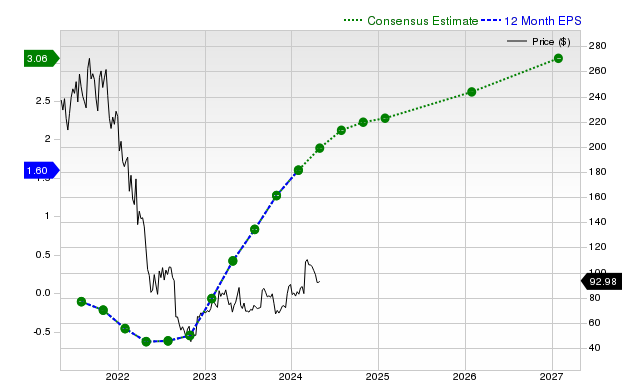

Okta (OKTA) has recently underperformed the broader market and its industry, returning -4.9% over the past month. Despite this, the cloud identity management firm has consistently beaten consensus revenue and EPS estimates in the last four quarters, with its latest reported revenue of $688 million reflecting 11.5% year-over-year growth and EPS of $0.86 surpassing expectations by 11.69%. Positive earnings estimate revisions have led Zacks to assign a #2 (Buy) Rank, suggesting potential near-term outperformance, though its 'D' Value Style Score indicates it currently trades at a premium relative to peers.

Okta, Inc. (OKTA) presents a conflicting profile for investors, marked by strong fundamental execution set against a premium valuation and recent stock underperformance. Over the past month, the company's shares declined 4.9%, lagging both the S&P 500 composite's 5.1% gain and its own security industry's 3% rise. This price action contrasts with its operational track record, where Okta has surpassed consensus revenue and EPS estimates for four consecutive quarters. In its last report, revenue grew 11.5% year-over-year to $688 million, beating estimates by 1.22%, while EPS of $0.86 represented an 11.69% surprise. Looking forward, sell-side analysts project continued growth, with consensus estimates indicating a 16.7% year-over-year EPS increase for the current fiscal year and 8.6% for the next. These positive earnings estimate revisions have driven a Zacks Rank of #2 (Buy), suggesting potential for near-term outperformance. However, this bullish outlook is tempered by valuation concerns, as evidenced by a Zacks Value Style Score of 'D', which indicates the stock is trading at a premium compared to its peers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment