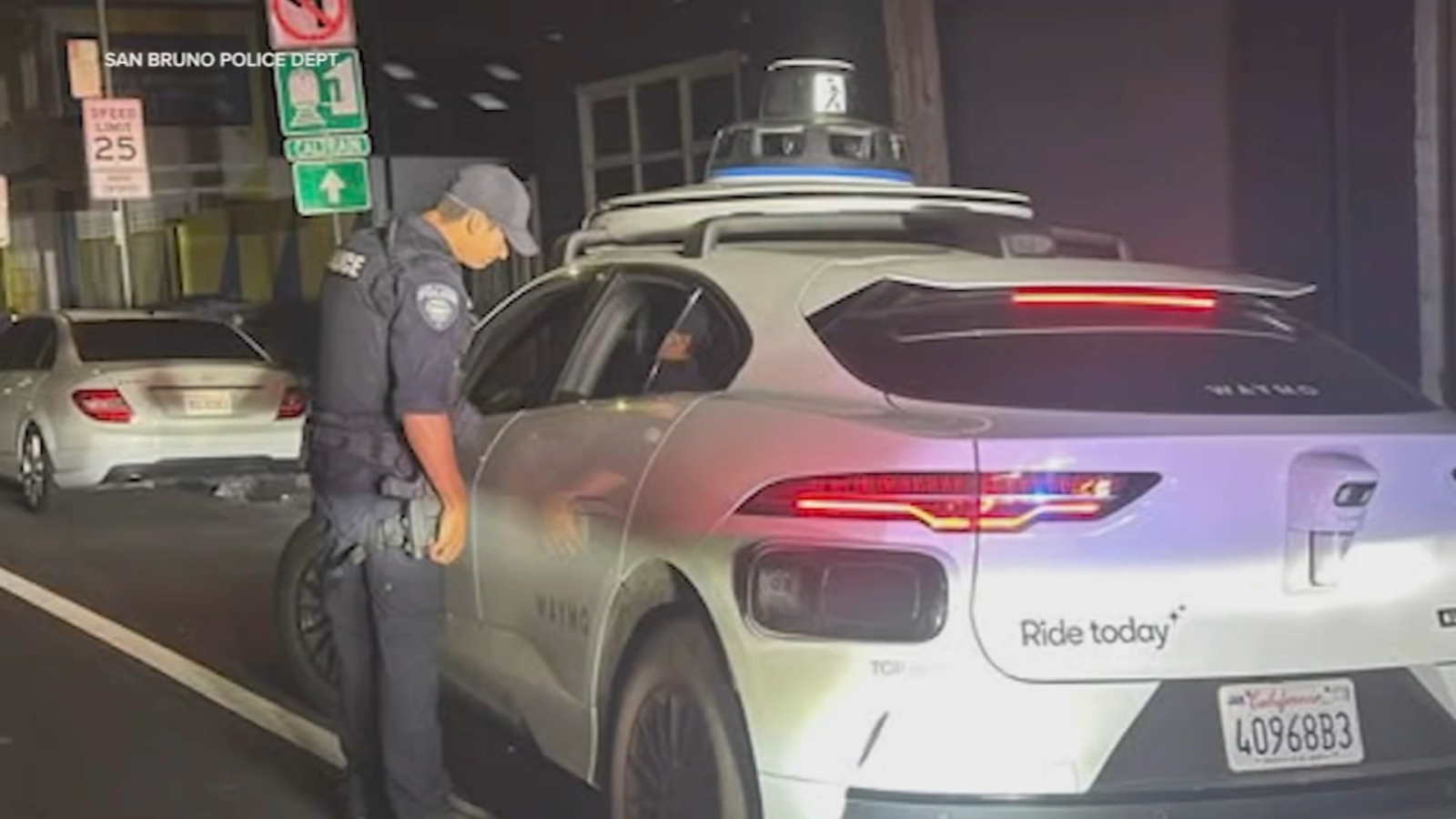

California’s DMV updated autonomous vehicle rules to allow police citations for moving violations even without a human driver, require AV companies to respond to first responders within 30 seconds, and let local officials restrict AV access during emergencies. The rules also open the door to broader testing of heavy-duty autonomous freight vehicles, a constructive development for Waymo and Aurora. Overall, the article points to clearer regulatory guardrails rather than an earnings or demand catalyst.

This is a margin-compression event disguised as a safety update. The biggest economic effect is not the citation itself, but the move toward treating AV fleets like regulated industrial operators: more compliance overhead, slower route optimization, and a higher probability that local restrictions fragment the serviceable map at precisely the moments when utilization is most valuable. That is modestly negative for unit economics across robotaxi platforms, but the damage is asymmetric: dense urban deployment is more exposed than highway freight, because city operations depend on uninterrupted access and reputation-driven expansion.

The more interesting second-order winner is autonomous freight. If California creates a clearer testing lane for heavy-duty AVs while city passenger fleets absorb more scrutiny, capital and engineering effort should tilt toward long-haul trucking where the ROI is easier to underwrite: 20+ hours/day utilization, fewer edge cases than urban driving, and better ability to scale via depot-to-depot routes. That likely accelerates competitive pressure on incumbent trucking labor, trailer leasing, and some brokerage models over the next 12-24 months, even if near-term deployments remain small.

Contrarian takeaway: the regulatory tightening may actually be constructive for the best-capitalized players. Smaller AV entrants and thinly funded pilots are more likely to fail under a regime that monetizes noncompliance and requires rapid response systems; the result could be a de facto moat for the few firms with dense mapping, legal infrastructure, and balance-sheet capacity. The market may initially read this as a drag on AV adoption, but the longer-term effect is likely industry consolidation rather than category retreat.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.05