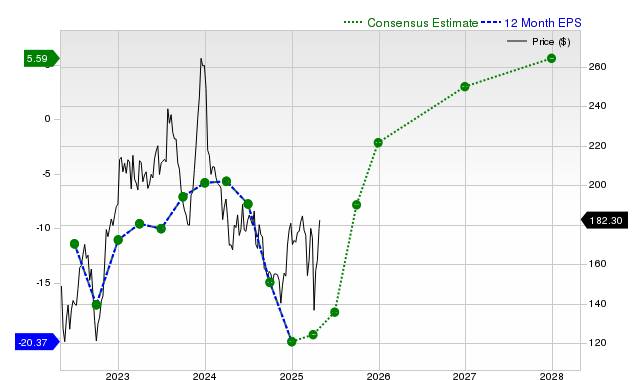

Boeing (BA) has underperformed the broader market and its sector recently, despite reporting strong revenue beats and significant year-over-year revenue growth. While the company is projected to substantially narrow losses this fiscal year and return to profitability next, recent earnings estimate revisions show slight downward adjustments for the near term. Consequently, Zacks maintains a "Hold" (Rank #3) rating for BA, anticipating market-perform returns, and notes the stock currently trades at a premium valuation relative to its peers.

Boeing (BA) exhibits a complex fundamental picture, characterized by significant stock underperformance juxtaposed with strong underlying growth metrics. Over the past month, shares have declined 8.7%, lagging both the S&P 500 composite's 2.7% gain and the Aerospace-Defense industry's 4.6% rise. Despite this price weakness, the company's recent operational results were strong, with last quarter's revenue of $22.75 billion beating estimates by 4.09% and representing a 34.9% year-over-year increase. Looking forward, consensus forecasts project robust revenue growth of 28.8% for the current fiscal year and 13.1% for the next. The earnings outlook is also improving dramatically on a year-over-year basis, with an expected loss of $2.33 per share for the current fiscal year marking an 88.6% improvement, and a projected return to profitability next fiscal year with an EPS of $2.44. However, sell-side analysts have recently tempered near-term expectations, trimming current-year EPS estimates by 3.6% over the last 30 days. This mixed sentiment is captured by a Zacks Rank #3 (Hold) and is compounded by a challenging valuation; the stock receives an 'F' grade for value, indicating it trades at a premium to its peers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

-0.10

Ticker Sentiment