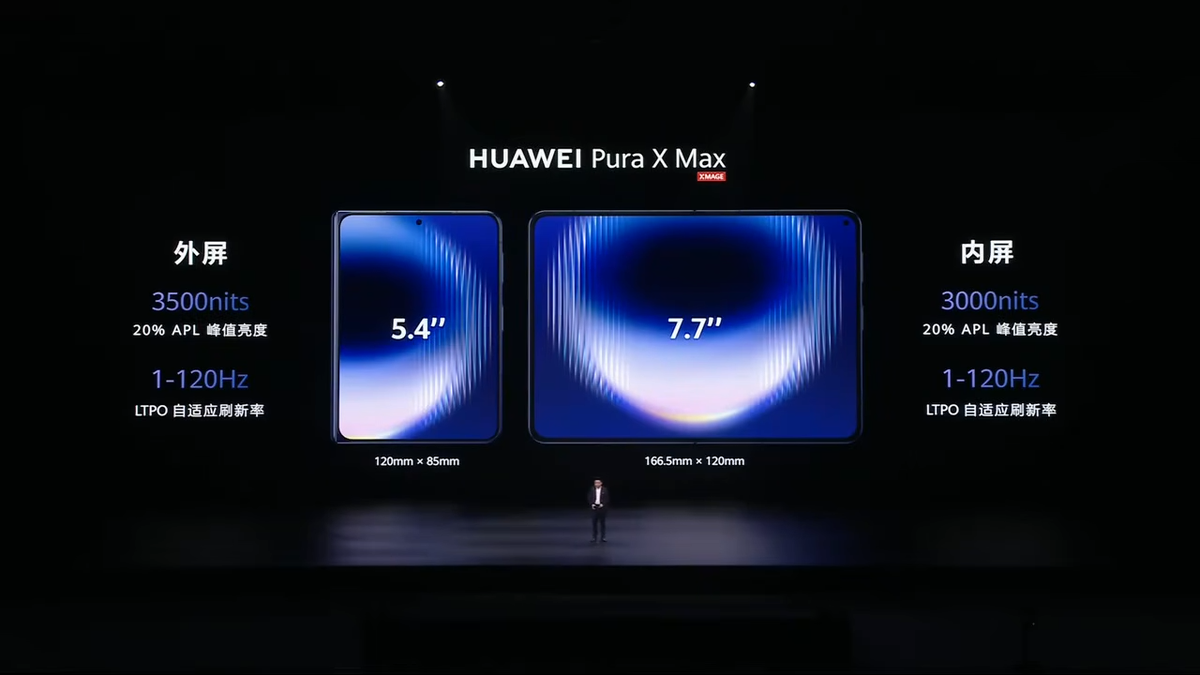

Huawei officially launched the Pura X Max, a new foldable smartphone with a 5.4-inch outer display, 7.7-inch inner display, Kirin 9030 Pro chip, up to 16 GB RAM and 1 TB storage. Pricing starts at 10,999 yuan ($1,613) for the 12 GB/256 GB model and rises to 13,999 yuan ($2,053) for the top configuration. The device is China-focused with no official U.S. or expected European release, and the article frames it as an innovative form factor ahead of anticipated Apple and Samsung foldables.

Huawei is not just launching another foldable; it is compressing the product cycle risk for Apple and Samsung by proving the wider-form-factor thesis in-market before their premium ecosystem releases. The second-order effect is less about unit share in China and more about narrative capture: if consumers normalize the “wide foldable” use case now, the competitive bar for Apple/Samsung moves from feature parity to software ergonomics and app optimization, where late entrants often spend 12-18 months catching up.

For QCOM, the direct revenue impact is limited because Huawei is already off the core Western Android OEM ecosystem, but the strategic read-through is negative for the high-end Android supply chain. A successful Huawei premium device reinforces a bifurcated market: China-premium hardware increasingly designed around domestic silicon, domestic OS, and domestic app rails, which caps the upside from any future China handset refresh cycle that investors might otherwise have attributed to Qualcomm content expansion.

AAPL’s risk is subtler: this increases the probability that its first foldable must launch as a polished category-definer rather than an experimental SKU. That raises execution risk on hinge durability, battery tradeoffs, and app adaptation, and likely shifts the launch mix toward higher ASP configurations to protect gross margin. The market is still underestimating how much a foldable iPhone would cannibalize the Pro Max upgrade pool if the form factor genuinely improves media consumption and multitasking by a visible margin.

The contrarian view is that the headline is more important than the hardware economics. Huawei can set design direction, but without global distribution, its innovation may overstate competitive threat in revenue terms while underestimating how much it pressures rivals’ roadmap timing. Over the next 6-12 months, the stock-level winners are more likely to be the companies selling tools, components, and app infrastructure that benefit from foldable adoption broadly rather than the handset brands fighting for first-mover prestige.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.20

Ticker Sentiment