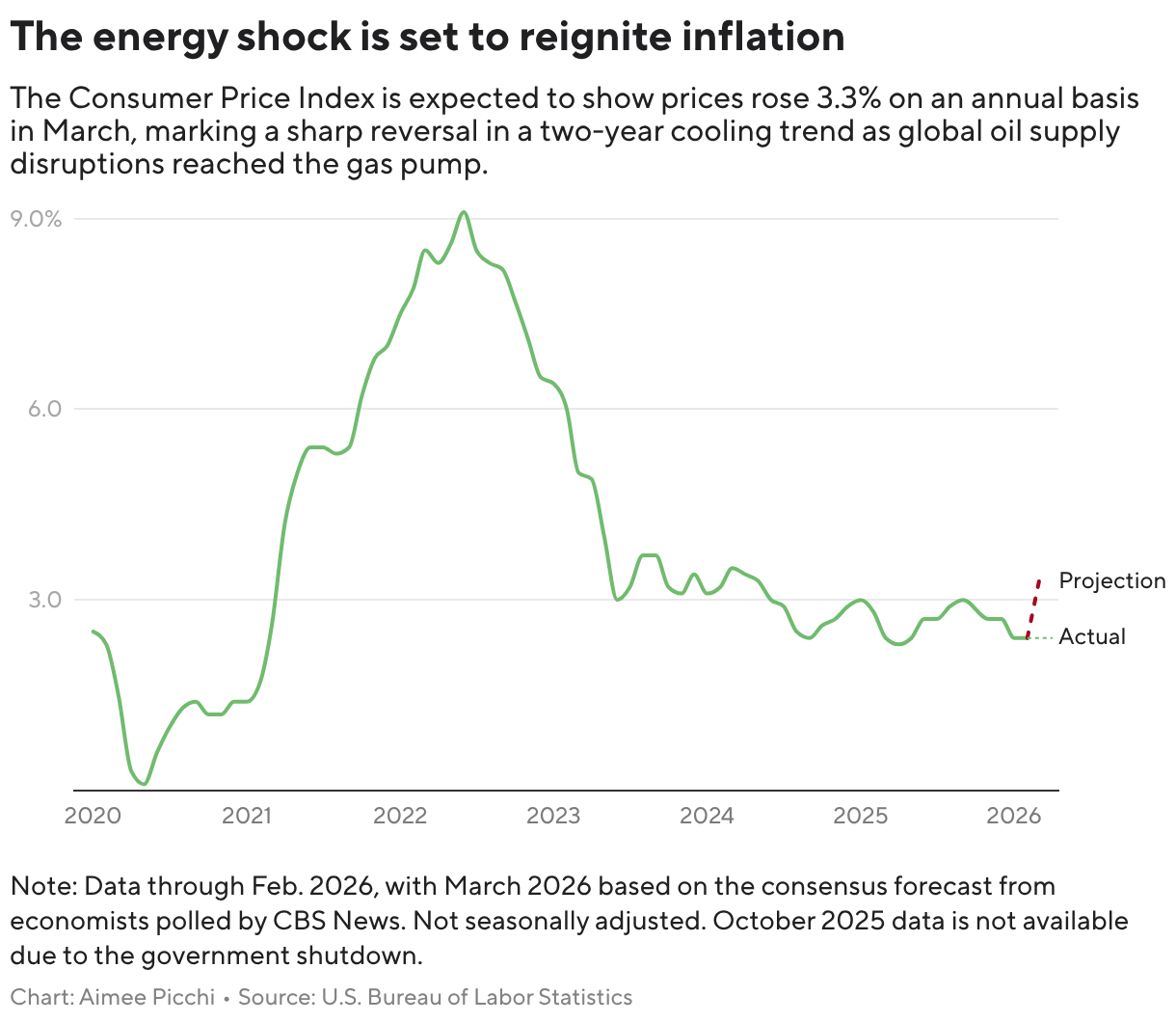

April PCE inflation is expected to rise 3.9% year over year, the highest reading for the Fed's preferred gauge since May 2023, increasing pressure on new Chair Kevin Warsh to keep policy restrictive. Economists say steady labor markets and sticky inflation could push the Fed toward holding rates through 2026, with CME FedWatch implying a 40% probability of a December hike versus 3% in June. The article also highlights political tension as President Trump presses for lower rates while Warsh emphasizes Fed independence and a reform agenda.

The market is underpricing the asymmetry between a one-month inflation print and a regime shift in Fed reaction function. If inflation stays sticky while labor remains intact, the next policy move risk migrates from cuts to hikes, which is a much sharper repricing for duration than a simple delay of easing. That matters because long-end rates can back up even if the policy rate is unchanged: term premium rebuilds fast when investors start pricing a less-dovish chair plus a more politically constrained central bank. The first-order beneficiaries are cash-flow duration shorteners: banks with asset-sensitive balance sheets, value/financials, energy-linked credit, and firms with limited reliance on cheap refinancing. The more interesting second-order loser set is growth stocks that have been levered not just to rates, but to the belief that the Fed would cushion macro volatility; software, unprofitable tech, and small-cap indices are vulnerable to multiple compression if the market begins to price policy inertia or an eventual hike. A hotter inflation print also increases the odds that real yields rise faster than nominal growth expectations, which is usually the most hostile cocktail for high-P/E equities. The contrarian risk is that markets may be overfitting a single inflation data point to a sustained hawkish regime. If the oil impulse proves temporary, headline inflation can decelerate quickly while the Fed keeps sounding tough, creating a window where nominal yields overshoot fundamentals and risk assets stabilize. In that scenario, the best trade is not a blanket equity short but a barbell: short duration and lower-quality equities, while keeping some exposure to beneficiaries of resilient nominal growth and steeper curves. For the next 2-6 weeks, the key catalyst is whether the Fed changes its communication framework more than its actual rate path. Any move away from explicit projections would reduce forward-guidance value and increase data dependency, making every CPI/PCE release more market-moving than usual. That lifts realized volatility across rates and equity factors even before the committee moves.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.15