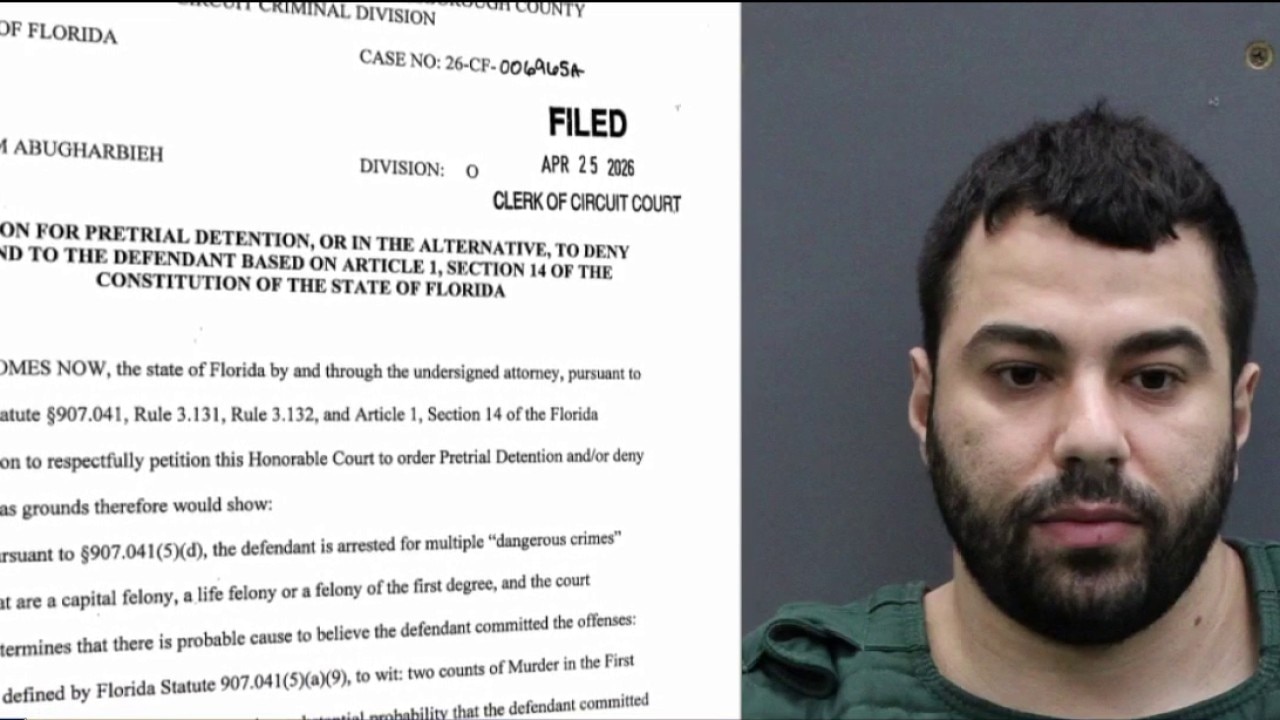

Court documents and family accounts allege warning signs and ignored complaints at Avalon Heights before the killings of two University of South Florida doctoral students. The article says the suspect had prior violence-related charges and that residents/families are questioning background checks, security, and the housing complex’s response. The case remains active, with the suspect in custody and investigators seeking additional evidence.

This is a governance/liability story first and a real-estate story second. The immediate economic damage is not to a public ticker list but to the operating model of private student-housing platforms: if a resident with a documented volatility history remained in place after complaints, the market will increasingly price in a higher cost of resident screening, security staffing, incident response, and insurance. The second-order effect is a widening dispersion between professionally managed, institutionally capitalized operators and lightly supervised local landlords, because the former can absorb compliance costs while the latter face rising litigation and reputational risk.

The broader read-through is a likely re-rating of anything exposed to “duty of care” claims: student housing, multifamily, and adjacent private dorm operators may see lenders tighten underwriting and insurers reprice umbrella and general liability coverage over the next 6–18 months. Even without a named public company, the event creates an earnings headwind via higher reserves, lower occupancy velocity, and slower lease-up as families become more sensitive to management quality and security credentials. The biggest underappreciated impact is on asset managers: if this becomes a template case, boards will push for more conservative resident selection and more documented incident escalation, which lowers operational flexibility and raises overhead.

The contrarian view is that the market may over-penalize the entire student-housing complex for what could become a localized management failure. If the facts show the incident was primarily a violent outlier rather than a systemic screening breakdown, then this may produce a short-lived sentiment hit rather than a structural demand issue. The real catalyst to watch is litigation discovery: if internal emails show ignored complaints or under-resourced security, that would convert reputational damage into a durable underwriting problem for the sector.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60