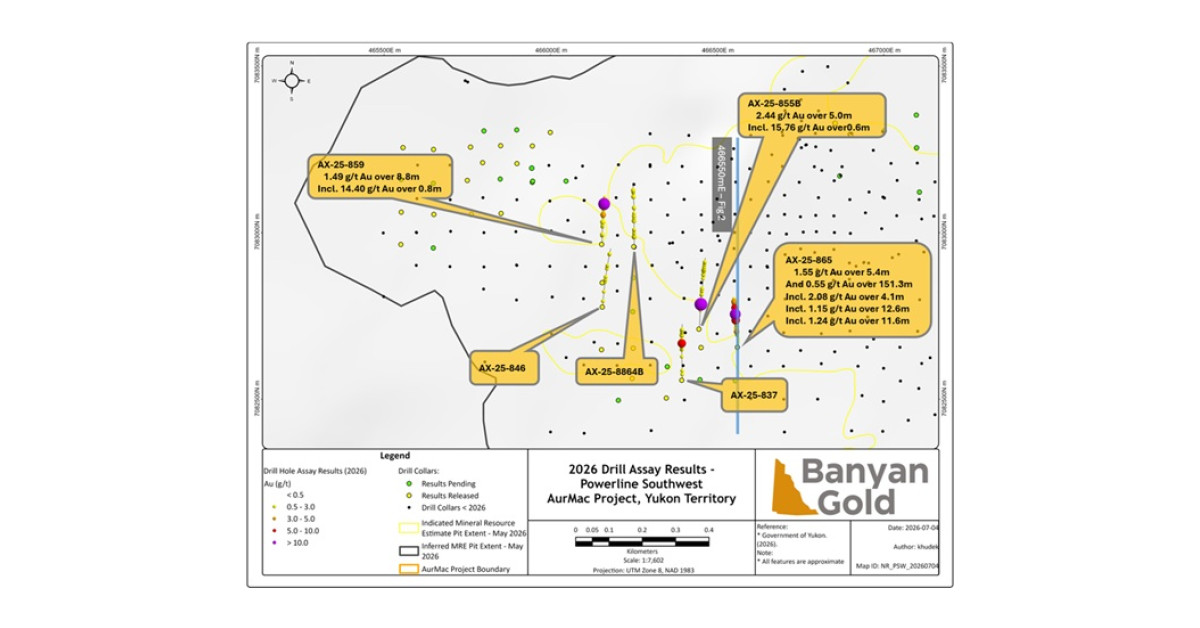

Banyan Gold reported additional high-grade gold drill results at its AurMac Powerline Southwest/West area, including 2.08 g/t Au over 4.1m (within 0.86 g/t Au over 31.4m) and 2.44 g/t Au over 5.0m (with 15.76 g/t Au over 0.6m). Management said the intervals could support upgrading mineralized domains and discovering new continuous, high-grade zones, while the drill program is ahead of schedule with 33,000m completed out of a 70,000m plan. Overall, the update is a modest positive catalyst for the company’s resource expansion narrative rather than a financial/market-wide event.

This is more important as a de-risking event than a discovery event. In a bulk-tonnage project, the market pays for continuity and conversion, not just isolated grade spikes; if these zones tighten the geological model, the implied value per ounce can rise faster than the headline resource count. That matters most for BYN/BYAGF because the current discount is really a discount to confidence in mineability, not a lack of ounces.

The immediate tape can overshoot because junior gold names trade on exploration momentum, but the next 1-3 month catalyst is whether the infill pattern supports a meaningful inferred-to-indicated migration in the next resource update. If the higher-grade shoots prove discontinuous or too narrow, the excitement will fade and the stock will revert to being a financing-sensitive optionality vehicle. The key falsifier is any update that fails to broaden the mineralized envelope or materially improve modeled economics in the pit shell.

Second-order, a credible upgrade path should pull speculative flow toward other Yukon gold developers and GDXJ beta, while marginally starving lower-quality peers of capital. The structural risk is that the valuation framework appears to assume very strong gold economics; if bullion softens or capex/strip assumptions rise, the marginal value of these holes falls quickly despite the good optics. In that sense, this is a gold-price-enabled story, not yet a self-funded development story.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.20

Ticker Sentiment