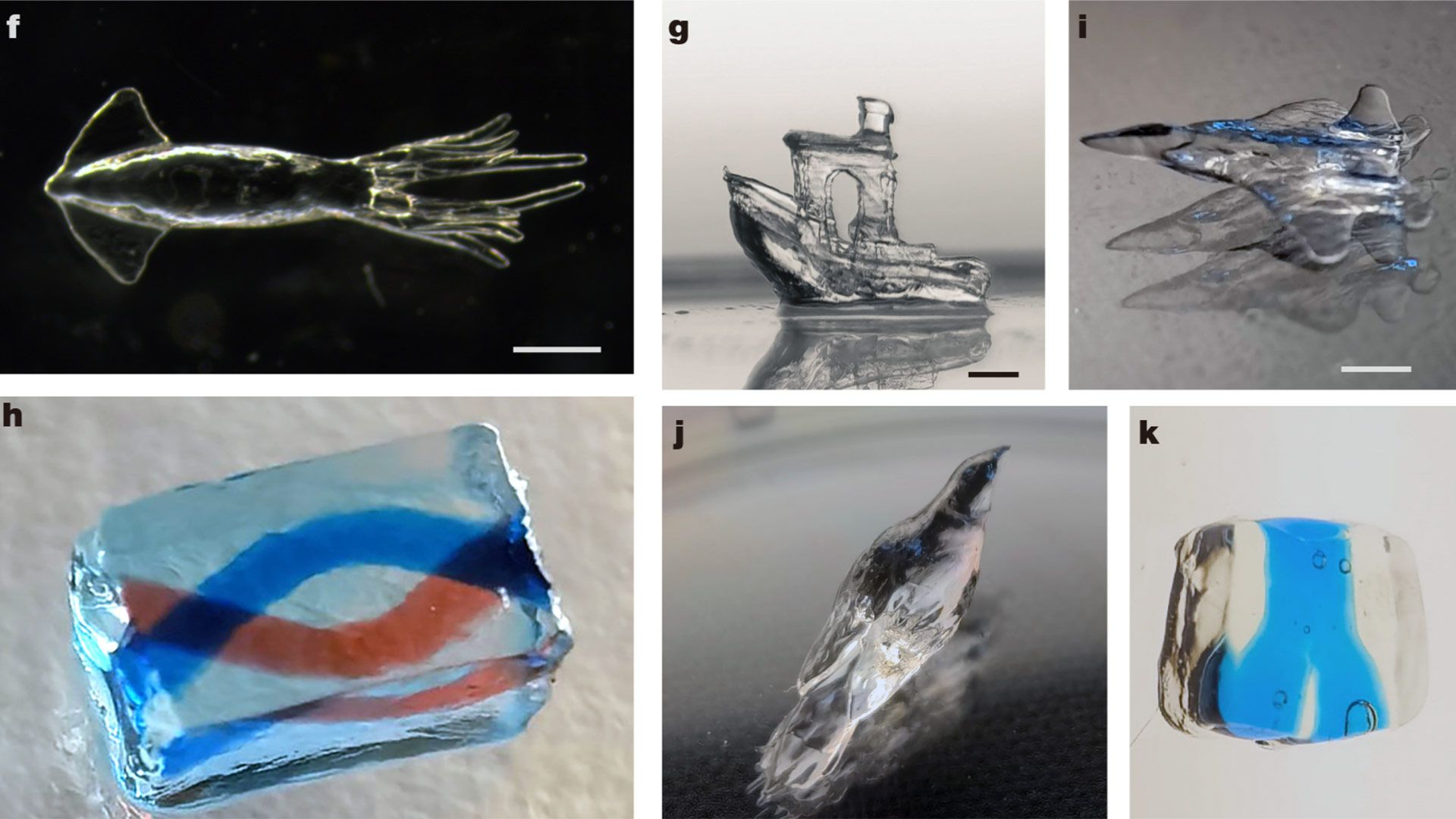

Tsinghua University researchers published in Nature a new volumetric 3D‑printing technique called digital incoherent synthesis of holographic light fields (DISH) that fabricates complex millimeter‑scale parts in as little as 0.6 seconds by rotating a high‑speed multi‑perspective light field around stationary resin rather than spinning the material. The team reports improved stability and accuracy versus traditional approaches and positions DISH as suitable for mass production of microcomponents — e.g., photonic computing elements and smartphone camera modules — with potential downstream applications in flexible electronics, microrobotics and high‑resolution tissue engineering.

Market structure: DISH materially expands the addressable market for millimeter- and micron-scale additive manufacturing — winners will be specialists in electronics-focused AM (Nano Dimension - NNDM), high-precision optics/laser suppliers (IPG Photonics - IPGP, II‑VI/Coherent/ IIVI) and resin/photochemistry producers; losers include high-volume injection molders and some legacy contract manufacturers (e.g., Flex - FLEX) for micro‑components. If DISH reaches commercial throughput, pricing power will shift to platform/IP owners and materials suppliers; expect downward pressure on per‑part costs for complex micro‑parts by 20–50% over 3–5 years as cycle time compresses from minutes to sub‑second for certain parts. Risk assessment: Key tail risks are IP and export‑control actions (10–25% probability over 12–24 months) and scaling/qualification of biocompatible resins (20–40% chance of multi‑year delay for medical use). Immediate effect is headline-driven equity volatility (days–weeks); meaningful commercial adoption and capex orders should be visible in vendor/order books in 6–18 months and revenue recognition in 12–36 months. Hidden dependency: success hinges on proprietary optics, high‑precision lasers and niche chemistries — shortage or price spikes in any can delay adoption. Trade implications: Tactical long exposure to NNDM (electronics AM) and selective optics/laser suppliers (IPGP/IIVI) is warranted; use 9–18 month call spreads to cap premium. Reduce/trim exposure to legacy precision contract manufacturers by 2–4% and rotate into industrial AM hardware/resin suppliers; accumulate on >15% pullbacks and target 30–100% upside depending on company and timeline (12–24 months). Options: buy NNDM 9–12 month call spreads 25–50% OTM sized at 1–2% NAV; sell covered calls on SSYS to fund carry. Contrarian angles: The street will over-index to “consumer printer boom” narratives — that is likely overdone; real value accrues in B2B microelectronics, photonics, medical components where TAM is smaller but margins higher. Historical parallel: SLA and DLP took 5–10 years to move from lab demos to industrial scale; expect a multi‑year commercialization curve, not immediate replacement of injection molding. Unintended consequence: rapid commoditization of some micro‑parts could compress OEM margins and create consolidation opportunities for well‑capitalized platform owners.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.33