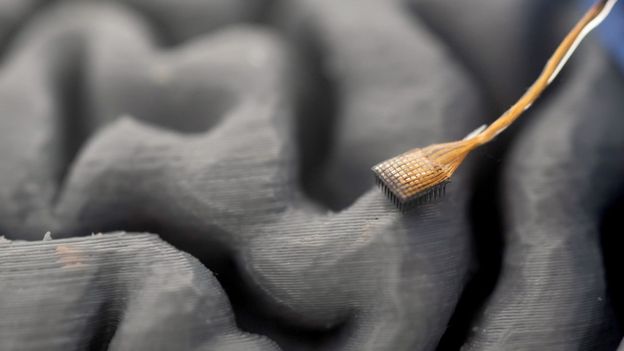

Academic teams at Stanford and UC Davis reported advances in brain–computer interfaces that use machine learning to decode inner speech and the non-verbal features of speech: Stanford achieved up to 74% real-time accuracy on an inner-speech counting task, while earlier work yielded ~32 words per minute at 97.5% accuracy and prototype prosody decoding produced ~60% intelligibility. Parallel fMRI+generative-AI work (including Stable Diffusion approaches) is enabling crude image and audio reconstruction from brain scans; current systems sample very limited neural populations (e.g., ~256 electrodes) and face clear technical and ethical limits, but researchers and commercial players (eg, Neuralink) are positioning for near-term commercialization.

Market structure: Cloud and AI infrastructure owners (GOOGL, AMZN, NVDA) are the primary near-term beneficiaries as BCI research drives demand for model hosting, high-throughput GPUs and multimodal inference. Medical device suppliers (surgical implants, microelectrode manufacturers) and specialized imaging vendors will see higher ASPs but face concentrated supply chains; margins will bifurcate between platform owners and hardware specialists.

Risk assessment: Key tail risks are regulatory/privacy shocks (moratoria or stringent data residency rules) and clinical setbacks; either could erase 20–50% of market value in vulnerable small-caps within 6–24 months. Hidden dependencies include cloud data policies, chip shortages, and liability insurance for implants; catalysts are FDA clearances, large-tech commercialization announcements, or high-profile breaches occurring in the next 3–12 months.

Trade implications: Favor platform/cloud exposure (GOOGL > AMZN on sentiment/AI model IP) and avoid/short pre-revenue neuro-hardware names without FDA pathways. Use defined-risk option structures to lever upside on GOOGL over 6–12 months and hedge medtech longs with long-dated puts; expect asymmetric returns as monetization of BCIs likely front-loads to cloud and model owners over 12–36 months.

Contrarian angles: The market underestimates commercialization lag—consumer/enterprise BCI monetization is a 5–10 year runway, not immediate. Early winners will be software/IP-rich firms; hardware-only names will face capital intensity and regulatory drag. Expect regulation to force on-prem or edge solutions, increasing capex for cloud providers and lowering gross margins for commoditized data-hosting services.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment