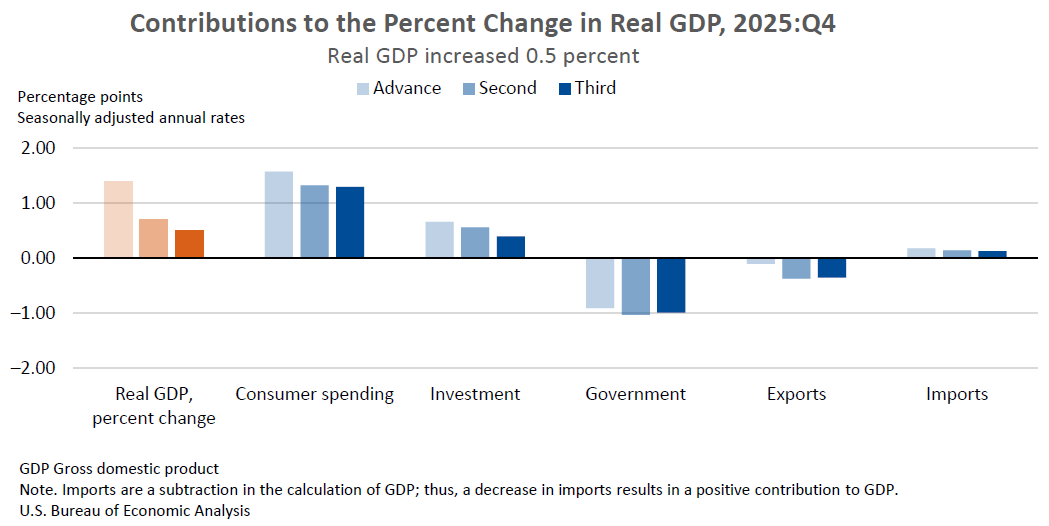

Real GDP grew 0.5% annualized in 2025Q4 (revised down 0.2ppt from the second estimate) following a 4.4% increase in Q3; BEA says the October–November federal shutdown subtracted about 1.0 percentage point from Q4 growth. Growth was driven by consumer spending and investment and partly offset by declines in government spending and exports; real final sales to private domestic purchasers rose 1.8% in Q4. Corporate profits increased $246.9 billion in Q4, the PCE price index rose 2.9% (core PCE 2.7%), and full-year 2025 real GDP rose 2.1% with PCE inflation at 2.6% for the year.

Wholesale inventory adjustment in the latest release is the clearest leading indicator here: it implies negative order flow for industrial manufacturers and their distribution chains over the next 1–3 quarters, not a permanent demand collapse. That destocking will amplify margin pressure at low-turn distributors and freight providers (who have little pricing power in a volume shock), while benefitting balance-sheet-light software and services businesses that won’t carry excess inventory. The fiscal/timing quirks from the federal interruption create a high-probability sequencing distortion — a mechanically weak quarter followed by a transitory rebound when federal services and back-pay normalize. That pattern increases the odds of whipsaw for market-implied policy expectations over the next 60–120 days: a short-lived growth scare that can push yields and risk premia lower, then a noise-driven retracement as prints normalize. Corporate profit resilience on the surface masks uneven drivers: a meaningful share appears non-operational or one-off, so equity-level earnings leverage to underlying final sales is asymmetric. Sectors tied to recurring demand (information services, healthcare delivery) will likely show durable earnings, whereas industrials and distribution-heavy names face downside earnings revision risk as inventories re-align. Net-net, the setup favors quality service providers and rate-duration exposure into the near-term growth scare, paired with targeted short exposure to inventory-levered industrial/distribution equities. Hedge inflation/data-volatility via short-dated volatility or curve steepener protection given the elevated probability of noisy CPI/PCE prints in the coming releases.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

0.00