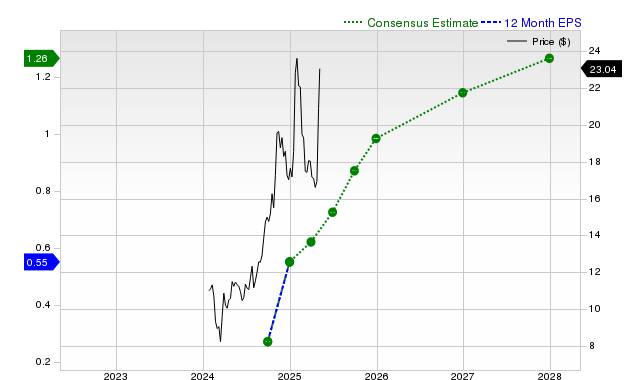

BrightSpring Health Services (BTSG) has seen material upward revisions to analyst earnings estimates, with the current-quarter EPS consensus at $0.34 (up 54.6% year-over-year) and full-year EPS at $1.12 (up 100% y/y). The Zacks Consensus estimate for the current quarter rose ~22.9% over the last 30 days (two upward revisions, none down) and the full-year estimate rose ~22.3% over the past month; the stock carries a Zacks Rank #1 (Strong Buy) and has gained 6.5% over the past four weeks. These coordinated analyst upgrades and positive momentum suggest upside potential for the equity as estimates are a key driver of near-term stock performance.

Market structure: The immediate beneficiary is BrightSpring Health Services (BTSG) and other home/behavioral-health services with Medicaid/Medicare exposure as analysts pushed forward EPS +22% in 30 days (current-quarter $0.34, +54.6% y/y; FY $1.12, +100%). Momentum suggests short-term pricing power via utilization or better payer mix rather than cost reductions; competitors with weaker reimbursement leverage or higher labor intensity will lose relative share. Cross-asset: positive BTSG news should tighten credit spreads for a subset of speculative-grade healthcare names and modestly depress implied equity vol; Treasury 2s/10s likely unchanged absent macro news but M&A chatter could lift leveraged loans. Risk assessment: Tail risks include CMS reimbursement cuts, post-earnings guidance downgrades, or labor cost spikes — each could erase current estimate gains and drop shares >30% within quarters. Immediate (days-weeks) risk is earnings/guide disappointment; short-term (1–6 months) depends on contract renewals and auditor/CG scrutiny; long-term (≥12 months) hinges on sustainable margin expansion vs. structural payor pressure. Hidden dependency: consensus lift may stem from 2 analyst revisions (fragile), not material operational inflection; catalysts are quarterly report, analyst notes, and CMS announcements. trade implications: Direct play: establish a starter long in BTSG (2–3% portfolio) and layer to 4–6% if post-earnings guidance confirms trends; set hard stop at -15% and take-profit at +30–50% over 6–12 months. Pair trade: long BTSG vs short iShares U.S. Healthcare Providers (IHF) to express idiosyncratic upside, weight 1:0.5 to moderate beta. Options: buy 6–9 month BTSG call spreads (e.g., buy 30–45 delta, sell 60–70 delta) to cap cost, or sell cash-secured 6-month OTM puts at ~10–12% below current price to collect premium if comfortable owning. Sector: overweight home/behavioral health operators, underweight hospital equipment and elective services. contrarian angles: Consensus may be over-extrapolating a short cluster of analyst upgrades into durable earnings power; +100% FY EPS projection looks like a high base-effect call and could reverse if one large contract or one-time item is removed. Reaction is likely underdone to downside — only +6.5% price move versus large EPS revision implies option skew could reprice quickly on a miss. Historical parallels: roll-up healthcare services often rerate on single-quarter beats then retrace after reimbursement scrutiny (example: past home-health consolidators). Unintended consequence: buy-side crowded long positions could trigger sharp liquidation on any negative CMS commentary within 30–90 days.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.65

Ticker Sentiment