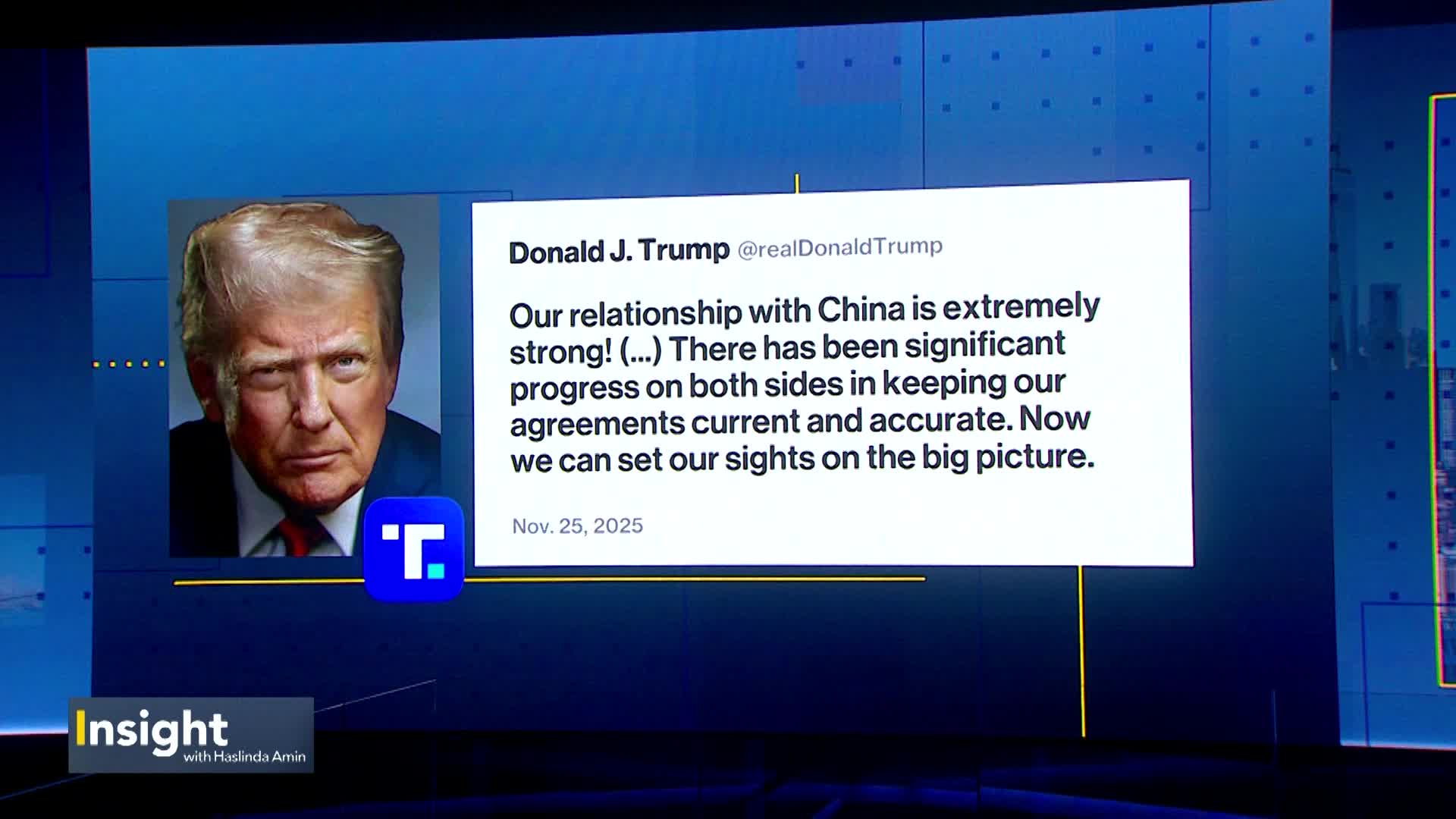

Former President Trump held separate calls with Chinese leader Xi Jinping and Japanese politician Sanae Takaichi that produced policy signaling with potential implications for US-China relations and Japan–US alignment. The exchanges could presage shifts in trade rhetoric, tariffs or export-control postures and thereby affect supply-chain-sensitive sectors, Asian equities and FX positioning; investors should monitor for concrete follow-on policy actions or joint statements that would move markets.

Market structure will bifurcate: semiconductor equipment and foundry suppliers (ASML, LRCX, AMAT, TSM) gain pricing power if export controls/tariff risk eases and deferred capex resumes, while China‑exposed consumer names and exporters (NIO, LI, PDD, AAPL’s China revenue line) face either upside from demand or downside from renewed restrictions — positioning should reflect binary outcomes. Supply/demand for advanced tools is inelastic short‑term (12–24 months) so even a 10–20% policy relaxation could translate to a 15–30% uplift in orders; conversely an abrupt tightening can produce >20% share re‑rating for exposed firms. Cross‑asset implications: risk‑on reduces safe‑haven flows (US 10y -10–20bps potential), CNH appreciation of 1–3% on détente, and commodity upside (copper +3–6%) via industrial demand reacceleration. Tail risks center on a sudden policy U‑turn: emergency export bans, sectoral sanctions or a Taiwan/Maritime incident that would spike volatility across Asian equities and FX; probability low but impact extreme (30–50% drawdowns in targeted names). Time horizons split — immediate (days) for FX/option vols, short (weeks–3 months) for Q‑revenue guidance revisions, long (12–36 months) for capex/resilience reconfiguration. Hidden dependencies include non‑transparent supply chain nodes (substrates, rare earths) and US congressional action that can override bilateral presidential signaling. Catalysts: a joint communique, coordinated tariff rollback, or a congressional bill in the next 30–60 days. Trade implications: establish modest asymmetric exposure — 2–3% long in ASML (ASML) and 1.5–2% long TSM (TSM) with 8% stop and 20% 12‑month target if a positive joint statement occurs within 60 days; hedge with 1% allocation to 3‑month puts on LRCX or a short 1% position in China‑listed EVs (NIO) to protect against renewed restrictions. Use volatility trades: buy 3‑month ATM straddles on USD/CNH (delta‑neutral) sized to 0.5–1% portfolio to capture policy‑driven FX moves; consider 3‑6 month call spreads on NVDA (bullish on easing) funded by selling OTM calls if implied vol >40%. Rotate overweight semis and industrial capex, underweight China consumer discretionary by 30% of current weight until policy clarity (30–90 days). Contrarian angles: consensus treats rhetoric as short‑lived; markets underprice multi‑year structural decoupling — therefore long positions in non‑China fabs (TSM/ASML) may be underappreciated even if near‑term détente occurs. The market could overreact to a minor conciliatory statement (overbought Asian equities); trade size accordingly and avoid full conviction until a written agreement or reciprocal actions materialize. Historical parallels (2018 tariff cycles) show volatility spikes followed by multi‑quarter capex commitments; unintended consequence of early easing is political backlash that restores tight controls within 6–12 months, so keep convex hedges in place.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00