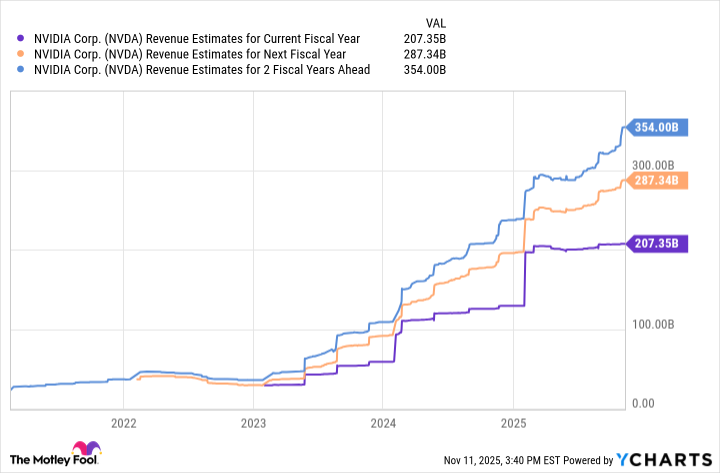

Nvidia's CEO Jensen Huang recently revealed a substantial $500 billion order book for its new Blackwell Ultra and Rubin GPUs, anticipated over the next five quarters, which initially boosted its market cap past $5 trillion. While the company's finance team later clarified that this figure isn't formal guidance and includes previously shipped units, with a more accurate backlog estimated at $307 billion over the next year, the immense demand still highlights Nvidia's unparalleled position in AI infrastructure. This sustained growth, with the data center division now surpassing the company's pre-AI annual revenue, suggests analysts may be underestimating Nvidia's future revenue trajectory, making its current forward P/E of 30 appear undervalued given its robust sales pipeline.

Nvidia's CEO Jensen Huang announced a staggering $500 billion order book for its new Blackwell Ultra and Rubin GPUs, expected over the next five quarters, during the GTC Conference. This revelation propelled Nvidia's market capitalization past $5 trillion, reflecting significant investor enthusiasm for its continued dominance in AI hardware. The company's transformation from a gaming-focused chip designer to a fundamental AI data center supplier has created an unparalleled virtuous cycle of demand and reinvestment. However, Nvidia's finance team subsequently clarified that the $500 billion figure is not formal guidance and includes approximately 30% of Blackwell chip demand already shipped and recognized. The more accurate, trued-up backlog is estimated at $307 billion, anticipated over the next year, contingent on stable supply chains and customer capital expenditures. This adjustment provides a more nuanced financial picture, distinguishing between headline figures and recognized revenue. Despite the clarification, the sheer scale of the $307 billion backlog remains highly significant, dwarfing Nvidia's pre-AI annual revenue of less than $30 billion. This robust demand suggests that sell-side analysts may be underestimating the future revenue growth from AI infrastructure, potentially leading to Nvidia's trajectory outpacing Wall Street expectations. The author posits that Nvidia's forward price-to-earnings ratio of 30 appears "pedestrian" in light of its expanding profitability and strong sales pipeline.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.80

Ticker Sentiment