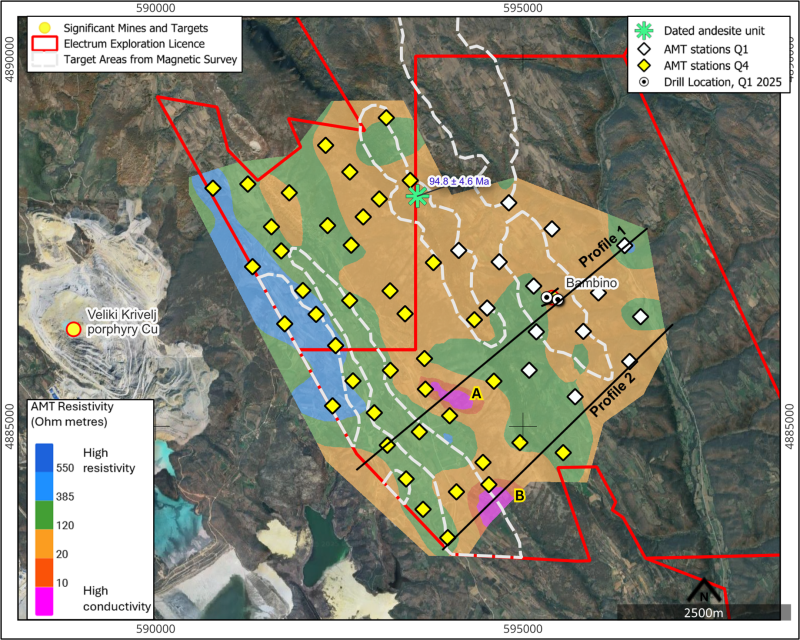

Electrum Discovery (TSXV:ELY) completed a Phase 2 broadband AMT survey (41 stations over a 5 x 2.5 km area) at its Timok East copper‑gold project in Serbia, combining data with an earlier survey to produce an extended 3D resistivity model that highlights two high‑conductivity target zones at ~250–550 m depth. U–Pb apatite dating returned a Late Cretaceous age of 94.8 ± 4.6 Ma for an andesitic unit within the Limestone Boundary anomaly, supporting the interpreted eastward extent of Timok magmatism. Management views these geophysical and geochronological results as providing a technical basis to advance the new targets to a drill‑ready stage in 2026, representing an early‑stage exploration upside for investors but requiring drilling to convert into definitive value.

Market structure: The AMT + dating news chiefly benefits Electrum Discovery (TSX‑V:ELY / OTC:ELDCF), potential local drill contractors and M&A‑active mid‑tiers hunting porphyries; service providers (3D Consulting) and drill rigs also gain optionality. It does not move global copper/gold supply materially but increases investor appetite for Western Tethyan copper juniors — expect a sector re‑rating with typical junior rerates of +20–60% on drill anticipation, pressuring implied vol and bid/ask spreads in small‑cap listings. Risk assessment: Tail risks include a failed scout drill (no economic intercepts), a dilutive financing (>C$5–10M at >20% discount), or Serbia permitting/political delays; each has >10% probability and would trigger >40% downside for current equity. Immediate (days) impact is muted; short term (weeks–6 months) hinges on drill permits and financing; long term (12–24 months) depends on drilling outcomes and ability to define a maiden resource. Hidden dependencies: access to rigs/contractors and USD/CAD financing cost; a global drill shortage or copper price drop >15% would materially change project economics. Trade implications: Direct play — initiate a small speculative position: 2–3% portfolio in ELY.V (or OTC:ELDCF) ahead of planned 2026 scout drilling; set a tactical take‑profit at +50–100% on positive early intercepts and a hard stop at −40% or on announcement of >C$5M dilutive raise. If liquid options exist, buy Dec 2026 LEAP calls or a 1:1 call spread (buy ATM, sell +30% OTM) size 0.5–1% to limit premium; pair trade: long ELY.V vs short GDXJ (Junior Gold Miners ETF) 25% notional to hedge metal‑beta and volatility. Contrarian angles: The market underestimates drill cost and depth risk — targets at 250–550m are expensive (C$500–1,200/m), increasing dilution risk; many AMT conductors fail to convert to economic porphyries, so positive pre‑drill sentiment may be overdone. Historical parallels (junior geophysics rallies then post‑drill crashes) suggest sizing small and preparing to add on a >30% post‑drill sell‑off; a disciplined buy‑the‑dip plan after first negative scout results offers asymmetric reward.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.35