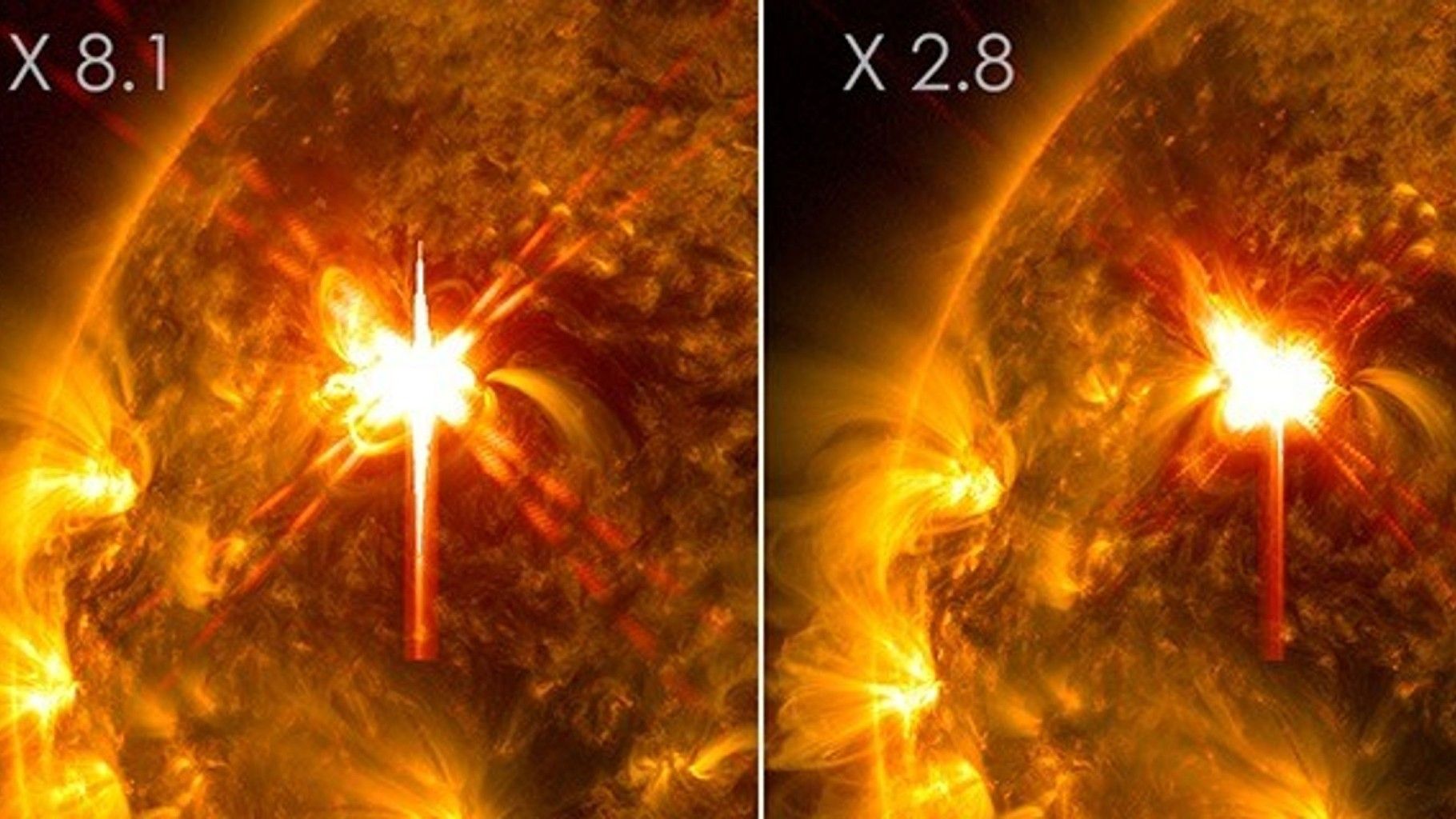

Sunspot region 4366 rapidly grew and produced more than 20 solar flares within 24 hours, including at least 23 M-class flares and four X-class events that peaked with an X8.1 eruption — the strongest single flare since October 2024. The X8.1 flare triggered partial radio blackouts in the South Pacific and launched a coronal mass ejection now forecast to pass near Earth on Feb. 5, with a possible glancing blow that could cause radio/GPS disruptions, satellite damage and enhanced auroras. Solar maximum conditions are expected through 2026, raising the chance of further disruptive space-weather events that could affect communications, navigation and power-grid-sensitive assets.

Market structure: Winners are suppliers of hardened space and grid hardware and government/defense primes (space systems, ground-hardened comms) that can convert a spike in mission-critical orders into backlog — expect pricing power improvement if insurers tighten capacity. Losers include vulnerable satellites/operators, small-cap launch/satellite services with low cash buffers, and specific GPS-dependent operators; airlines/utilities face operational risk but low immediate revenue loss absent a direct grid hit. Risk assessment: Tail risk remains low-probability/high-impact — a Carrington-class event (Kp≥9) could produce multi-week grid/satellites outages and >1% GDP shock; probability this solar cycle ~1–3% annually per historical models but impact is severe. Immediate window: days (Feb 5 glancing blow risk), short-term: weeks–months (insurance claims, capex orders), long-term: 6–36 months (procurement, regulatory spending, insurance repricing). Hidden dependencies include GPS timing for financial networks, semiconductor supply constraints for replacement sats, and reinsurance capacity. Trade implications: Near-term volatility trading window around Feb 5 favors short-dated, high-gamma option plays on satellite and comms names; medium-term trade is long defense/space primes that sell resilience (NOC, LMT, LHX, RTX) with 6–18 month horizons. Commodities/bonds: small safe-haven bid to Treasuries and gold if event escalates; USD/JPY and CHF may strengthen. Use triggers: add/trim positions on SWPC alerts (G3+ or Kp≥6). Contrarian angles: Consensus underprices structural spend on resilience through 2026 — premiums and procurement cycles will rise, benefiting select equipment makers more than diversified insurers. Conversely, near-term market panic in large insurers is likely overdone — diversified balance sheets limit claims exposure; small-cap space equities may price in permanent demand that execution risk will undercut. Historical analogs (2003, 2012 storms) show concentrated gains for suppliers, not broad consumer dislocation.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00