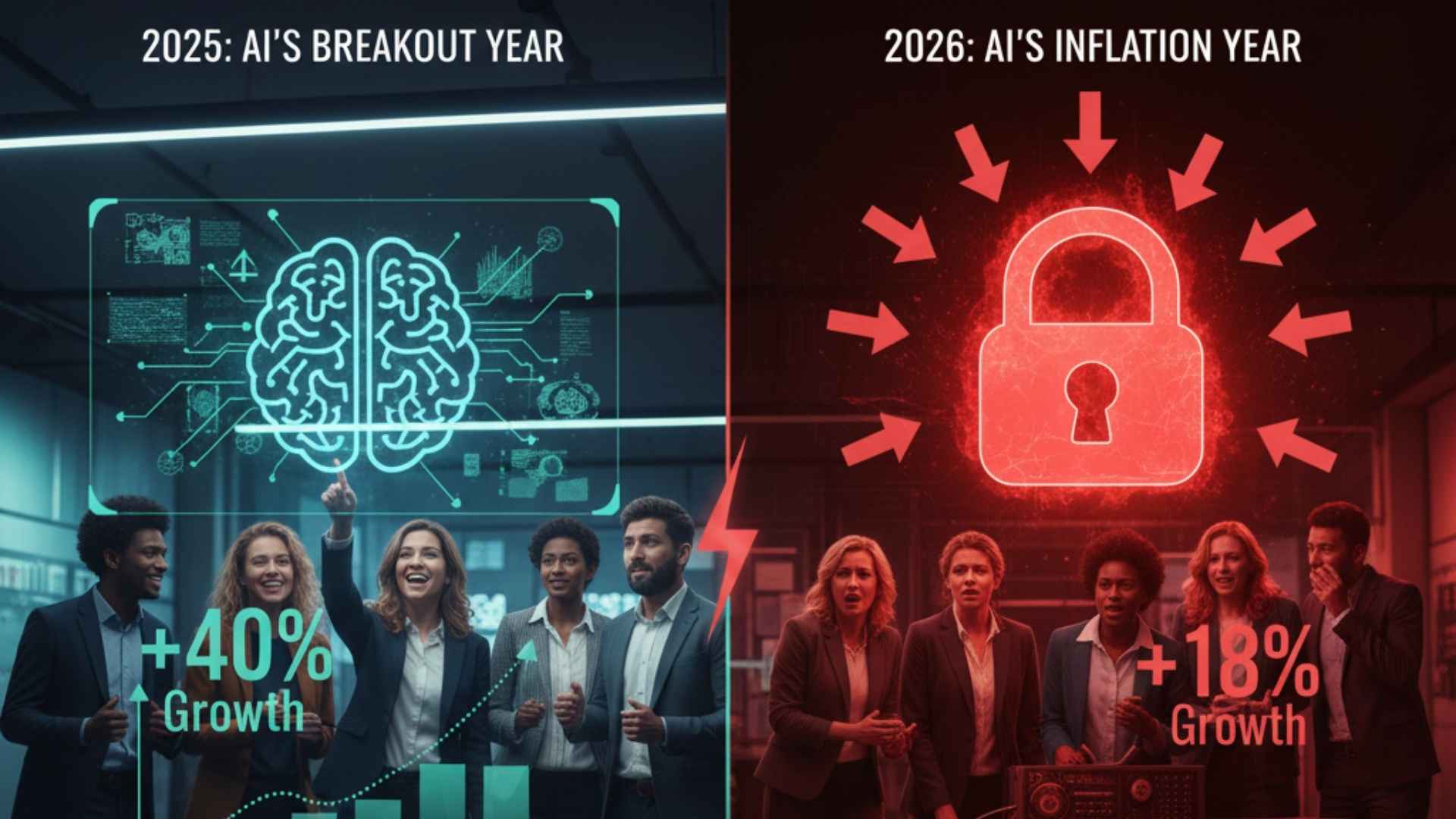

Corporate adoption of AI moved from fringe to infrastructure in 2025, with major tech firms (Microsoft, Meta, Alphabet) and startups (Anthropic, Cohere) driving market gains and large funding/cloud-compute deals (Anthropic → Azure on Nvidia GPUs). By late 2025 roughly 78% of companies used AI in some form, Samsung pledged to double AI-capable devices to 800m in 2026 (from ~400m in 2025), and enterprises poured capital into data centres, chips and electricity. While investors rewarded aggressive AI investment, analysts warn these broad spending patterns could fuel inflationary pressure through 2027 and create chip/energy supply constraints that reshape labour, costs and investment strategies into 2026.

Market structure: Hyperscalers (MSFT, GOOGL/GOOG, META) and chip leader NVDA are clear winners — they capture both enterprise spend and pricing power for AI compute; expect 2026 revenue upside of +10-30% vs peers as cloud commitments and device integrations scale. Losers include legacy software vendors slow to embed models (SAP at risk of margin compression) and labour-heavy service firms facing automation-driven demand erosion. Cross-asset: sustained AI capex pushes near-term inflationary pressure raising real yields and commodity demand (power, copper); expect 10y yields to drift +25–75bp if CPI remains >3% through H1 2026. Risk assessment: Tail risks include export controls on advanced GPUs, a run-rate GPU supply shock, or sweeping AI regulation that could compress model monetization — these are low probability but could cut NVDA/MSFT multiples by 30–50% within weeks. Time horizons: immediate (days–weeks) = higher equity vol and event-driven re-pricings; short (3–9 months) = earnings mix shifts as AI revenue recognition lags; long (1–3 years) = structural productivity gains but also persistent sectoral inflation through 2027 per consensus. Hidden dependencies: grid capacity, hyperscaler capex cycles, and concentrated AI talent create bottlenecks that amplify shocks. Trade implications: Favor concentrated exposure to MSFT/GOOGL/NVDA on pullbacks of 10–15% with 6–12 month holding periods; hedge with TIPS or tail-protection options. Consider pair trades (long MSFT, short SAP) to capture secular platform gains vs legacy ERP margin pressure. Options: buy long-dated (Jan 2027) NVDA calls 25–35% OTM sized 0.5–1% of portfolio to capture convexity; sell premium into near-term earnings spikes. Contrarian angles: Market may underprice medium-term deflationary effects of AI (productivity drop in unit labor cost) even as short-term capex fuels inflation — this dichotomy can create mispricings in cyclicals vs tech. Consensus overweights “AI label” revenue; target companies with demonstrable AI-driven ARR growth >20% YoY, avoid headline-driven names without measurable product monetization. Historical parallel: cloud capex cycle 2010–15 shows multi-year supply tightness, consolidation and margin re-rating — expect similar winners and losers here.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

0.10

Ticker Sentiment