The EU has restarted ratification of its US trade deal, moving a long-delayed agreement toward final approval that includes a 15% tariff ceiling on most EU exports. Lawmakers advanced the process despite the US launching fresh investigations that could lead to additional tariffs, creating execution risk. The restart reduces near-term regulatory uncertainty for EU exporters if ratified, but markets should monitor the US probes and final parliamentary votes for potential tariff upside or implementation delays.

The shift toward a more predictable transatlantic trade framework will disproportionately accelerate capital allocation and inventory decisions in sectors with long procurement cycles — think auto OEM supply contracts, aerospace OEM tier-1s and luxury seasonal buys. Expect procurement windows to tighten over the next 3–12 months as firms re-rate landed-cost assumptions; conservatively, this could raise EU-origin unit flows into the US by low-single digits percentage points in the first year in corridors where tariffs were previously a gating variable. Currency and working-capital dynamics will matter: importers will hedge larger EUR exposure and push payable/receivable terms tighter, which benefits banks and FX forwards desks while pressuring short-term liquidity for mid-cap manufacturers.

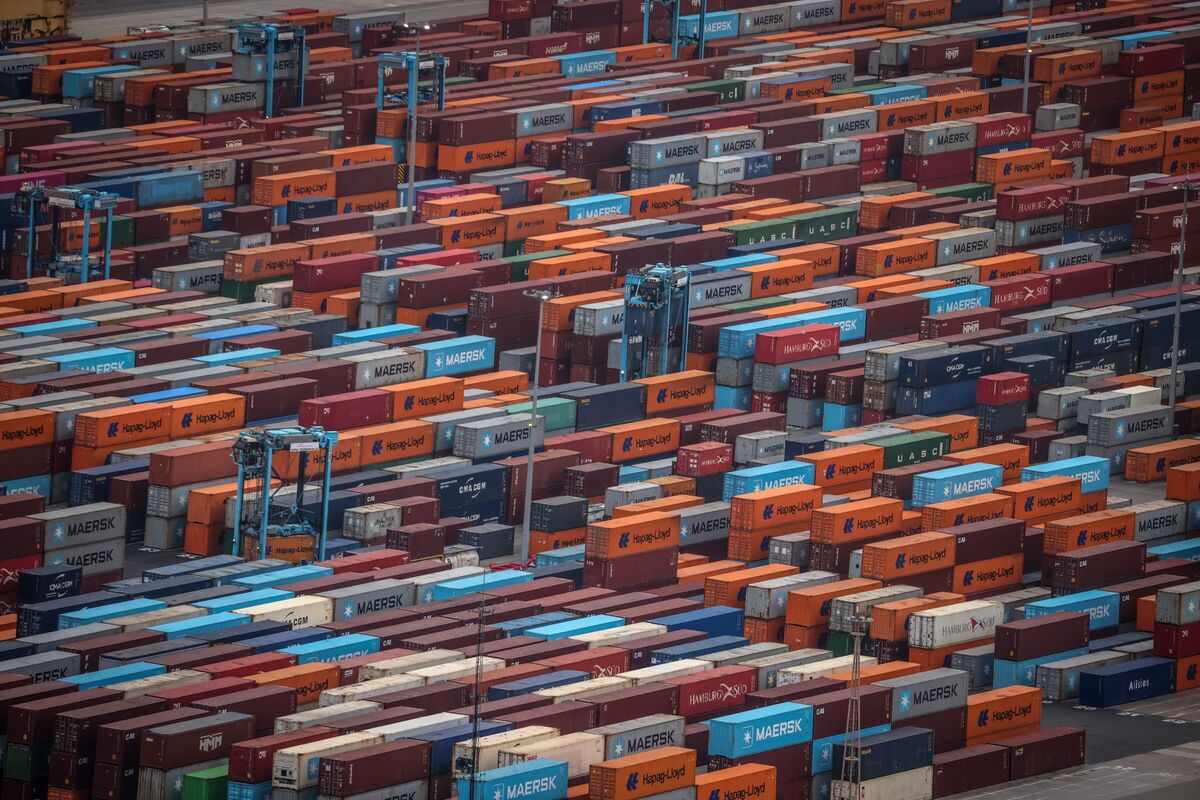

Second-order winners are trade-service providers that convert policy clarity into volume — ports, integrated carriers, forwarders and trade-finance lenders — because they capture margin as freight re-optimizes and modal choices shift. Conversely, US incumbents whose margins rely on protected pricing or local content premiums face modest but tangible share loss and margin compression (think 100–250bps pressure within 6–12 months) in contested categories. Also watch component sourcing: OEMs that had begun nearshoring will pause or reverse parts of those initiatives, lengthening lead times but lowering unit cost volatility over a multi-year horizon.

Key risks and catalysts are political and legal, not economic: near-term headline risk (30–90 days) from adjudications or fresh tariff probes can re-create volatility spikes, while substantive reversals require legislative action or punitive WTO-style rulings over 6–18 months. Market pricing can swing quickly on a single adverse ruling; prepare for 5–12% repricing windows in affected equities and 1–3% moves in EURUSD during such episodes. Monitoring bipartisan Congressional messaging and trade-case filing schedules is the highest-value indicator for a policy reversal.

The consensus view understates implementation friction — trade agreements change legal risk but not overnight supply-chain topology. That favors plays that monetize the transition (freight, FX, trade finance) over binary bets on manufacturers until on-the-ground sourcing decisions are confirmed (12–36 months). A hedged, flow-centric approach captures early alpha while limiting exposure to political tail events that can reverse the narrative quickly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.15