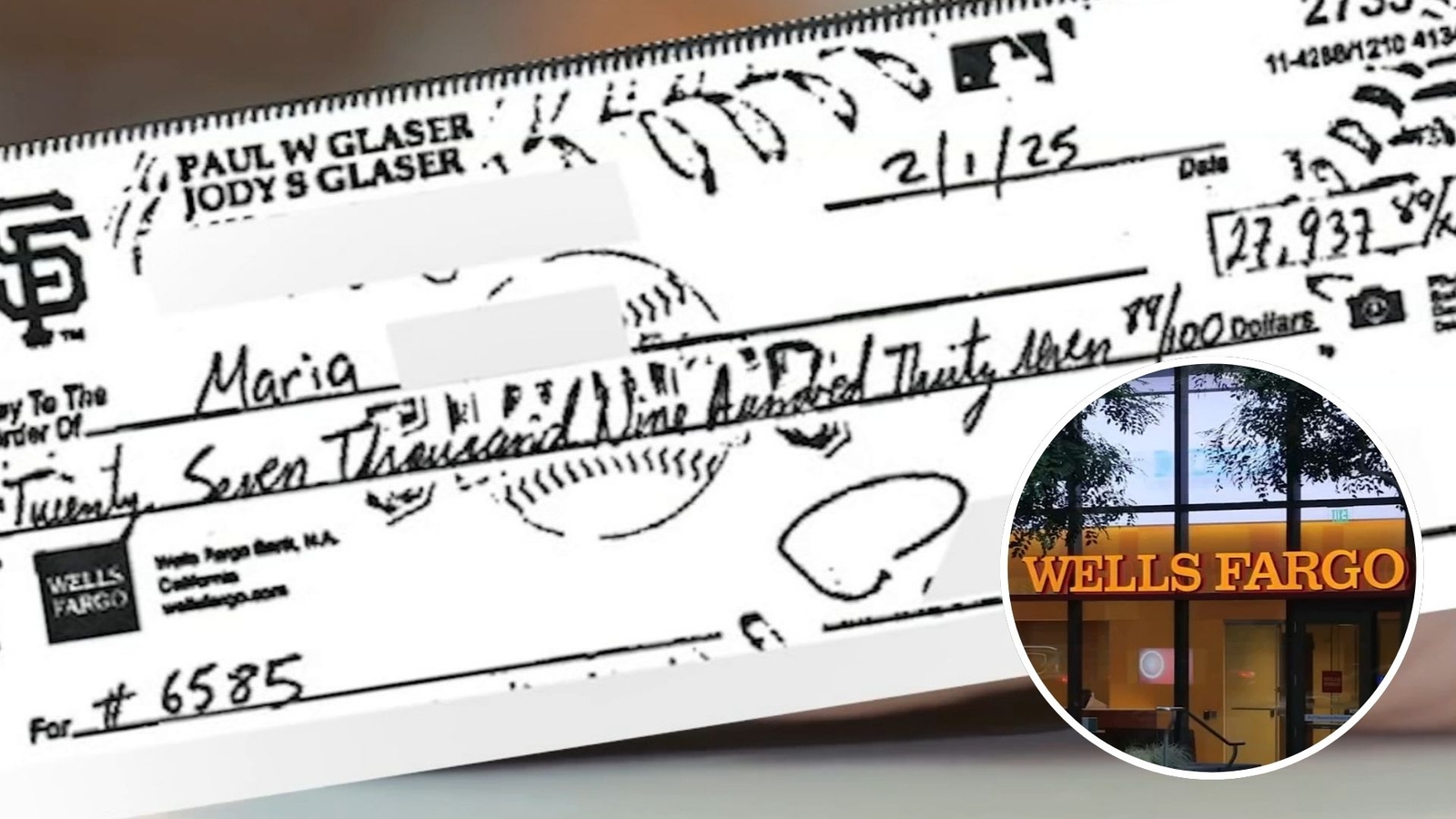

Two Northern California homeowners lost large property-tax payments after mailed checks were stolen, chemically altered and cashed by criminals — one victim lost $2,400 and another couple nearly $28,000 and subsequently paid roughly $30,000 more in taxes and penalties. Wells Fargo denied the couples' reimbursement claims citing a 30-day customer reporting requirement and a (recently clarified) obligation to review check images, though it later refunded one customer after media attention; the cases highlight operational, reputational and legal risk for banks and underscore a push toward electronic payments and potential regulatory scrutiny of disclosure and dispute-handling practices.

Market structure: Recent mail‑check fraud stories are a negative idiosyncratic shock to retail banks—Wells Fargo (WFC) in particular—raising expected operational losses and reputational cost. Expect incremental compliance/legal expense of 1–5% of quarterly EPS if state AGs or CFPB open investigations within 3–6 months; conversely card networks (V, MA) and digital bill‑pay providers should see modest share gains as consumers shift electronic, improving revenue mix over 6–24 months. Risk assessment: Tail risks include a multi‑state class action or CFPB enforcement forcing industry‑wide refunds/reserves (low prob, high impact — potential hit 2–7% CET1 for a large bank if precedent expands). Near term (days–weeks) market reaction will be reputational and volatility spikes; short‑term regulatory catalysts over 30–90 days matter most, while long term (quarters) the structural shift to electronic payments and fraud‑prevention spending is durable. Trade implications: Direct short pressure on WFC is justified tactically; option vol for WFC likely cheapens puts during headline cycles—consider small, time‑bounded hedges. Buy payments processors (V, MA) and cybersecurity names (CRWD, OKTA) as beneficiaries of payment digitization and fraud‑prevention budgets over 3–12 months. Contrarian angle: The market may over‑penalize WFC relative to expected loss magnitude—these are operational losses, not credit losses—so a disciplined short should be size‑limited and event‑driven. Historical parallels (1990s check fraud) show rapid consumer migration to electronic rails; winners may be priced for growth already, so prefer high‑quality compounders of payments volume rather than speculative fintechs.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.60

Ticker Sentiment