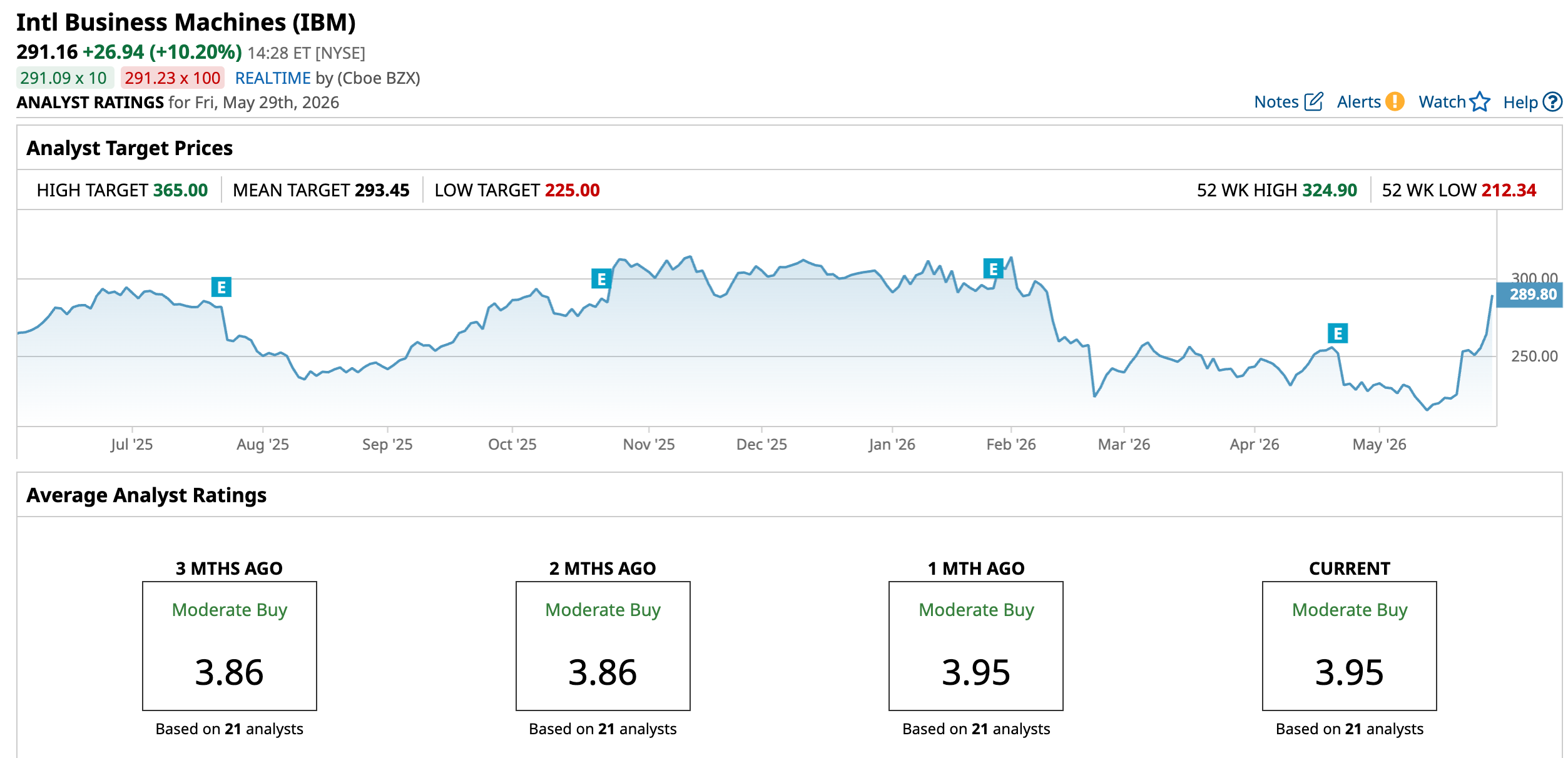

IBM is positioning itself as the best-capitalized quantum computing winner, with $14.7 billion of free cash flow in 2025, $10.6 billion of net income, and a planned $10 billion quantum investment over five years. The company also secured roughly $1 billion in public funding, maintains a 2029 target for a fault-tolerant quantum computer, and trades at 20.59x forward earnings with a 2.6% dividend yield. Analysts rate IBM a Moderate Buy with a $293.45 mean target, implying 0.79% upside, while the high target of $365 suggests 25.36% upside.

IBM is emerging as the “toll collector” on a theme that remains far too immature for the market to underwrite as a standalone commercial winner. The second-order effect is that quantum spend is likely to concentrate around a handful of balance-sheet-rich incumbents, which compresses the survivability of pure plays that need frequent capital markets access just to keep the R&D engine running. That dynamic should keep valuation dispersion wide: capital-light storytelling can still support bursts of momentum in IONQ/RGTI/QBTS, but the medium-term winner is more likely to be the company that can finance multiple product cycles without dilution.

The real catalyst is not near-term quantum revenue; it is procurement and ecosystem lock-in. IBM’s strategy of pairing quantum with classical infrastructure and AI accelerators increases the probability that enterprise pilots convert into broader platform spend, even if fault-tolerant systems slip beyond the stated timeline. Government dollars matter here because they shorten the gap between lab progress and commercial relevance, and they also make IBM’s roadmap less optional than the pure plays’—a subtle but important de-risking of the capex burden.

The key risk is that investor enthusiasm re-rates the sector too early, then fades when monetization stays negligible for 12-24 months. In that scenario, the pure plays are vulnerable to multiple compression and dilution, while IBM could still outperform on relative basis because quantum acts as a long-duration call option financed by current cash flows and dividends. The contrarian view is that the market may be underpricing how long incumbents can keep funding the “waiting game,” which argues for owning the infrastructure parent rather than chasing the narrative leaders.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.32

Ticker Sentiment