticker Sentiment