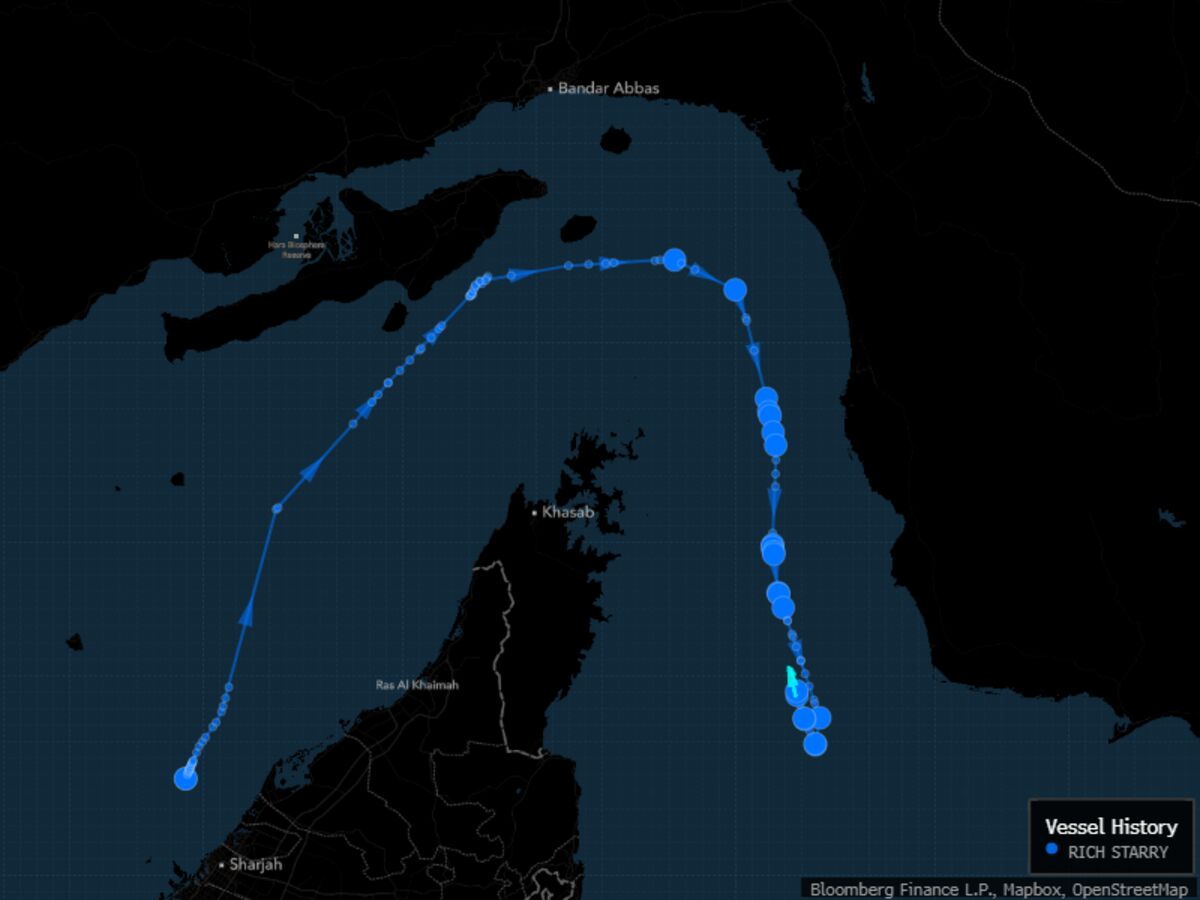

A US-sanctioned tanker linked to China, Rich Starry, crossed the Strait of Hormuz and then appeared to U-turn after sailing out, highlighting immediate risk around Iran-related maritime flows. The vessel was blacklisted by Washington in 2023 for helping Tehran evade energy sanctions. The episode underscores geopolitical tension in a critical oil shipping chokepoint and could keep freight and energy risk premiums elevated.

The key signal here is not the vessel itself, but the fact pattern it implies: even a small, visible reversal by a sanctioned tanker can indicate that the market is already pricing a meaningful probability of interdiction, delay, or inspection risk. That tends to show up first in spot freight and insurance before it is obvious in outright crude prices, so the cleaner tradeable spread is often maritime risk premia versus broad energy beta.

Second-order, the biggest winners are not necessarily the obvious oil longs. LNG and refined-product routes with lower Strait exposure can capture diversion demand, while shipowners with compliant fleets and stronger war-risk coverage can gain bargaining power as charterers scramble for alternatives. The losers are sanctioned-linked shipping intermediaries, smaller tanker operators with weak compliance infrastructure, and Asian refiners most dependent on Middle East barrel flow and just-in-time inventory.

The timeline matters: over days, headlines can whip crude but shipping and insurance rates are the faster reflexive indicators; over months, persistent blockade fear can widen Brent-Dubai and support backwardation, but a single de-escalatory signal would unwind that premium quickly. The main catalyst that reverses the move is not necessarily a formal policy shift — it could simply be credible evidence that transit remains permissive, which would compress war-risk and freight add-ons faster than outright crude.

Contrarian view: the market may be over-focused on a visible test and underestimating how quickly participants adapt via routing, transshipment, AIS discipline, and fleet segmentation. If the incident proves isolated, crude upside from this headline is likely capped, while the more durable opportunity is in relative-value dislocations across shipping, refiners, and non-Middle East supply chains rather than a directional energy macro bet.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25