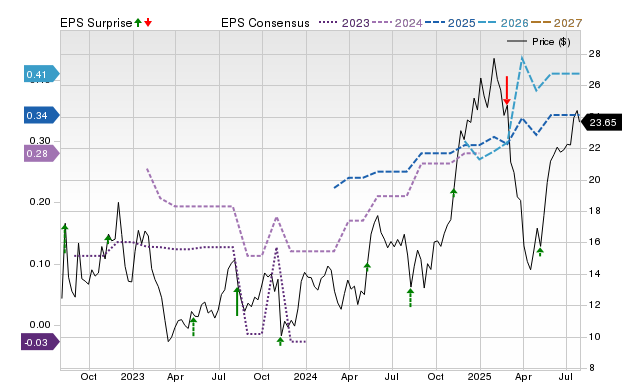

Warby Parker (WRBY) is projected to report Q2 2025 earnings of $0.09 per share (+50% YoY) and $212.8 million in revenue (+13.1% YoY) when it releases results on August 7. Despite these consensus growth expectations, Zacks' analysis suggests a low probability of an earnings beat, citing a negative Earnings ESP of -11.11% and a Zacks Rank of #4. This combination, alongside a history of only one EPS beat in the last four quarters, indicates that WRBY is not a strong candidate for a positive earnings surprise, potentially limiting upside ahead of the report.

Warby Parker (WRBY) is approaching its Q2 2025 earnings release on August 7 with high consensus expectations, including a projected 50% year-over-year increase in EPS to $0.09 and a 13.1% rise in revenue to $212.8 million. Despite this optimistic top-line and bottom-line growth forecast, several quantitative indicators suggest a heightened risk of the company failing to meet these targets. The stock carries a Zacks Rank of #4 (Sell) and a negative Earnings ESP (Expected Surprise Prediction) of -11.11%, a combination that historically makes it difficult to predict an earnings beat. This bearish signal is reinforced by the company's recent performance, having surpassed consensus EPS estimates only once in the last four quarters. Furthermore, the consensus EPS estimate has remained stagnant over the past 30 days, and the Most Accurate Estimate is lower than the consensus, indicating that recent analyst revisions have been negative. While the market anticipates strong growth, these proprietary metrics and historical data point to a low probability of a positive surprise, creating a cautious setup heading into the report.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment