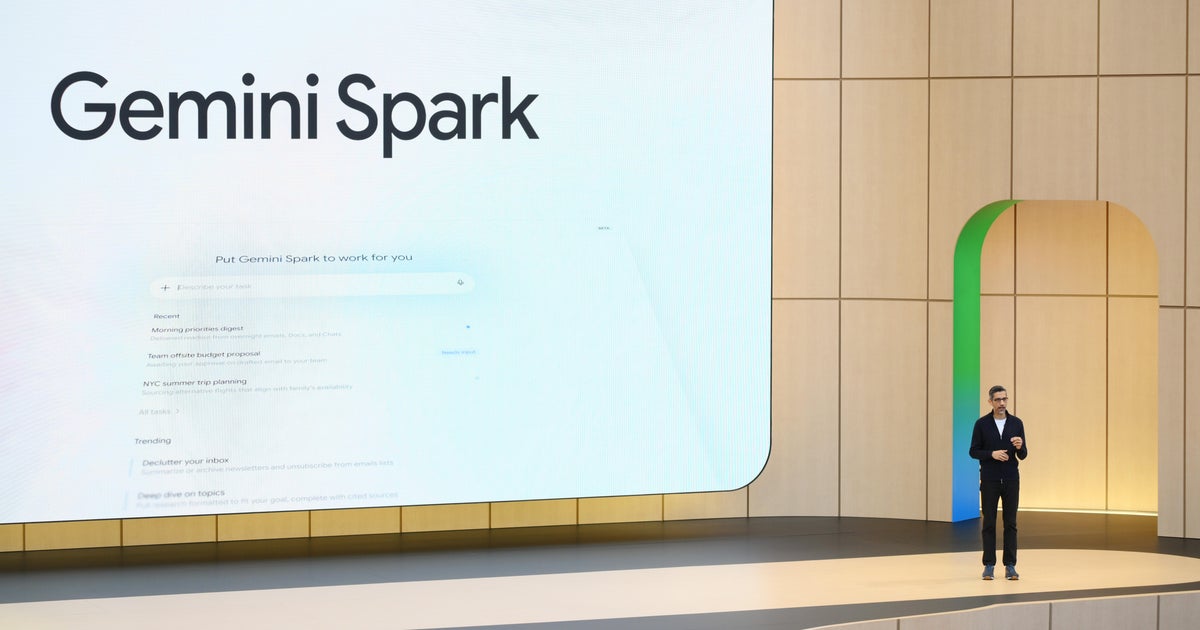

Google is rolling out Gemini Spark, an AI agent that can execute tasks across Gmail, Docs, Calendar and external services like Instacart and OpenTable, with Google AI Ultra subscribers gaining access next week at $100 per month. The article frames the product as a potential game changer because it can act on user context, but it also highlights privacy and permission risks around email access and high-stakes actions. Overall, the piece is constructive on Google’s AI roadmap but is primarily a product and industry commentary, not a direct market-moving event.

GOOGL’s edge here is not the chatbot layer; it’s distribution plus context. If agents become the new workflow surface, the company that already sits inside the inbox, calendar, documents, and commerce layer can monetize intent more efficiently than standalone model vendors, while lowering customer acquisition costs for agent subscriptions. The second-order effect is that this shifts value from generic LLM access toward operating-system-like control points, which is structurally bullish for platform owners and bearish for point solutions that lack native data access. The near-term market reaction should be modestly positive, but the bigger earnings inflection is months out: higher attach rates to premium AI tiers, lower churn in Workspace, and eventual transaction take-rate opportunities as agentic commerce matures. The risk is that agent usefulness is capped by permission friction and liability constraints; if users only allow low-stakes tasks, monetization remains more narrative than financial. That said, even partial adoption can increase switching costs because the agent learns personal patterns embedded in proprietary user data. The main contrarian miss is that privacy concerns could actually favor Google over pure-play competitors, not hurt it, because incumbent trust and default relationships matter when handing an agent inbox access and payment authority. The real losers are independent assistant startups and app-layer aggregators that depend on being the user’s primary interface. Over a 6-12 month horizon, the key catalyst is whether Google shows measurable usage in Workspace and consumer subscriptions rather than just demo-quality task completion. For catalysts, watch for evidence of transactional workflows expanding beyond drafting/summarization into reservation, shopping, and scheduling use cases. If adoption is real, the next leg is not multiple expansion alone but a re-rating of Google’s long-duration option value in agentic commerce and enterprise productivity.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment