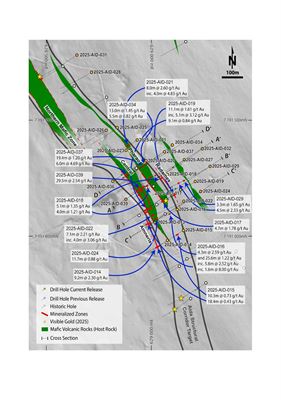

Goldsky Resources reported results from a 10,296.9 m, 39-hole 2025 diamond drill program at its Paubäcken Aida target, with mineralization intersected in 33 of 39 holes and visible gold in 7 holes. Key intercepts include 26.4 m @ 2.80 g/t Au (2025-AID-039), 21.4 m @ 1.17 g/t Au (AID-037), 8.1 m @ 2.30 g/t Au (AID-014) and a high-grade 1.45 m @ 11.42 g/t Au (AID-027); the program identified two new zones (Radames, Amneris) and expanded strike to ~2.1 km with targets remaining open, supporting follow-up programs planned for 2026. These results materially de-risk and expand the project's exploration upside for equity holders but represent exploration-stage news rather than a resource or production update.

Market structure: Goldsky (GSKR.V) is the direct beneficiary — 10.3 km of drilling and multiple multi-meter intercepts (notably 26.4m @2.8 g/t and 11.7m @0.88 g/t) materially de‑risks a district-scale orogenic system in a corridor adjacent to operating mills (Svartliden/Fäbodtjärn) and Agnico’s Barsele JV. Near-term market share gains accrue to Scandinavian explorers and toll‑mill operators; supply impact on bullion is negligible but discovery increases M&A optionality and junior equity flows. Cross-assets: expect modest support to gold (XAUUSD) and junior‑miner implied vols; small‑cap mining equities and HY spreads may tighten on positive risk appetite. Risk assessment: Key tail risks are continuity/metallurgy (visible gold vs disseminated), permitting/environmental pushback in Sweden, and acute dilution from financings; a negative metallurgy or a capital‑markets failure could drop GSKR >40% (tail). Timeframes: immediate (days) = news pop/liquidity; short (3–9 months) = resource modelling and 2026 follow‑up drill plan; long (1–3 years) = PEA/JV or takeover. Hidden dependency: proximity to Svartliden mill raises tolling optionality but also creates M&A crowding; catalysts include maiden resource (>1 Moz at >1.5 g/t to trigger major interest), metallurgical recoveries, and Agnico JV moves. Trade implications: Direct: establish a tactical long in GSKR (small cap micro‑position) sized for idiosyncratic risk; hedge gold‑beta with GDX/GDXJ exposure. Pair: long GSKR vs short GDXJ 1:1 notional to isolate exploration upside; rebalance monthly and cut if underperformance exceeds 30% in 60 days. Options: express leveraged bullishness via 6–12 month GDX call spreads (buy 40% OTM / sell 70% OTM) to cap premium. Entry: accumulate on pullbacks up to 15% from announcement; wait for maiden resource (H2 2026) for scale decisions. Contrarian angles: Consensus focuses on strike length and visible gold but underestimates dilution and metallurgy risk — many intercepts are narrow or lower grade when averaged; the market can reprice juniors sharply once a financing or poor metallurgy appears. Historical parallels: Scandinavian discoveries often trigger takeover interest only after a >1 Moz resource and stable recoveries, not upon early drilling; unintended consequences include aggressive equity raises that halve pre‑raise valuation. Therefore size positions assuming a 40% downside financing shock and plan to add only after PEA or robust metallurgical data.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment