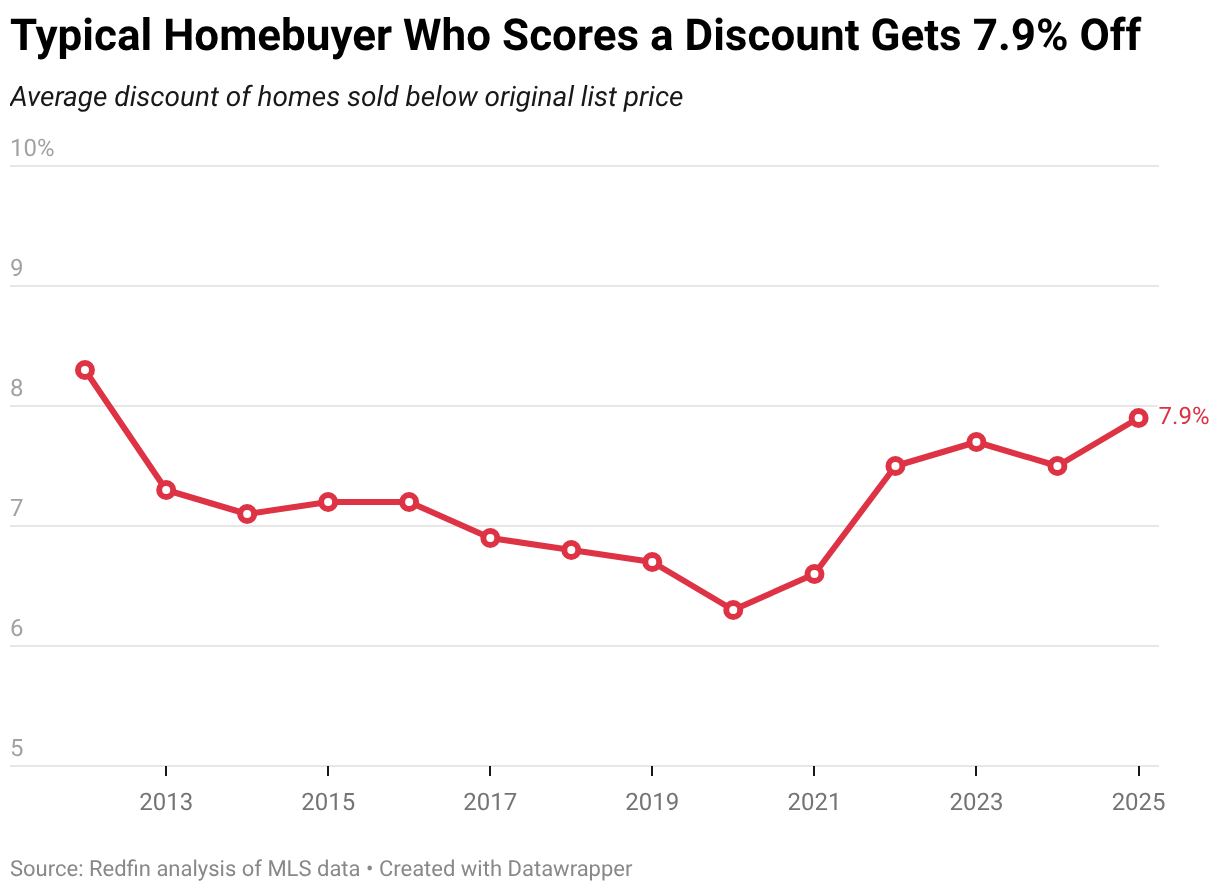

Redfin’s MLS analysis shows the typical 2025 buyer who purchased below list price received a 7.9% discount—the largest since 2012—equating to roughly $31,592 against a median original list price of $399,900; across all buyers the average discount was 3.8% ($15,196) and 62.2% paid below list. The shift to a strong buyer’s market (about 47% more sellers than buyers), high mortgage rates and regional factors (insurance and disaster exposure in Florida) produced larger discounts—26.1% of below-list buyers secured discounts of 10%+—while only four metros (led by San Francisco at a 3.8% premium) saw typical sales above asking.

Market structure: The data show a pronounced buyer’s market—62% of transactions closed below ask and the typical below-ask discount rose to 7.9% (=$31.6k vs median list $399.9k). Winners: renters, multifamily REITs, mortgage-bond holders and buyers in high-inventory metros (FL, MI, PA). Losers: leverage-dependent homebuilders, mortgage-originators tied to purchase volume, Florida condo owners/HOAs and insurers facing higher claims/fees. Risk assessment: Key tail risks include a sharp 2026 regional catastrophe (FL hurricanes) that forces insurance losses/assessment spikes, or a rapid Fed pivot lowering rates >100bp that materially re-prices demand up (housing rally). In the next 0–3 months expect continued price discovery and more delistings; 3–12 months is decisive for inventory normalization; 12+ months will reflect rate path and migration patterns. Hidden dependencies: condominium economics hinge on HOA assessments and local insurance markets, not national GDP. Trade implications: Favor long duration and mortgage-backed exposure if housing weakness feeds disinflation (buy 7–10y Treasuries/IEF on pullbacks if 10y <4.0%). Tactical longs: coastal/core multifamily REITs that benefit from rental substitution (AVB, EQR). Shorts / hedges: national homebuilders (LEN, PHM) and mortgage originators (RKT) into weaker purchase volumes; prefer put spreads 3–6 month expiries to control premium. Contrarian angles: Consensus focuses on ‘housing crash’ headlines; miss is segmentation—Bay Area/AI hubs and well-priced listings still command premiums (San Francisco +3.8%). Reaction may be overdone in multifamily and corporate-balance-sheet REITs where rental demand should tighten if buyers sit out; conversely, builder stocks may already price in weakness, so prefer pairs (short builders, long apartment REITs) rather than naked shorts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25