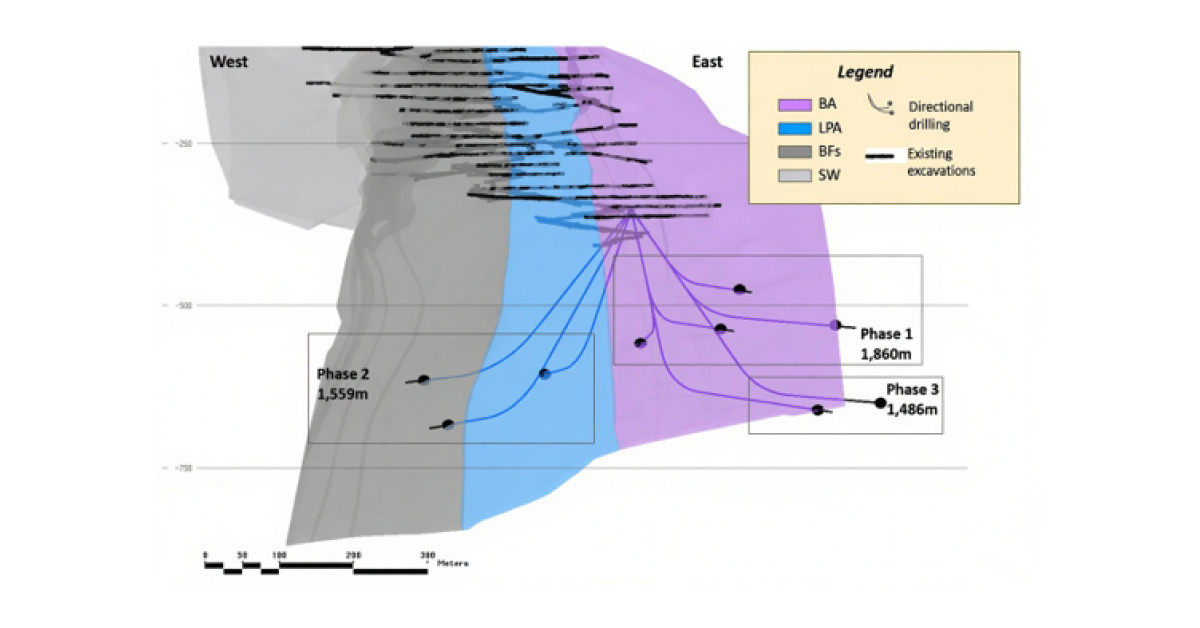

Jaguar Mining commenced a 5,000-metre directional drilling program at its Pilar gold mine in Brazil’s Minas Gerais, targeting three zones (BA, LPA, BF) below current workings that extend to 1.1km depth. The company expects the drilling to run for 10–12 months and aims to significantly extend life-of-mine beyond the current 8 years, supported by prior drilling indicating grade and mineralization widths increasing at depth. With Pilar producing 40,000+ ounces in 2025 and similar output expected for 2026, the initiative is intended to de-risk and convert depth targets into formal mineral resources, though the company cautions exploration may not result in resource delineation.

This is more valuable as a de-risking signal than a valuation catalyst. The real market mechanism is not “more ounces” on day one, but a longer runway for a fixed-processing-asset junior: if Pilar’s depth extensions convert, Jaguar can keep mills utilized, spread sustaining overhead across more ounces, and reduce the odds of a dilutive acquisition or equity raise to fund growth. That matters most if gold stays firm; in a flat gold tape, resource expansion at depth can still lift NAV, but it does not solve the small-cap financing discount by itself. The nearer-term winner is the drilling ecosystem, especially Major Drilling (MDI.TO), because this kind of multi-phase underground program is sticky, multi-quarter revenue with low cyclicality versus new-build capex. The second-order loser, if results are strong, is the acquisition market: a credible life-of-mine extension lowers Jaguar’s urgency to buy ounces, which can compress optionality premiums for nearby Brazilian juniors that trade on “strategic asset” scarcity. For sector peers, the read-through is that investors should reward brownfield conversion over greenfield storytelling, especially in Brazil where permitting and power/logistics risk can turn theoretical ounces into stranded value. The key risk is timing mismatch: the stock can rerate only after assay density and continuity are proven, while the drilling bill starts immediately. Over 1-3 months, the catalyst is data quality; over 6-18 months, the catalyst is resource classification and reserve conversion. What would falsify the bullish setup is a sequence of weak intercepts that show grade thinning at depth, or management needing to extend the drill campaign without upgrading the mine plan or guidance. Contrarian view: the market may be overpaying for ‘depth = better grade’ because deeper underground ounces often come with higher ventilation, hoisting, and geotechnical costs. If gold weakens, the present value of speculative ounces collapses faster than the operating cost base does. This is a better watch item than a high-conviction long in JAG.TO until the first phase data proves the down-plunge continuity and resource conversion path.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.15

Ticker Sentiment