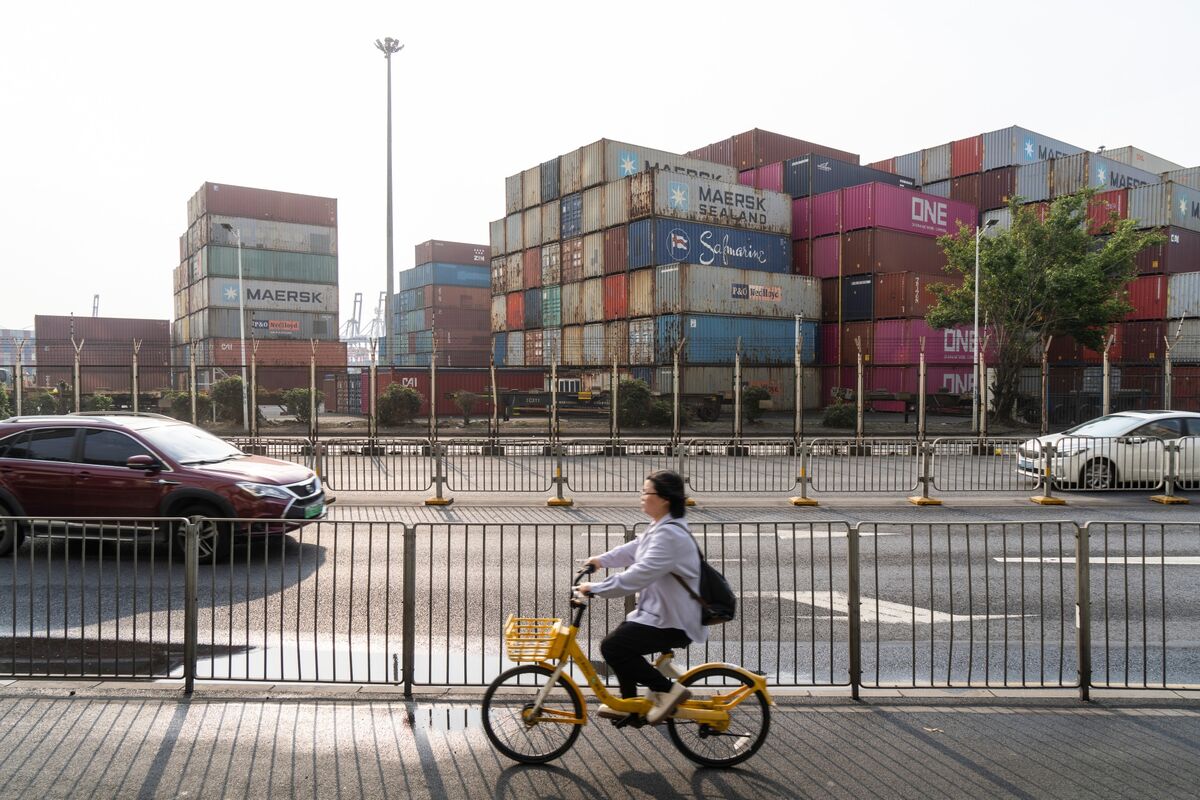

China said it will take countermeasures if the EU moves ahead with tougher restrictions on Chinese imports, escalating trade tensions between the two blocs. The warning comes as Brussels considers new curbs amid concerns over Chinese overcapacity. The rhetoric raises the risk of retaliatory trade actions that could affect autos, pharmaceuticals, wine and cosmetics.

This is less about the headline tariff threat itself and more about the signaling value: both sides are moving from dispute to pre-negotiation positioning, which tends to extend uncertainty rather than resolve it. That matters for European cyclicals with China exposure because valuation multiple compression usually starts before any actual tariff implementation, as supply-chain managers, distributors, and OEMs begin to build optionality into inventory and sourcing decisions. The first-order losers are the most China-dependent EU exporters, but the second-order loser set is broader: freight, industrial automation, and luxury/discretionary names that rely on Chinese end-demand can see slower order growth even if no formal measures arrive. The biggest near-term market effect is likely in relative performance rather than absolute price moves. Chinese policymakers have incentive to respond asymmetrically—targeting politically visible EU sectors where substitution is easier and domestic pain is limited—so investors should think in terms of product-specific pressure rather than a broad trade war beta shock. That makes autos, premium consumer goods, and some pharma supply chains vulnerable, while commodity-linked or domestically insulated European names may prove relatively resilient. The key catalyst is the sequencing over the next 2-8 weeks: rhetoric can de-escalate quickly if Brussels softens language, but once formal consultations or provisional duties are announced, the probability of retaliatory action rises sharply. A useful contrarian frame is that markets may be underpricing how quickly firms reroute intermediate goods through third countries, blunting the medium-term earnings hit, but overpricing the durability of current China demand for EU exporters if Beijing chooses selective retaliation. In other words, the risk is not a clean blanket tariff regime; it is fragmented, sector-specific friction that erodes margins and volumes quietly over several quarters.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35