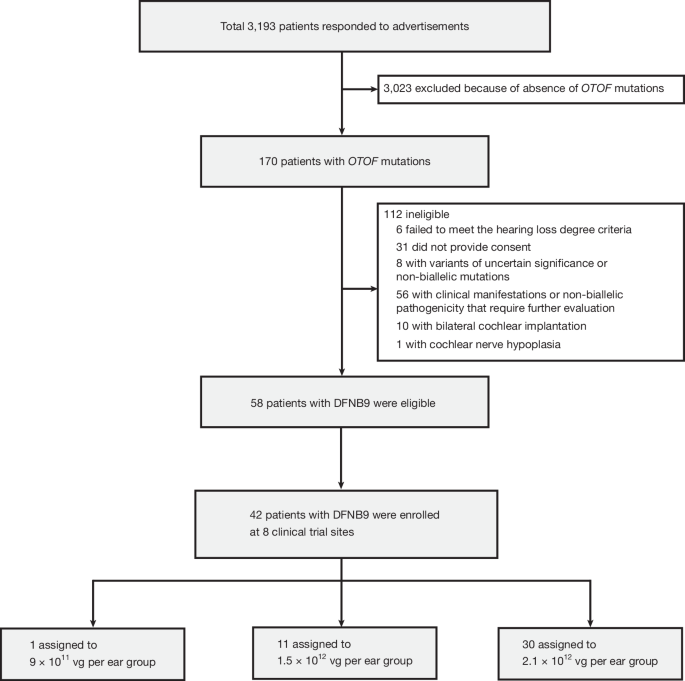

AAV1-hOTOF gene therapy for OTOF-related congenital deafness showed no dose-limiting toxicities in 42 participants and restored hearing in 90% of treated patients. Hearing thresholds improved steadily through 2.5 years, with better outcomes in younger patients and those with baseline DPOAE activity or biallelic non-truncated OTOF variants. The study supports sustained efficacy and tolerability, though the direct market impact is limited to the biotech/medtech space.

This is more important as a platform-validation event than as a single clinical readout. The key second-order effect is that the asset is moving from a “pediatric, narrow-label curiosity” toward something that could support a broader commercial framework: wider age inclusion, longer durability, and early biomarker-based responder selection. That lowers development risk not just for this program but for the entire class of inner-ear gene therapies, because it suggests the cochlea may tolerate AAV delivery better than skeptics assumed while still leaving room for meaningful functional recovery.

The biggest commercial lever is patient stratification. If baseline outer hair-cell function markers and genotype class can predict response, the market doesn’t need a perfect one-shot therapy; it needs a gatekeeping workflow that enriches for responders and improves payor economics. That creates a follow-on opportunity in diagnostics, sequencing, and audiology tools, and it also raises the bar for cochlear implant economics in this subpopulation because gene therapy can potentially delay or displace implantation in the best candidates, especially in younger patients where neuroplasticity still matters.

The main overhang is not efficacy, it is scalability and health-system friction. Treatment centers, surgical expertise, long-term monitoring, and antibody management are the bottlenecks, so adoption will likely look like a staged rollout over years rather than a step-function launch. Safety signals appear manageable, but any hematologic or inflammatory event in a small-disease, high-visibility pediatric population can meaningfully slow uptake if regulators demand post-marketing surveillance or repeat-dosing contingencies remain unresolved.

The contrarian read is that the market may still be underestimating how quickly this could become a template for adjacent monogenic sensory disorders. If one inner-ear gene program can demonstrate durable benefit across ages, the financing environment for rare-disease AAV could improve materially, but only for teams with strong delivery, manufacturing, and patient-finding capabilities. The economic winners may ultimately be the enabling layer — genetics diagnostics, surgical delivery infrastructure, and select platform biotech names — rather than the first commercial product itself.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.72