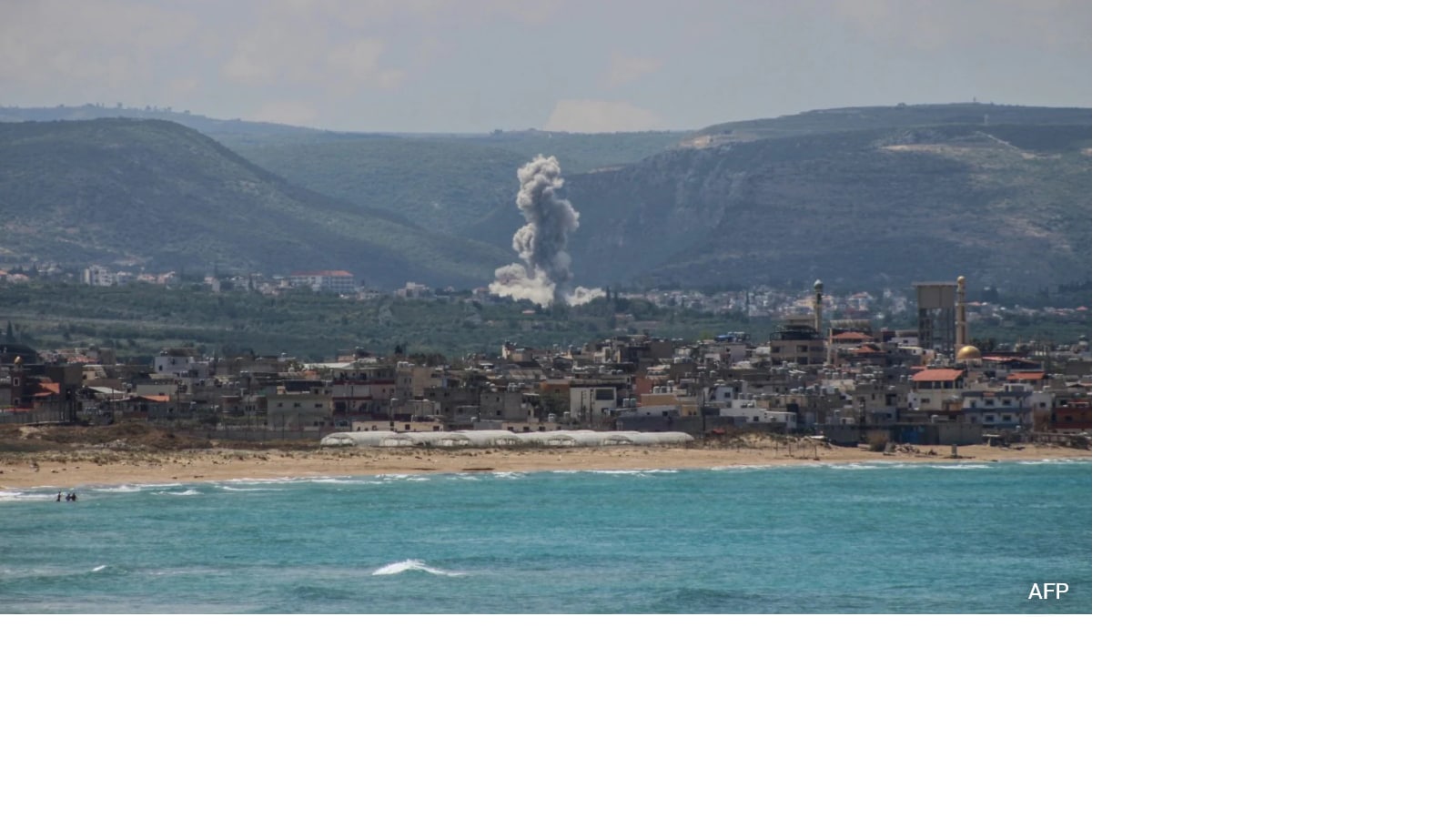

The US launched new strikes on southern Iran targeting missile sites and boats suspected of placing mines, escalating tensions while peace talks were underway in Doha. The attacks raise risks to the Strait of Hormuz, a critical energy transit route, and could disrupt global oil flows and broader market sentiment. Iran has not yet responded, but the fragile ceasefire and negotiations appear increasingly vulnerable.

This is not just another headline risk event; it is a direct escalation against the single choke point that prices a large share of global energy and freight risk. The market’s first-order instinct is to buy crude and defense, but the more durable implication is higher volatility across the entire Gulf complex: shipping insurance, regional equity risk premia, and EM FX all reprice faster than spot oil. If this feeds even a modest increase in perceived closure risk for Hormuz, the marginal winner is not only upstream energy but also optionality on disruption itself — tanker rates, LNG route economics, and inflation breakevens. The second-order issue is timing: these events often produce a sharp 24-72 hour risk-off move, but the lasting move depends on whether talks remain alive. If diplomacy continues, crude may mean-revert while volatility stays bid; if negotiations break, the market transitions from event risk to inventory risk, and physical barrels in the Atlantic Basin become far more valuable. That setup tends to favor refiners with secure feedstock and U.S.-exposed producers over broad energy baskets, because the winners are those with barrels not exposed to Middle East transit and with pricing power on realized differentials. The contrarian view is that the market may be overestimating the probability of a true Hormuz shutdown while underestimating the commitment of both sides to preserve a negotiating channel. That means spot oil could overshoot relative to the actual supply loss, creating a better entry on volatility than on outright crude direction. The bigger medium-term risk is not one strike, but policy contagion: higher shipping costs, tighter financial conditions, and renewed pressure on emerging-market currencies with external funding needs.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.72