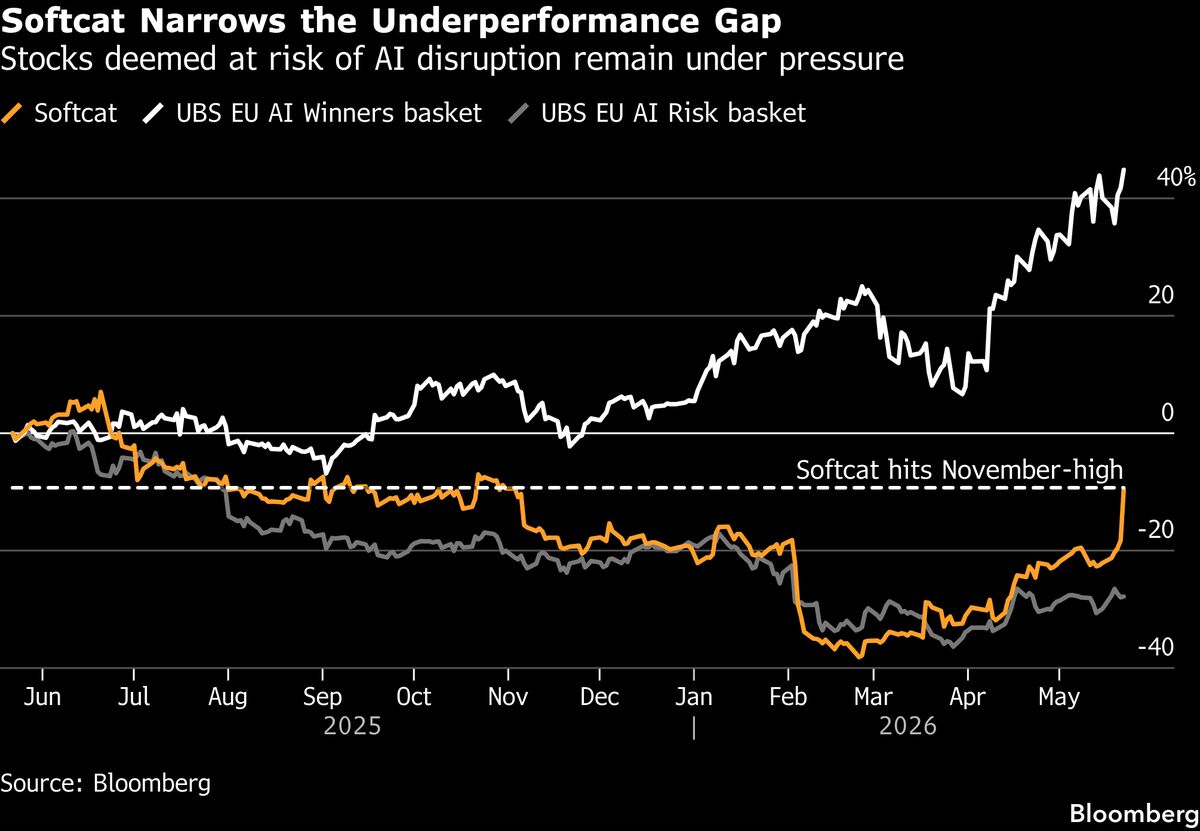

Softcat shares soared as much as 13% after the company said trading benefited from demand for AI-enabled infrastructure. The update is shifting investor perception from AI loser to AI winner and implies a more favorable growth trajectory. The move is driven by upgraded guidance and stronger demand trends rather than a broader sector event.

The important signal here is not the one-day price reaction; it is that the market is beginning to re-rate legacy IT resellers as leverage points on AI capex rather than as low-growth ticket clippers. That matters because once investors accept that AI infrastructure demand can show up in guidance beats, valuation multiples can expand before earnings catch up, especially for names with recurring enterprise relationships and relatively asset-light models. Second-order, this is more helpful for the distribution layer than for the hyperscalers: incremental AI spend tends to flow through networking, servers, storage, power, and integration services before it becomes visible in software monetization. The near-term beneficiaries are the vendors and channel partners that can bundle procurement, deployment, and support; the losers are incumbent suppliers that fail to capture share in the refresh cycle or are too exposed to commoditized PC/standard software budgets being displaced by AI-directed spend. The key risk is that this is a guidance-driven multiple move, not yet proof of durable end-demand. If AI-related orders are front-loaded or tied to a narrow cohort of large enterprise projects, the growth rate can normalize quickly over the next 1-2 quarters, creating an easy setup for a post-earnings fade. A second-order bearish risk is margin compression: if this demand comes with heavier services mix, pricing pressure, or working-capital drag, the market may eventually conclude the revenue quality is weaker than the headline suggests. Contrarian view: the consensus may be underestimating how early this is in the channel cycle, but also overestimating the durability of the rerating. In the next 3-6 months, the trade is less about absolute AI adoption and more about whether management teams can keep converting pipeline into raised guidance without a step-up in inventory or receivables. If that discipline holds, the rerating can extend; if not, this becomes a tactical squeeze rather than a structural winner.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.62