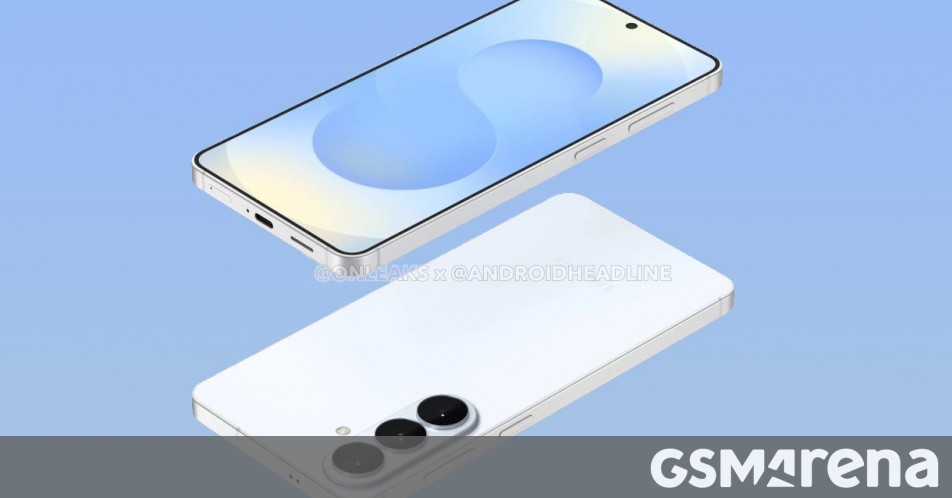

Samsung cancelled the Galaxy S26 Edge late in development and substituted an S26+ variant, but late-stage changes forced the S26+ to revert to a display nearly identical to the S25+ while the vanilla S26 will get a slightly larger 6.27" panel. Samsung prioritized the S26 Ultra, which entered mass production last month with initial production targets of 3.6 million Ultras, 700,000 vanilla units and 600,000 Plus units; those allocations are expected to be rebalanced in February toward higher vanilla and Plus volumes and lower Ultra output. The series is expected to be unveiled on February 25, and the last-minute design and supply changes signal execution risk and potential product mix impacts for Samsung's next-cycle sales.

Market structure: Samsung’s last-minute S26+ design rollback favors component incumbents (existing S25+ panel suppliers, glass/cover-glass vendors) and reduces a potential hardware premium that would have supported higher ASPs. Initial production skew (3.6M Ultra vs 700k vanilla/600k Plus) signals a deliberate mix toward high-margin Ultra units near launch but management expects to rebalance volumes upward for vanilla/Plus in Feb — a weak signal on consumer willingness to pay for mid-tier premium upgrades. Expect limited pricing power vs Apple in 1H given marginal hardware deltas and a later Feb launch date that compresses the promotional window versus iPhone 17 momentum. Risk assessment: Short-term operational risk includes supply-chain churn (panel substitution, retooling) that can cause 1–3 week delays and incremental costs of ~mid-single-digit USD per unit; tail risks (component shortage, regulatory sanctions in key markets) could cut volumes >20% and meaningfully pressure Korea-listed equities. Hidden dependency: supplier inventory positions (panels, glass) and component purchase commitments — if Samsung cancels orders, upstream suppliers (OLED fabs, glass) face abrupt revenue hits and inventory markdowns. Key catalysts: Feb 25 launch and February volume target revision; watch unit guidance and channel sell-through over first 4–6 weeks post-launch. Trade implications: Tactical trades should focus on suppliers and volatility around the Feb 25 event rather than Samsung parent multiple — buy options on diversified suppliers (Corning GLW, Qualcomm QCOM, Sony SONY) and avoid concentrated exposure to small Asian panel vendors (e.g., BOE). Consider relative trades: long Corning (GLW) vs short small-display suppliers where order cancellations risk is concentrated; size positions 1–3% portfolio and use defined-risk option structures. Expect meaningful option IV lift into Feb 25; use calendar or vertical spreads to monetize premium if directional view uncertain. Contrarian angles: Consensus will read this as a marginal negative for Samsung handset growth; that may be overdone because Ultra ASP/mix and camera feature positioning can sustain margins near-term — a post-launch pullback >5–8% in SSNLF/005930.KS could be a buying opportunity. Conversely, suppliers that booked bespoke Edge-panel lines could see asymmetric downside (20–40% downside if large order cancellations) — the market is underpricing forced inventory markdown risk for small-cap suppliers. Historical parallel: mid-cycle design cancellations (Samsung 2019–2020) produced short-term supplier stress but parent recovered within 2–3 quarters once mix normalized.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25