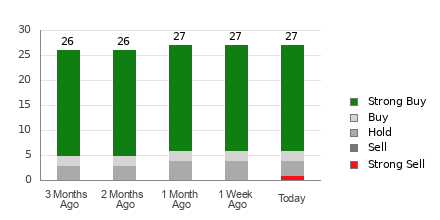

AutoZone (AZO) presents a conflicting outlook, with an Average Brokerage Recommendation (ABR) of 1.43 (approximating Strong Buy/Buy) from 27 firms, yet simultaneously receiving a Zacks Rank #5 (Strong Sell). This divergence is driven by a recent 8.6% decline in AZO's Zacks Consensus Estimate for current year EPS to $152.84, reflecting growing analyst pessimism. The article advises caution against potentially biased ABRs, emphasizing that declining earnings estimates, as captured by the Zacks Rank, are a more reliable indicator of potential near-term price weakness for AZO.

A significant disconnect exists between qualitative sell-side sentiment and quantitative earnings momentum for AutoZone (AZO). While the stock carries a bullish Average Brokerage Recommendation (ABR) of 1.43, derived from 27 firms where 21 issue a "Strong Buy" and two a "Buy", this is directly contradicted by underlying estimate revisions. Specifically, the Zacks Consensus Estimate for the current year's earnings per share has declined 8.6% over the past month to $152.84. This strong agreement among analysts in lowering EPS estimates signals growing pessimism about the company's near-term earnings power, resulting in a bearish Zacks Rank #5 (Strong Sell). The central thesis is that the trend in earnings estimate revisions serves as a more timely and predictive indicator of near-term stock price movement than the potentially biased and lagging ABR.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.50

Ticker Sentiment