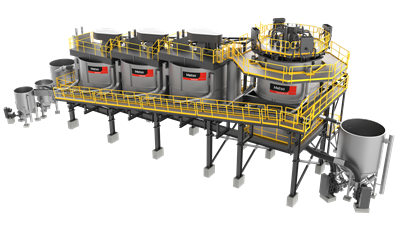

Barrick Gold has selected Metso’s Concorde Cell flotation technology for the Lumwana copper expansion in North-Western Province, Zambia, to be integrated with previously chosen TankCell equipment; the Concorde Cell order was recorded in Metso’s Minerals segment 2025 Q3 order intake. The forced-air pneumatic Concorde Cell is designed to boost flotation kinetics and recovery of fine and ultra-fine particles, reinforcing Metso’s minerals equipment backlog and technology positioning (Metso reported ~EUR 4.9bn sales in 2024). The contract underscores continued capital spending on copper processing infrastructure in emerging markets and is a modest positive for Metso’s equipment franchise, though unlikely to be material market-moving news on its own.

Market structure: Barrick's selection of Metso’s Concorde Cell for Lumwana is a microeconomic efficiency gain — faster kinetics and better fine-particle recovery imply 3–8% higher concentrate yield and/or lower unit milling costs vs legacy cells (industry heuristic). Direct winners are Barrick (ABX.TO) via lower AISC per lb and Metso via equipment revenue and aftermarket services; marginal losers are lower-tech flotation suppliers and high-cost copper peers who can’t match throughput improvements. Expect modest copper supply-side tightening from higher recoveries at large projects (Lumwana-scale), supporting copper prices if similar retrofits roll out across industry over 12–36 months. Risk assessment: Tail risks include Zambian political/regulatory shocks (license/royalty changes), a >12–18 month construction/commissioning delay, or a sharp >25–30% copper price drop that would negate incremental margin gains. Short-term (days–weeks) market impact will be muted; short-to-medium (3–12 months) effects materialize as equipment deliveries and commissioning milestones are met; medium-to-long (12–36 months) will show realized production uplift. Hidden dependencies: project financing, power/water access in NW Zambia, and Metso’s execution/capex schedule; watch Q2–Q4 supplier order backlogs as a leading indicator. Trade implications: Tactical long in ABX.TO captures project-specific upside; consider defensive allocation to industrial OEM suppliers (Metso) to play service annuity upside. Use relative-value pair trades to isolate project execution (long ABX.TO vs short high-cost copper peer like FCX) and option-call-spreads to cap premium while preserving upside. Rotate modestly into Materials and Industrial Tech over 3–12 months, trimming cyclical long-only commodity exposures if copper rallies >20%. Contrarian angles: Market may underweight engineering tech as an earnings lever — Metso aftermarket/service margins could expand by 100–200 bps if Lumwana generates multi-year service contracts, which is underappreciated. Conversely, consensus may under-price Zambian sovereign-operational risk: a regulatory shock or prolonged local outage could wipe >30% of project NPV. Historical parallel: supplier-driven recovery gains (e.g., SAG/HPGR upgrades) often redistributed 5–15% of free cash flow toward operators and OEMs, not commodity traders; expect a similar asymmetric benefit here.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment