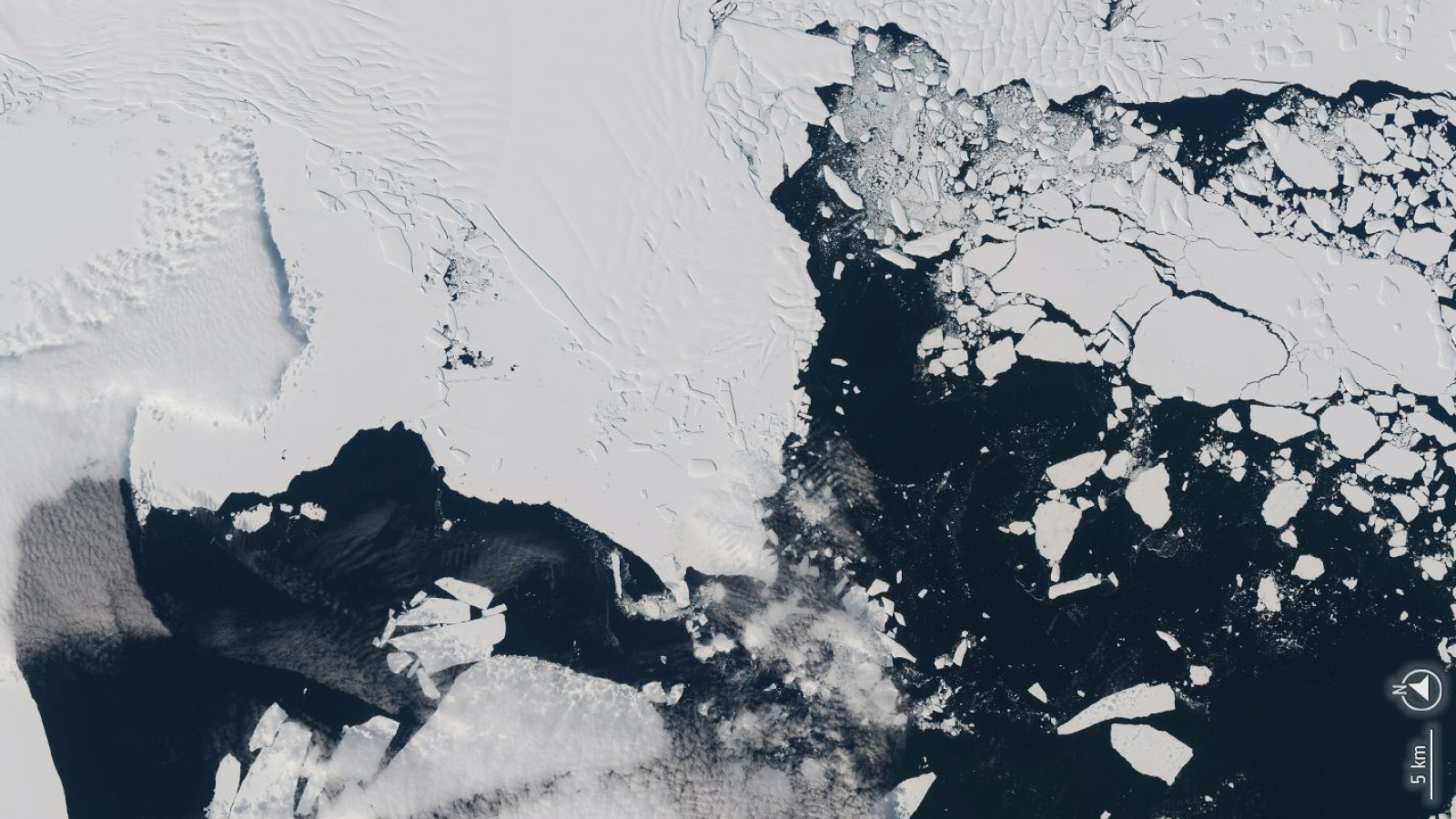

Antarctic seismic data from 2010–2023 reveal more than 360 glacier seismic events, with 245 clustered at the marine terminus of Thwaites Glacier — the “Doomsday Glacier” whose complete collapse would raise sea levels by roughly 3 meters. Most events are consistent with capsizing icebergs, and a prolific 2018–2020 episode of quakes coincided with satellite-confirmed speed-up of Thwaites' ice tongue, suggesting ocean conditions can rapidly affect marine-terminating glacier stability and amplify uncertainty in multi-century sea-level projections.

Market structure: The new detection of hundreds of glacial earthquakes at Thwaites raises the probability that scientific consensus will accelerate recognition of faster regional ice loss, shifting long-term demand toward reinsurance, coastal-defense engineering, and water-infrastructure suppliers. Winners: reinsurers (pricing power on catastrophe coverage), engineering/contractors (AECOM/Jacobs), water-tech (Xylem), and construction materials (steel/cement). Losers: coastal residential/commercial real estate, long-duration coastal municipal bonds and coastal-focused REITs as expected-loss and borrowing costs rise. Risk assessment: Tail risk is low-probability but extreme—an accelerated Thwaites collapse path that materially increases multi-decade sea-level projections could produce sovereign/multi-trillion insured-loss stress; shorter tails include stepped-up regulation and mandatory disclosure of coastal exposure. Near-term (days–months) market moves likely muted; medium-term (6–24 months) sees repricing as datasets, model updates, and insurer reserving change; long-term (3–20+ years) structural capital reallocation to inland infrastructure and adaptation. Trade implications: Expect demand surge for adaptation capex and reinsurance capacity; tactical trades should overweight engineering and water-infrastructure equities and reinsurers, hedge coastal real-estate/muni exposure, and use options to buy convexity (LEAP calls on adaptation names; put spreads on coastal REETs). Watch catalysts: IPCC/satellite papers, insurer 10-K reserve revisions, and national infrastructure bills—each can move valuations 10–40%. Contrarian angles: Consensus still treats Antarctic signals as long-tail and may underallocate to adaptation capex; therefore early exposure to contractors/reinsurers could be underpriced. Conversely, immediate panic shorting coastal assets could be premature because government bailouts/subsidies historically blunt price corrections (e.g., post-Katrina). Position sizing should assume political intervention that limits full private-loss realization.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.30