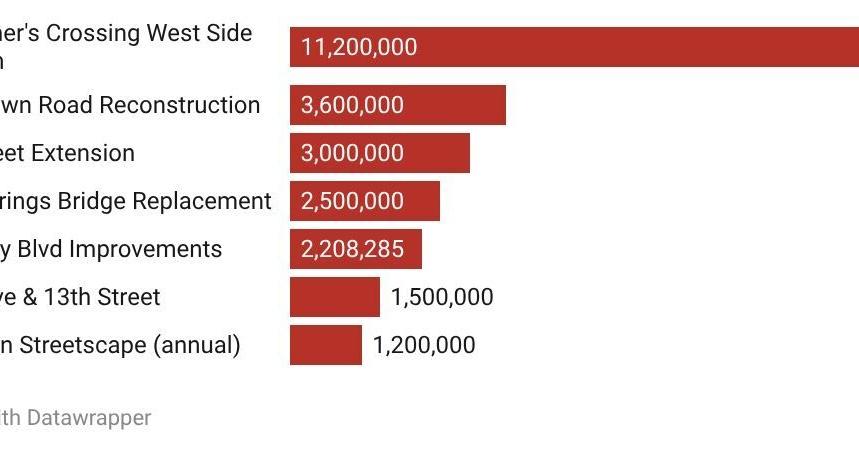

Frederick officials proposed a $57.4 million capital improvements program for fiscal year 2027, with the largest spending categories in stormwater projects at about $19.5 million, roads at roughly $19.0 million, and water projects at about $10.0 million. The plan also includes about $6.4 million for parking, sewer, parks and facilities, plus $3.0 million for the Bond Street extension and $1.3 million for improvements near West Patrick Street at Maryvale Ditch. The budget remains in review, with additional discussion in May and a final vote expected by May 26.

This reads less like a single-city budget item and more like a micro signal for a multi-year municipal capex cycle that is being forced by asset age, resilience needs, and debt capacity. The second-order implication is that the spending mix favors contractors with stormwater, paving, and utility execution capability over pure greenfield builders; the highest-conviction beneficiaries are firms with local backlog visibility, not headline infrastructure ETFs. Because the program is spread across several years, the earnings effect should show up gradually through backlog conversion rather than an immediate revenue pop.

The key underappreciated angle is that flood remediation and stormwater work can crowd out discretionary capital elsewhere, creating hidden opportunity cost for other public works and potentially delaying less urgent projects. That usually compresses bid competition in the near term, especially for specialized civil trades, which can support margins for incumbents with municipal relationships and bonding capacity. If borrowing costs stay elevated or tax receipts soften, the city may phase, resize, or defer later-year packages, making the early tranche the most important for suppliers.

The contrarian view is that markets may overestimate the durability of this demand if it gets lumped into a generic “infrastructure” basket. Municipal capex is lumpy, politically constrained, and vulnerable to election-cycle revisions; a budget proposal is not a funded order book. The real catalyst will be formal appropriation plus contractor awards over the next 1-2 quarters; absent that, this is more of a watchlist setup than an immediate catalyst.

From a risk perspective, the main downside is execution slippage: permitting, utility conflicts, and weather-related delays can push revenue recognition out by 6-12 months while still keeping labor and equipment costs tied up. That favors companies with strong balance sheets and diversified end markets, while levered local contractors could see working-capital strain if the project mix stalls or bid prices come in above plan.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.05