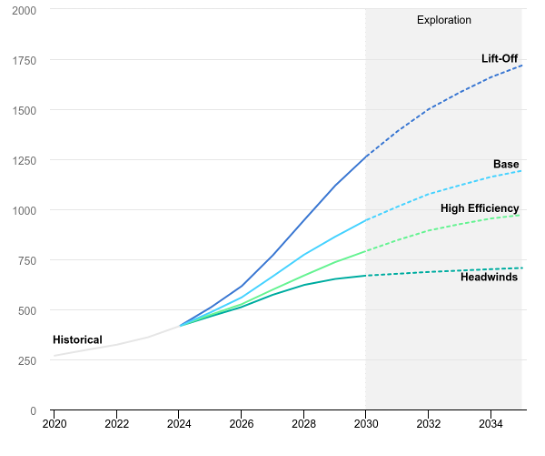

The article argues that AI/data-centre power demand and geopolitical energy shocks are accelerating a nuclear power revival, with global data-centre electricity use projected to rise from about 415 TWh in 2024 to 945 TWh by 2030. It cites 63 reactors under construction worldwide, more than 60 lifetime extensions in the past five years, and US plans for $80 billion of spending on 10 AP1000 reactors plus upgrades at existing plants. The near-term beneficiaries are likely utilities, reactor builders, uranium/supply-chain names, and data-centre operators seeking 24/7 low-carbon power.

The market is starting to price nuclear less as a policy story and more as an infrastructure bottleneck trade. The first-order beneficiaries are not just reactor developers, but firms that can monetize the bottlenecks around grid interconnection, heavy electrical equipment, thermal management, and long-duration fuel logistics; those businesses often get paid earlier in the cycle than reactor owners do. The second-order winner is the hyperscaler cohort, because any credible baseload contract reduces the option value of self-build generation delays and lowers the probability that AI capex gets throttled by power scarcity.

The real inflection is financing behavior: when balance sheets with trillion-dollar market caps start underwriting power directly, the traditional utility-regulated cost-of-capital penalty for nuclear construction becomes less binding. That should compress the gap between “announced capacity” and “actual starts,” but only for standardized designs and repeatable sites. The counterintuitive loser is any adjacent clean-power asset that depends on scarcity pricing and intermittent-balancing premiums; a successful nuclear restart path can cap merchant power upside and reduce the need for some backup generation assets.

The contrarian miss is timing. The narrative is structurally bullish, but the tradable earnings impact for most exposed equities is likely a 12-36 month story, while the nearest-term market reaction may overstate how much of the build-out is executable before 2030. Nuclear remains a permitting, supply-chain, and labor-constrained industrial program; the market may be too quick to extrapolate headline announcements into cash flows. Any reversal likely comes from project slippage, policy churn, or a sharp decline in power prices that weakens the urgency premium.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.45

Ticker Sentiment