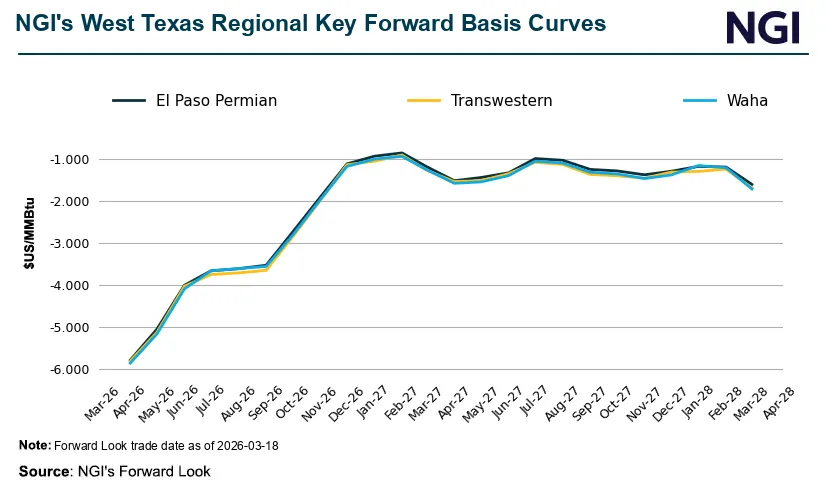

U.S. natural gas forward prices fell over the past week as strong production, healthy storage inventories and the approaching shoulder season outweighed escalating Middle East tensions. Declines were strongest in the Northeast, while rising crude prices put additional pressure on Waha basis differentials.

Lower forward gas strips are already reshaping incentives across the value chain: producers face deferred drilling and capital rationing within 3–12 months, while downstream consumers (petrochemicals, fertilizers, industrials) get a multi-quarter margin tailwind that can translate into faster cash conversion and opportunistic buybacks. Midstream dynamics bifurcate — fee-based trunklines see stable volumes, but regional basis spreads and optionality value (e.g., Permian/Waha) compress, transferring economic pain to basin-level producers and price-insensitive takeaway bottlenecks. Volatility compression around the forwards reduces realized vol for storage/service merchants and option sellers, but it also makes short-dated volatility a crowded trade that will reprice violently on any supply shock.

Key catalysts that could reverse the current drift come in three flavors and timeframes: (1) weather shocks (days–weeks) — a 2–3 standard-deviation cold snap would blow out prompt spreads and force producers to scramble, (2) LNG demand shocks (weeks–months) — faster-than-expected European or Asian draw will pull U.S. exports and tighten balances over a 1–6 month window, and (3) structural supply adjustments (6–24 months) — sustained price weakness will curtail US drilling and FID on incremental gas-focused projects, creating a scarcity move thereafter. Tail risks include major pipeline outages or a geopolitical event that sterilizes LNG flows; these create non-linear upside to short-dated calls but are low probability and hard to hedge with cash equities alone.

Consensus is underweight optionality: markets are pricing a long, slow mean reversion driven by inventories, but they underprice the asymmetry of colder-than-expected winters and the speed at which LNG re-routing can flip flows. That makes insurance-like instruments (out-of-the-money winter calls, calendar call spreads) attractive as cheap convexity. Conversely, pure equity shorts in basin producers are not free carries — unexpected warm winters or incremental rate-of-return-driven hedging programs by producers can limit downside over 1–3 months, so prefer defined-risk structures rather than naked short equity exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25