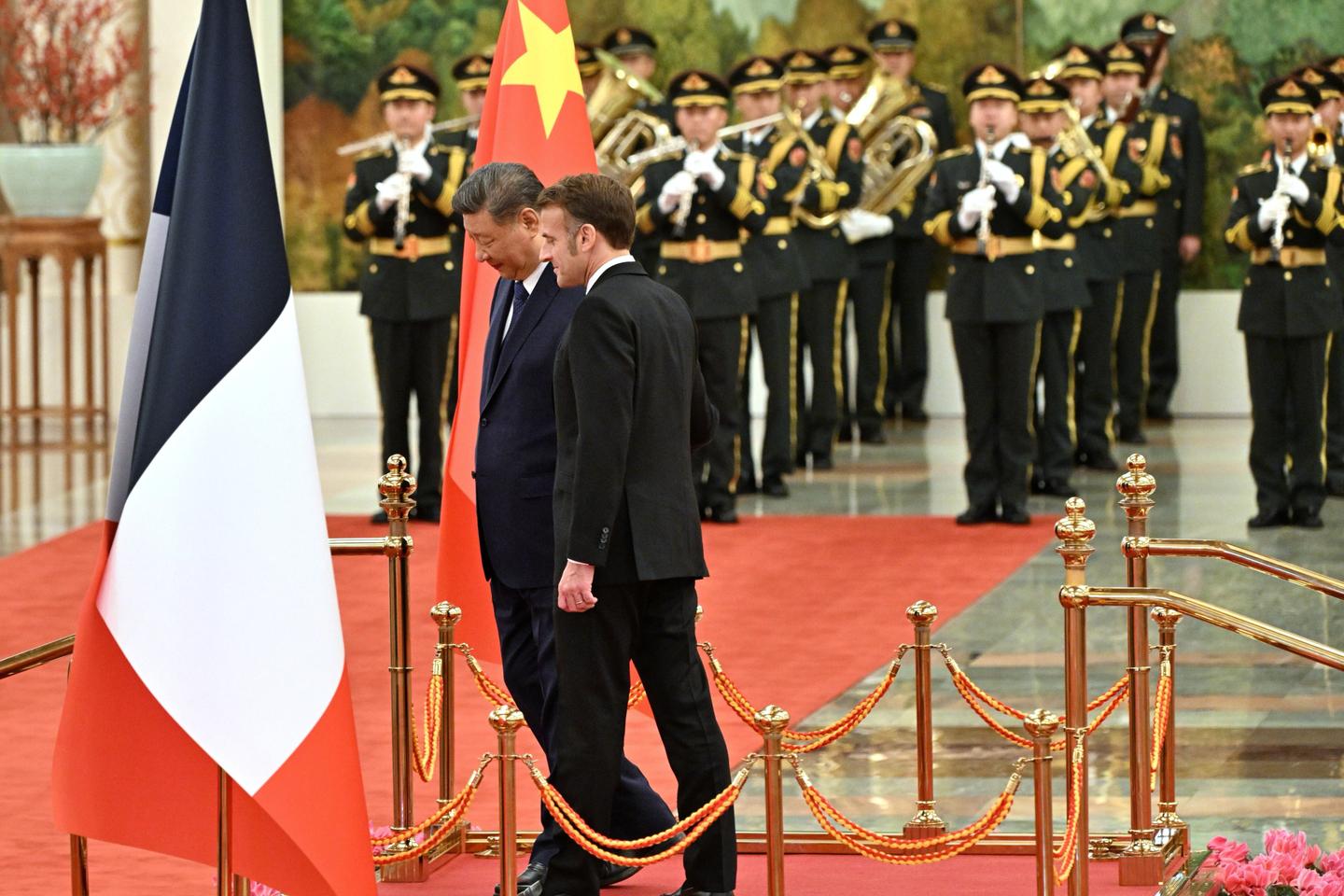

French President Emmanuel Macron met Xi Jinping in Beijing to press China to back efforts for a ceasefire in Ukraine and to address large trade imbalances, with France's trade deficit with China cited at €46 billion in 2024 and the EU's deficit with China around $357 billion. Macron pushed Beijing to refrain from supplying Russia with means to continue the war and sought greater Chinese investment and cooperation on rules-based economic governance ahead of hosting the G7; no immediate policy shifts or market-moving commitments were announced, but the discussions highlight diplomatic pressure points that could influence future trade, sanctions enforcement and bilateral investment flows.

Market structure: Macron’s Beijing visit signals a calibrated attempt to convert diplomacy into incremental trade and investment flows rather than a dramatic policy pivot. Winners in a modest rebalancing: European exporters to China (luxury, autos, agri-machinery) and French asset classes if even €5–15bn of targeted Chinese FDI materializes over 12–24 months; losers include global commodity exporters if China increases imports at lower global margin or if Russia redirects energy to China. FX and credit: successful rapprochement should tighten French sovereign spreads by 5–15bp and support EUR vs CNY/USD over 3–12 months. Risk assessment: Tail risks include a diplomatic breakdown that pushes China closer to Russia (high-impact) or EU domestic political pushback that blocks Chinese takeovers (mid-probability). Immediate (days) market moves likely muted; short-term (weeks–months) volatility around G7 and any announced MOUs; long-term (quarters–years) structural risks from EU tech “European preference” policies could fragment global supply chains and raise capex for EU semiconductors and machinery. Hidden dependencies: Chinese dual-use supply to Russian defense and EU political tolerance for FDI are binary catalysts. Trade implications: Tactical trades favor long selective French/European consumer and industrial exporters and long EUR, with hedges against geopolitically driven defense upside. Use 6–18 month call spreads on top luxury names and 3–12 month EUR/USD directional positions sized to portfolio risk limits. Avoid one-way longs on China large-cap exporters without clear evidence China will rebalance exports vs domestic consumption within 12 months. Contrarian angles: Consensus treats this as symbolic; miss is the speed at which targeted FDI and procurement deals (ports, aerospace maintenance, luxury JV) can reallocate revenues — a few €bn deals can lift specific mid-cap French equities 20–40% vs peers. Conversely, markets underprice the regulatory rollback risk in France/EU (foreign investment screens) which can derail M&A and create short opportunities in stocks that priced-in Chinese bids.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00