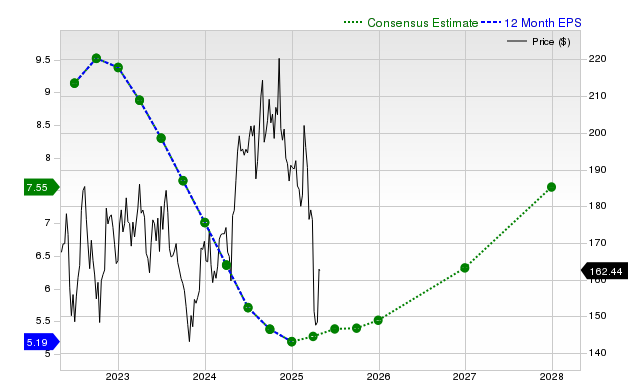

Texas Instruments (TXN) shares have underperformed the broader market and semiconductor industry over the past month, despite consistently exceeding consensus earnings and revenue estimates in recent quarters. Analysts have positively revised future EPS and sales estimates, projecting year-over-year growth, yet the stock carries a Zacks Rank #3 (Hold), indicating expected near-term performance in line with the broader market. Furthermore, TXN's valuation is graded 'D' by Zacks, suggesting it trades at a premium relative to its peers.

Texas Instruments (TXN) presents a conflicting profile for investors, marked by a significant divergence between its fundamental outlook and recent market performance. Over the past month, the stock has declined 11.6%, starkly underperforming both the S&P 500 composite (+3.1%) and its own semiconductor industry peers (+9.3%). This negative price action contrasts with the company's strong operational execution, evidenced by a consistent history of beating consensus estimates for both revenue and earnings over the last four quarters, including a +3.22% revenue surprise and a +6.82% EPS surprise in the last reported period. Looking forward, analyst sentiment is positive, with upward revisions to earnings estimates projecting EPS growth of +7.7% for the current fiscal year and accelerating to +14.8% for the next. However, two key factors temper this bullish fundamental view: the stock's valuation and its official rating. With a Zacks Value Style Score of 'D', TXN is identified as trading at a premium to its peers. This rich valuation, combined with a Zacks Rank of #3 (Hold), suggests that while fundamentals are solid, the stock is expected to perform merely in line with the broader market in the near term, balancing its growth prospects against its current market price.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.05

Ticker Sentiment