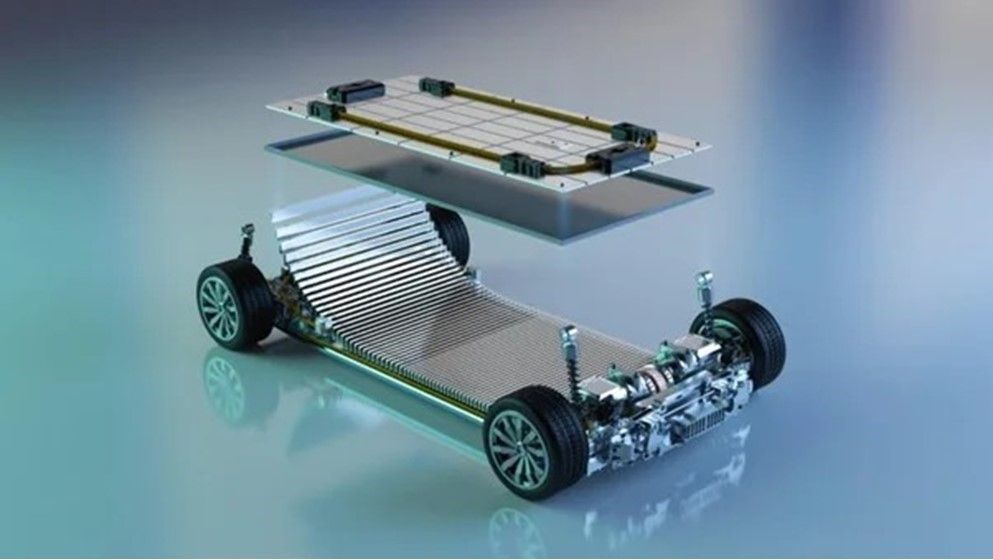

Geely Holding said global sales rose 26% to 4.116 million vehicles in 2025, with electric and hybrid sales reaching 2.29 million units, or 56% of total volume. The group targets more than 6.5 million annual sales and over 1 trillion yuan of revenue by 2030, while expanding in China and overseas markets. It also outlined advances in Level 2-4 autonomous driving and solid-state batteries, including a 100,000-vehicle robotaxi fleet goal by 2030.

The important signal is not the top-line ambition; it is the implied shift in capital allocation from volume growth to ecosystem control. A manufacturer publicly targeting autonomous mobility, solid-state batteries, and robotaxi scale is effectively telling the market it wants to internalize more of the value stack, which tends to pressure commoditized suppliers and legacy OEMs with slower software cycles. In China, that usually means margin share migrates toward brands that can monetize software, fleet services, and battery performance rather than purely sheet-metal execution.

The second-order winner set is broader than the company itself. Battery materials, ADAS sensor stacks, compute, and industrial automation vendors should see pull-forward demand if the roadmap is credible, but the biggest near-term competitive consequence is on domestic EV peers: when a large diversified group signals aggressive pricing, range, and autonomy upgrades simultaneously, it raises the bar for product cadence across the sector and can compress residual values in slower-refresh brands. Overseas, the expansion thesis is most dangerous for incumbents in Southeast Asia and Latin America, where localized assembly plus Chinese tech bundling can take share faster than Western OEMs can adapt.

The contrarian angle is that the market may be over-discounting the strategic optionality while underpricing execution risk. Level 4, robotaxi fleets, and solid-state batteries are all multi-year promises with binary commercialization gates; if any of those slip by 12–24 months, the narrative can re-rate from platform premium back to cyclical auto multiple. In other words, the right way to express this is not as a straight-line EV growth story, but as a dispersion trade on execution quality versus headline ambition.

Catalysts to watch are product launches, autonomous mileage milestones, and any evidence of margin sacrifice to hit share targets in China. The risk case is that global expansion adds working-capital drag and channel complexity just as pricing in EVs remains competitive, which could make the 2030 targets look structurally aspirational rather than financially accretive.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.72