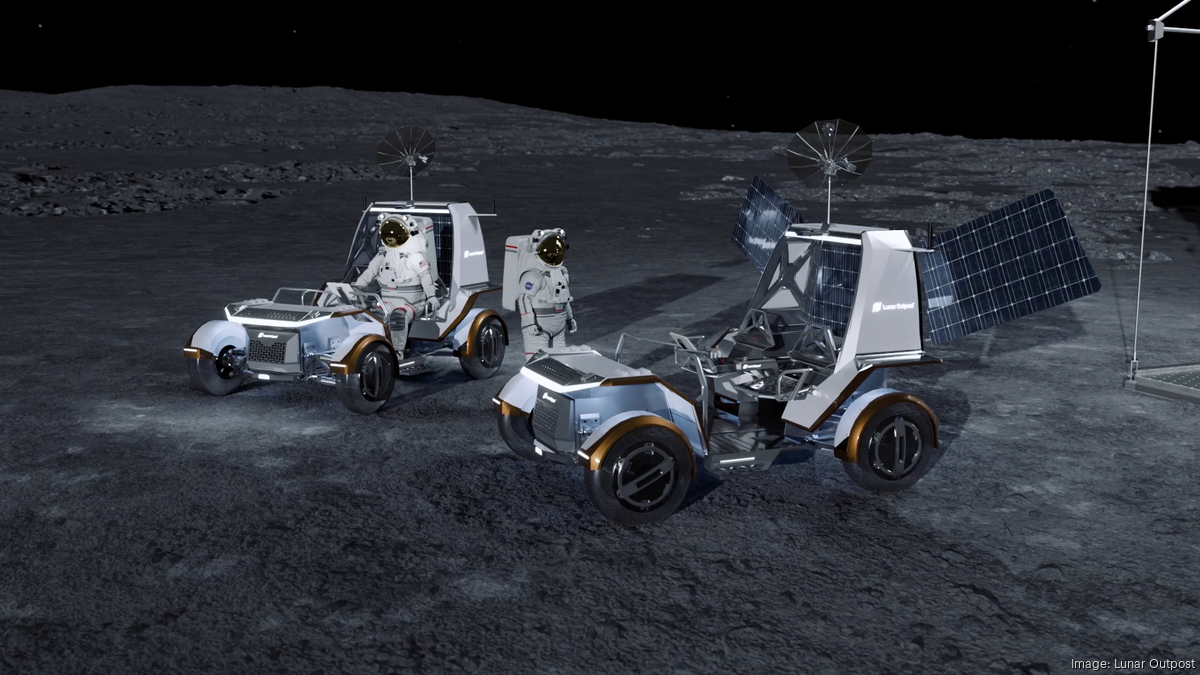

The article says the award was part of NASA’s mission to build a viable lunar economy and sustain human presence on the moon by 2030. It highlights recognition of a small business in connection with lunar commercialization and space infrastructure efforts. The piece is largely descriptive and does not provide financial figures or immediate market-moving catalysts.

This is less about a single prize and more about signaling where federal capital will likely crowd in over the next decade: lunar logistics, robotics, power systems, comms, and autonomous operations. The beneficiaries are the boring picks-and-shovels players that can translate space-adjacent R&D into defensible government revenue, not the headline-startup layer that wins awards but still lacks production-scale procurement. The real second-order effect is that a “lunar economy” narrative lowers perceived technical risk for adjacent terrestrial dual-use technologies, which can expand valuations in small-cap aerospace, advanced materials, and autonomy platforms even before actual lunar spending ramps. The key competitive dynamic is that space is becoming more of an infrastructure procurement market than a pure exploration market. That favors incumbents with compliance, integration, and program-management depth, while hurting pure-play venture names that need repeated raises to bridge the 5-10 year commercialization gap. If NASA’s roadmap stays intact, expect more value capture to accrue to subsystem vendors, launch enablers, and data/communications layers than to any single mission winner. The contrarian risk is that “lunar economy” optimism can outrun budget reality; these programs are vulnerable to continuing resolutions, election-cycle reprioritization, and one-off mission delays. In the near term, sentiment can stay positive for weeks, but cash-flow impacts are measured in years, so any trade should be sized as a long-duration optionality bet rather than a fundamentals call. The main reversal trigger is a shift from moon-to-mars rhetoric back toward nearer-term defense and ISS-style spending, which would compress the multiple expansion in venture-linked space names. For investors, the better expression is a basket trade on the infrastructure layer rather than a single moonshot name. The cleanest long is a space/defense integrator versus a venture-heavy unprofitable aerospace peer, because the former benefits from procurement visibility while the latter depends on funding windows. Options can be used to monetize the narrative without overcommitting capital, since the payoff is asymmetric but the timing is highly uncertain.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.20