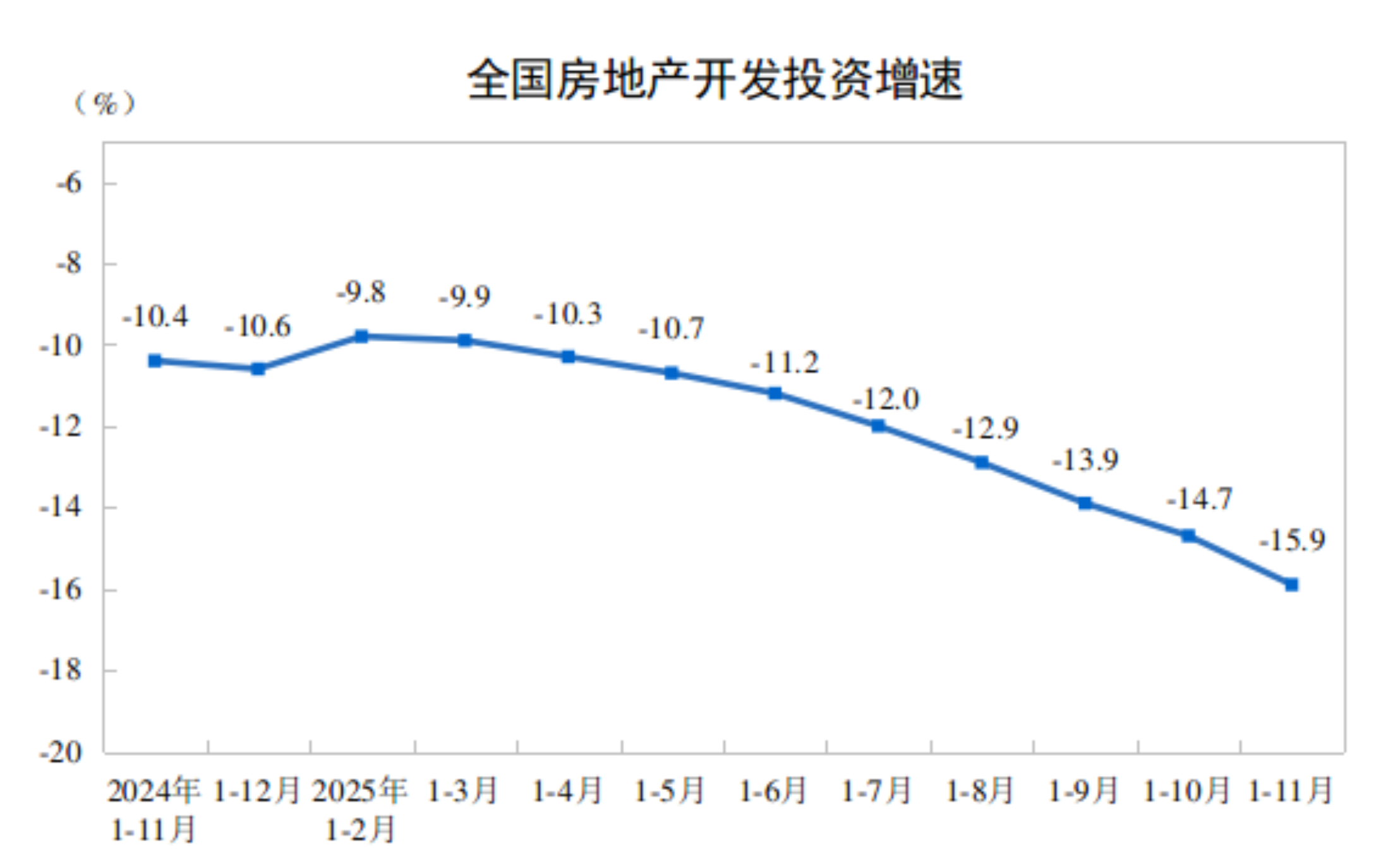

China’s property sector continued to contract through January–November as real estate development investment fell 15.9% year‑on‑year to ¥7,859.1 billion (residential ¥6,043.2 billion, down 15.0%), with floor space under construction down 9.6%, newly started area down 20.5% and completed area down 18.0%. Sales volumes also weakened—new commercial floor space sold fell 7.8% to 787.02 million m² and sales value declined 11.1% to ¥7,513 billion—while funds available to developers dropped 11.9% to ¥8,514.5 billion with declines across domestic loans, self‑raised funds, deposits/advances and mortgages; the Nationwide Real Estate Climate Index was 91.9 in November, underscoring ongoing demand weakness and liquidity stress that heighten credit and operational risks for developers and related sectors.

From January to November national real estate development investment fell 15.9% year‑on‑year to 7,859.1 billion yuan, with residential investment at 6,043.2 billion yuan down 15.0%; floor space under construction declined 9.6% to 6.5607 billion m² and residential under‑construction area dropped 10.0% to 4.5755 billion m². Newly started floor space plunged 20.5% to 534.57 million m² (residential down 19.9%) while completed floor space was down 18.0% to 394.54 million m² (residential completed down 20.1%), signaling a material pullback in construction activity and future supply delivery. Sales metrics show continued demand weakness: new commercial floor space sold fell 7.8% to 787.02 million m² and sales value declined 11.1% to 7,513 billion yuan, while inventories eased only slightly with pending‑sale area at 753.06 million m² (down 3.01 million m² month‑over‑month). Funding pressures are evident as funds available to developers dropped 11.9% to 8,514.5 billion yuan, with domestic loans down 2.5%, self‑raised funds down 11.9%, deposits/advance receipts down 15.2% and mortgage lending down 15.1%. The Nationwide Real Estate Climate Index of 91.9 in November underscores contractionary conditions; together the data point to heightened liquidity and credit stress for developers, elevated operational risk for suppliers and potential credit exposure for banks. Absent further data on policy support or funding relief, the sector outlook remains weak and sensitive to funding flows and sales stabilization metrics.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately negative

Sentiment Score

-0.60