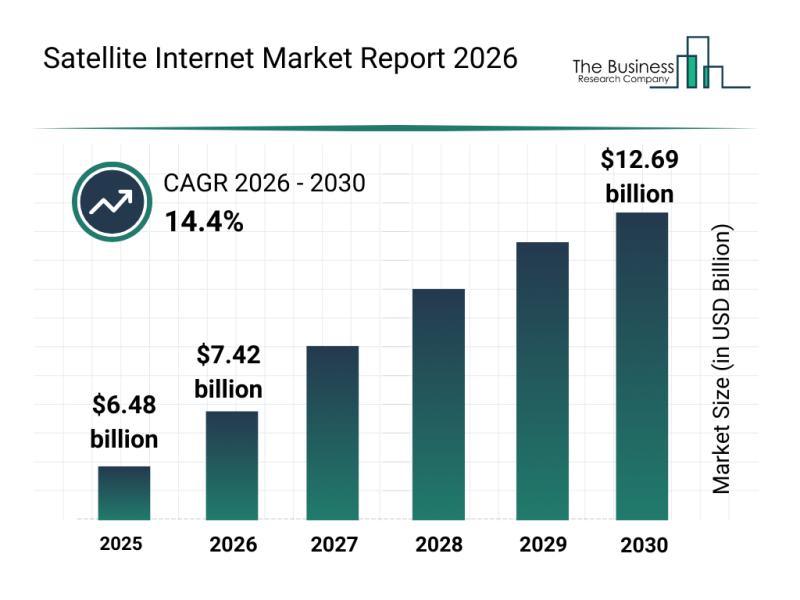

The satellite internet market is projected to reach $12.69 billion by 2030, implying 14.4% CAGR, supported by HTS deployment, LEO constellations, and faster broadband adoption. The article highlights a January 2024 EchoStar-DISH combination and SES's April 2024 launch of its second-generation O3b mPOWER system, which targets roughly 150 ms latency and multi-gigabit throughput. Overall, the piece is a constructive industry outlook rather than a near-term catalyst for broad market pricing.

The economic center of gravity is shifting from consumer broadband to a mix of enterprise mobility, defense, and backhaul. That matters because the winners are less likely to be the lowest-cost consumer ISP and more likely to be the operators with secure spectrum, government-grade SLAs, and the ability to sell into aviation, maritime, and tactical connectivity where switching costs are high and pricing power is real. The second-order effect is that equipment, launch, and ground-segment vendors can benefit before revenue inflects at the service layer.

The near-term competitive issue is capital intensity. LEO/MEO deployment rewards scale, but it also stretches balance sheets and creates a financing overhang for weaker operators that will need repeated capex cycles before cash flow turns self-funding. That makes this an uneven growth story: the market may continue to award optionality to platforms with credible constellation roadmap visibility while punishing businesses that still look like legacy bandwidth resellers.

A key contrarian point is that the market may be underestimating how much of the growth is already embedded in expectations for the obvious public names. The more asymmetric opportunity is in adjacent beneficiaries: operators with hybrid terrestrial/satellite integration, network integration software, and ground infrastructure exposure. Another underappreciated risk is service quality degradation during rapid scaling—congestion, terminal shortages, and latency variability can slow adoption in the very enterprise segments that justify premium valuations.

Catalyst timing is mostly months-to-years, not days. The next 6-12 months should be driven by proof of usable throughput, terminal economics, and backlog conversion rather than headline constellation launches. If adoption in defense and enterprise backhaul accelerates while consumer ARPU stays weak, the market will likely rotate toward names with recurring government and network-services revenue rather than pure-play consumer exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment