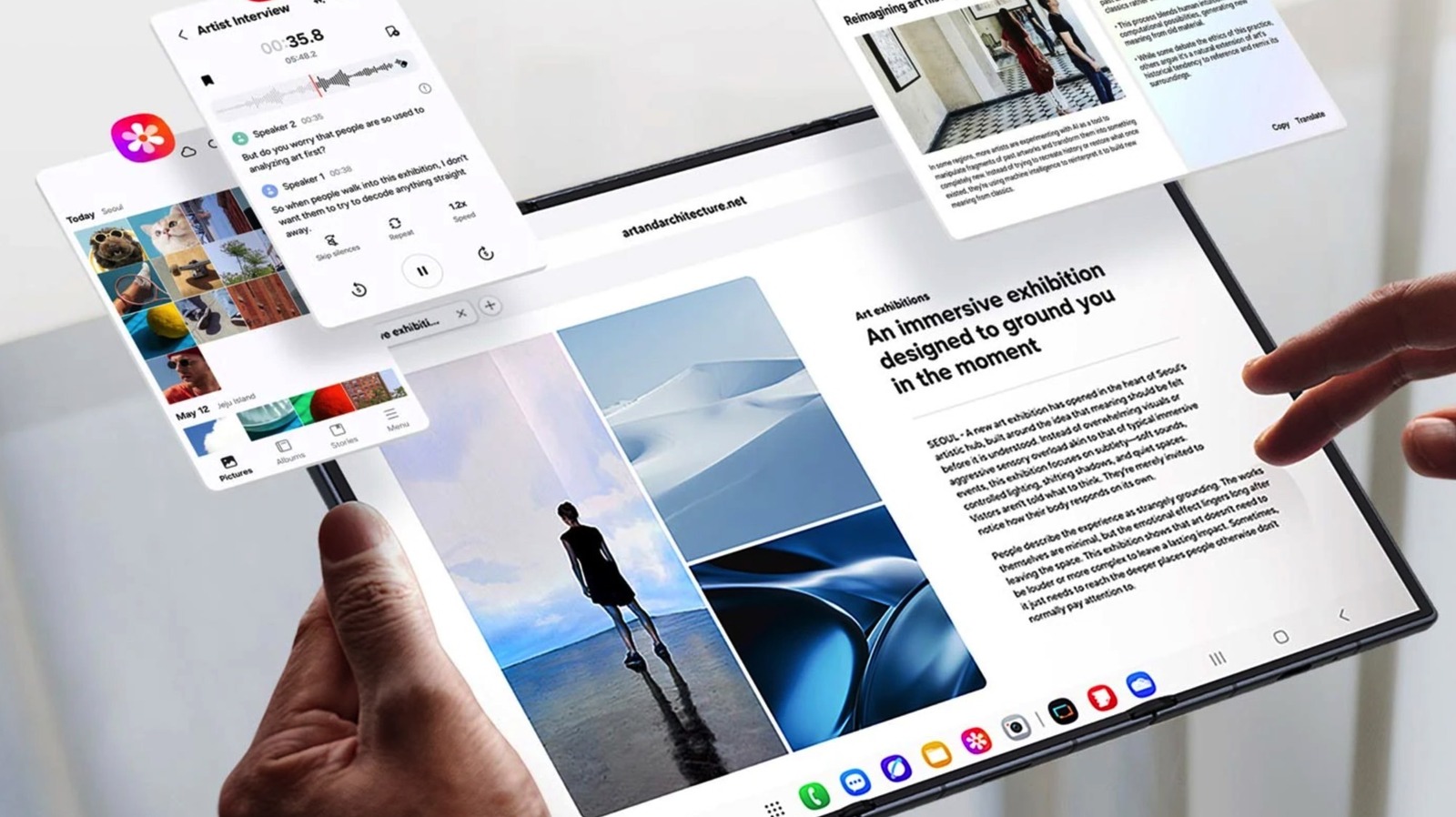

Samsung priced the Galaxy Z TriFold at $2,899 for the 512GB U.S. model, making it the company's most expensive foldable; the device features a 10-inch 2,160 x 1,584 internal display, 6.5-inch cover screen, Snapdragon 8 Elite, 16GB RAM, 200MP main camera, 5,600 mAh battery and 45W charging, with the 1TB price not disclosed. Demos begin Jan. 27 and sales start Jan. 30, 2026; Samsung highlights a 200,000-cycle multi-folding durability test and includes a six-month Google AI Pro trial, but the earlier announced one-time 50% display repair benefit was not mentioned for U.S. buyers.

Market structure: Samsung Electronics (005930.KS / SSNLF) and Samsung Display/Qualcomm (QCOM) are primary beneficiaries — premium $2,899 pricing signals Samsung is testing a >$2.5k ASP tier that could lift mix and gross margins if volume >100k units globally in the first quarter. Losers are mid-tier Android OEMs and aftermarket refurbishers who may face demand compression; Apple (AAPL) is only a second-order competitor because foldables remain niche vs. iPhone volumes. Cross-asset: stronger handset ASPs support Korean tech equity outperformance and could modestly strengthen KRW (+1–3%) on sustained demand; limited immediate commodity impact beyond sustained demand for flexible OLED capacity (benefiting display suppliers). Risk assessment: Tail risks include a high-profile durability failure or elevated return rates (>1–2%) that trigger recalls and compress EPS by >1% in a quarter, and negative headlines that force promotional pricing within 0–3 months. Watch immediate catalysts (retail trials Jan 27, sales Jan 30) for first-week sell-through and carrier subsidy terms; medium-term (3–6 months) risk is cannibalization of Fold 7 and discounting that erodes ASP by $200–400. Hidden dependency: the device’s value is partly tied to the 6-month Google AI Pro trial — if Google changes terms or monetization, perceived utility drops materially. Trade implications: Tactical ideas — low-conviction long exposure to Samsung and suppliers, and defensive hedges for durability risk. Direct: a 1–2% long in 005930.KS with 3–6 month horizon; pair: long QCOM (1% notional) vs. small short on a high-end accessory/repair ETF or names if retailer subsidy spreads widen. Options: buy a 3–6 month call spread on QCOM (5–10% OTM) sized 0.5–1% to capture upside from continued flagship demand; buy short-dated puts on Samsung sized 0.5% as tail protection if early reviews/return reports surface. Contrarian angles: The market underestimates enterprise upside from TriFold’s DeX/tablet-like workflow — if corporate pilot programs ramp in 2–4 quarters, accessory, MDM and cloud-storage revenues could be >$100m incremental annually for Samsung partners. Conversely, consensus may be underpricing the speed at which cheaper Chinese foldables compress margins in H2; a 20–30% price slide in the category in 6–12 months would flip the trade. Monitor first-month return rate, carrier subsidy depth, and Google AI monetization as discrete triggers that will decide whether this is margin expansion or a niche PR exercise.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25